During the recovery from the Great Recession, real interest rates on government securities have stayed low, but real returns on capital have rebounded. Although this divergence is puzzling in light of standard economic theory, it can be explained by credit market imperfections that raise the cost of capital and depress aggregate investment. The unusually slow credit market recovery is likely to have contributed to the diverging paths of the risk-free rate and returns on capital. It may have also contributed to a slow recovery in investment and output.

During the recovery from the Great Recession, inflation-adjusted or “real” interest rates on government securities have remained at historically low levels. Meanwhile returns on capital investments have rebounded sharply. This is puzzling when viewed through the lens of standard macroeconomic theory, which suggests that real returns on capital should be highly correlated with real interest rates. This Letter examines the sources of the divergence in the recovery paths of real interest rates and returns on capital. Our analysis suggests that the slow credit recovery after the Great Recession may have contributed to the divergence of returns as well as to the slow recovery in overall investment and output.

The puzzle of diverging paths for real interest rates and returns on capital

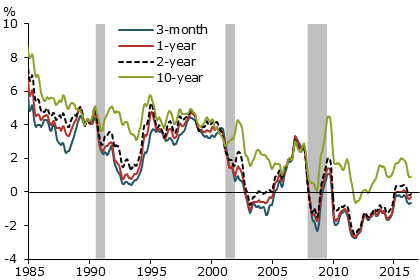

Real interest rates have declined since the early 2000s and remained low since the Great Recession. Figure 1 shows real interest rates on U.S. government securities, which are the nominal interest rates adjusted for realized inflation; the inflation rate here is measured by changes in the personal consumption expenditures price index (PCEPI). Persistently low interest rates have important implications for monetary policy (Williams 2016). Several economic factors may have contributed to the decline in real interest rates. One such factor may be the persistent or even permanent slowdown in productivity growth, which, combined with demographic shifts such as population aging and declines in labor force participation, can lead to sluggish growth of potential GDP (Fernald 2015). If households anticipate slow growth in the future, they would have an incentive to increase saving. Meanwhile, future slow growth discourages current investment. With a larger supply of funds available through savings and less demand for funds to use for investment, the real interest rate should fall. This factor is a part of the secular stagnation hypothesis highlighted by Summers (2014), among others.

Figure 1

Real nominal returns on Treasury securities

Source: Federal Reserve Board, Bureau of Economic Analysis; returns are shown as three-month moving averages.

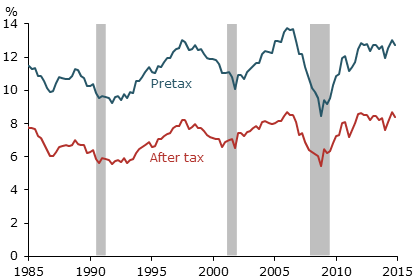

A related but less discussed phenomenon is the sharp rebound of real returns on capital investments following the Great Recession. Figure 2 shows the path of real returns on business capital before and after taxes, calculated based on the methodology described in Gomme, Ravikumar, and Rupert (2011). The rebound of capital returns and the declines in the real interest rates together imply that the excess return on capital has increased, resulting in a widening of the wedge between the two.

Figure 2

Real returns on capital investments

Source: Gomme, Ravikumar, and Rupert (2011) and authors’ calculation.

Persistent increases in the excess return on capital present a puzzle. Standard macroeconomic theory predicts that real returns on capital and real interest rates should be highly correlated. The premise is that declines in real interest rates reduce the cost of capital investment. As investment expands, returns on capital should fall. According to this theory, any deviations of returns on capital from the risk-free real interest rate should reflect compensation to investors for taking risks, commonly called the risk premium. Over the business cycle the risk premium can fluctuate, but on average it should not increase or decrease systematically. Thus, the standard theory predicts that returns on capital should not deviate persistently from risk-free rates, which is contrary to what we have observed since the Great Recession.

Credit constraints: A plausible resolution to the puzzle

In general, capital returns do not need to be highly correlated with risk-free rates. For example, if credit is constrained such that the supply cannot adjust to meet demand as it normally would to clear the market, those credit constraints may introduce a wedge between the risk-free rate and returns on capital. This possibility was especially relevant in the recent global financial crisis. As we will discuss in more detail, the credit market has recovered at an unusually slow pace since then, so credit constraints have remained tight.

Concerns about how credit constraints affect the real economy have led to a proliferation of macroeconomic models in recent years that incorporate financial market imperfections. One such model developed by Liu, Wang, and Zha (2013, hereafter LWZ) explicitly incorporates credit constraints in the form of limitations on investors’ ability to borrow against collateral assets such as land and physical capital. Like other models with credit constraints, the LWZ model implies that investors expect to receive excess returns on capital to compensate them for not just the loan interest rate but also for the implicit value of their internal funds due to limitations on borrowing capacity.

