The prices of special securities known as TIPS can give some insight into how investors view the outlook for future inflation. New research uses a novel term structure model of nominal and real yields to estimate how much the liquidity premium embedded in the prices of these securities have varied over time. Accounting for variation in the premiums notably increases estimates of the inflation expectations underlying market-based measures of inflation compensation, particularly during the most recent financial crisis.

The liquidity of financial assets matters to investors and therefore has an effect on market prices. This is true even for the least risky assets, including securities issued by the U.S. Treasury. In this Letter, we focus on the liquidity risk in a segment of the market known as Treasury Inflation-Protected Securities (TIPS). These are Treasury securities whose coupon and principal payments move together with the consumer price index (CPI), a common measure of inflation. As a result, TIPS compensate investors for the erosion of purchasing power due to price inflation, and their yield is therefore given in real terms. In contrast, standard Treasury securities pay fixed nominal coupons on a known principal and hence deliver a nominal yield.

The difference between nominal and real yields of the same maturity is known as breakeven inflation (BEI). It represents a market-based measure of inflation compensation that is widely used to assess financial market participants’ inflation expectations. However, there are two issues with using BEI for that purpose. First, BEI contains an inflation risk premium, which is the additional return investors require to be exposed to the uncertainty of future inflation. This premium is a discount on securities that provide no inflation protection. Second, there is a difference in market liquidity between Treasuries and TIPS as TIPS have wider bid-ask spreads and smaller trade sizes (Fleming and Krishnan 2012). Because of their weaker market liquidity, the prices of TIPS are penalized with a price discount known as a liquidity premium that reflects the present value of expected future trading costs as well as compensation for assuming the risk of potentially being forced to sell the bond prematurely at a disadvantageous price. This pushes up TIPS yields and complicates the measurement of inflation expectations from BEI. The empirical challenge is that neither the inflation risk premium nor the liquidity premium are directly observable and must therefore be estimated.

In this Letter, we describe recent research by Andreasen, Christensen, and Riddell (2016, henceforth ACR), who introduce a novel dynamic term structure model that addresses the issue of estimating the liquidity premium in TIPS prices. Because the model also provides an adjustment for the inflation risk premium, we can adjust BEI for both premiums to gain insights into financial market participants’ underlying inflation expectations. Considering the relative importance of accounting for each premium, we find that omitting the adjustment for the TIPS liquidity premium leads to a sizable understatement of the outlook for inflation among financial market participants as reflected in the prices of Treasuries and TIPS that is particularly severe at the peak of the financial crisis.

A liquidity-adjusted model of nominal and real yields

ACR augment an existing model of nominal and real yields described in Christensen, Lopez, and Rudebusch (2010, henceforth CLR) with a factor to capture the liquidity premium in TIPS prices. It captures the idea that the amount of outstanding securities locked up in investors’ “buy-and-hold” portfolios and hence unavailable for trading grows over time.

We can identify the liquidity factor within the ACR model from its loading in the pricing of TIPS, which is a function of both the time since issuance and the remaining time to maturity. The time since issuance serves as a proxy for how unobserved changes in buy-and-hold investors’ holdings of a given TIPS security affect its liquidity premium. The remaining time to maturity shows how much time is left for this process to continue, and so we use it to generate the appropriate risk-adjusted discount. These two characteristics are unique for each TIPS, and both are needed to determine the size of its liquidity premium. The remaining factors in the model are identical to the factors in the CLR model; they represent general patterns in the level and shape of the nominal and real yield curves that would prevail in a world without any frictions to trading in financial markets.

To estimate the model and identify the liquidity factor, we follow ACR and use historical prices for the entire universe of five- and ten-year TIPS issued since the inception of the TIPS market in 1997. Specifically, we use end-of-month data from July 31, 1997, to August 31, 2016, available on Bloomberg. For each TIPS, we start the data at its official issuance date and end it a year before its maturity to avoid erratic prices close to expiry. Finally, we include a standard sample of nominal Treasury yields from Gürkaynak, Sack, and Wright (2007) in the estimation.

The TIPS liquidity premium

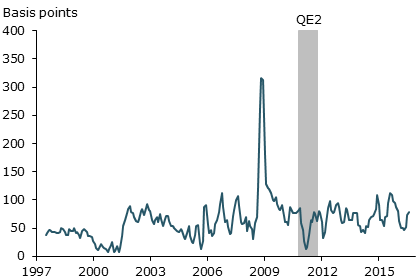

In general, we think of liquidity risk as having a negative effect on the TIPS market price or, equivalently, implying a higher yield for individual TIPS. However, the ACR model is flexible enough to allow for negative liquidity premiums if the data call for that. We identify the liquidity premium effect by calculating the fitted yield for each TIPS with and without the liquidity factor; we then back out the liquidity premium based on the difference in the fitted value. Taking the average of these liquidity premium estimates over all TIPS trading at each point in time produces the average TIPS liquidity premium series shown in Figure 1.

Figure 1

Average estimated TIPS liquidity premium

We next perform additional statistical analyses to assess the determinants of these liquidity premiums. In particular, we run standard regressions with the average TIPS liquidity premium shown in Figure 1 as the