In a recession with credit constraints being tightened, it is more difficult for investors to obtain external funding. Tightened credit constraints have two consequences. First, only those projects with the highest returns are funded, so that the average return on capital rises. Second, in response to the tighter credit market, fewer projects are started, meaning fewer investment opportunities are available, which further exacerbates the declines in investment and output in the recession. As investment demand falls, the real interest rate also falls at any given level of savings. Overall, these tightened credit conditions lead to a widened wedge between the return on capital and the real interest rate and also contribute to declines in investment and output.

The LWZ model provides a useful framework for assessing the importance of credit market imperfections as a driving mechanism for macroeconomic fluctuations, and especially for business investment fluctuations that tend to be very volatile. For example, the estimated LWZ model suggests that financial shocks that affect investors’ borrowing capacity account for fluctuations of about 40 to 55% in business investment and about 30% in real GDP.

Some evidence of slow credit recovery

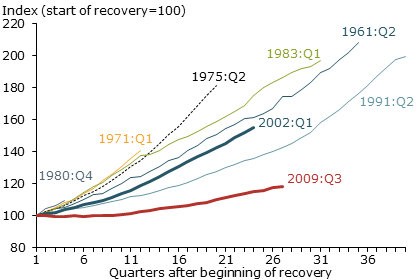

The implications of the LWZ model appear to be especially salient since the Great Recession. While credit conditions have recovered gradually, the overall pace of this recovery has been the slowest of any recession since the early 1960s. As shown in Figure 3, private credit extended to households and nonfinancial businesses in the current recovery (red line) has grown at a slower pace than in all previous recoveries shown. By the end of the first quarter of 2016, which was 27 quarters after the recovery began, private credit had increased only about 18% cumulatively from its level in the third quarter of 2009. In contrast, in the previous recovery that began in early 2002, private credit rose by more than 55% cumulatively in the following 24 quarters.

Figure 3

Private credit issued during recoveries

Source: Federal Reserve Board and NBER.

The slow credit recovery may be attributable to both credit supply and credit demand factors. On the supply side, regulations such as the Dodd-Frank Act that were passed in response to the global financial crisis may have contributed to tighter bank lending standards and thus slower growth in the credit supply. Indeed, although the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) suggests that banks have modestly eased their lending standards to large and medium-sized firms since mid-2009, such easing represents only a partial reversal from the extreme tightening of lending conditions during the crisis.

On the demand side, elevated economic uncertainty may have contributed to reductions in leverage and investment, leading to slower growth in credit demand. Both economic theory and empirical evidence suggest that uncertainty hinders aggregate demand (Basu and Bundick 2014; Leduc and Liu 2012, 2016). Facing higher uncertainty, households and firms choose to save more as a precaution and spend less on consumption and investment. Thus, uncertainty restrains credit demand.

With a slow credit recovery, credit constraints remain tight. Investors thus require a relatively high excess return on capital to compensate for the limitation of their borrowing capacity. In this sense, the observed diverging recovery paths of returns on capital and real interest rates are consistent with the theory that incorporates credit market imperfections.

Conclusion

Real returns on capital recovered rapidly after the Great Recession, while real interest rates stayed low. While this observation appears puzzling through the lens of standard economic theory, it is nonetheless predicted by macroeconomic models that account for imperfections in credit markets. Credit constraints introduce a wedge between returns on capital and the risk-free interest rate. Tighter credit conditions can lead to an increase in excess returns on capital and a simultaneous decline in the risk-free interest rate; they also restrain aggregate investment and other economic activity.

Evidence suggests that the recovery in credit markets following the Great Recession has been slower than previous recoveries, despite unconventional monetary policy easing. The still-tight credit conditions are likely to have contributed to the diverging paths of real returns on capital and the risk-free rate observed in the data. The slow credit market recovery may also have contributed to the slow recovery in aggregate output and investment.

Zheng Liu is a senior research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Andrew Tai is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Basu, Susanto, and Brent Bundick. 2014. “Uncertainty Shocks in a Model of Effective Demand.” NBER Working Paper 18420.

Fernald, John G. 2015. “Productivity and Potential Output Before, During, and After the Great Recession.” In NBER Macroeconomic Annual 2014, volume 29, eds. Jonathan Parker and Michael Woodford. Chicago: University of Chicago Press, pp. 1–51.

Gomme, Paul, B. Ravikumar, and Peter Rupert. 2011. “The Return to Capital and the Business Cycle.” Review of Economic Dynamics 14(2), pp. 262–278.

Leduc, Sylvain, and Zheng Liu. 2012. “Uncertainty, Unemployment, and Inflation.” FRBSF Economic Letter 2012-28 (September 17).

Leduc, Sylvain, and Zheng Liu. 2016. “Uncertainty Shocks Are Aggregate Demand Shocks.” Journal of Monetary Economics 82, pp. 20–35.

Liu, Zheng, Pengfei Wang, and Tao Zha. 2013. “Land-Price Dynamics and Macroeconomic Fluctuations.” Econometrica 81(3), pp. 1,147–1,184.

Summers, Lawrence. 2014. “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound.” Business Economics 49(2), pp. 65–73.

Williams, John C. 2016. “Monetary Policy in a Low R-star World.” FRBSF Economic Letter 2016-23 (August 15).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org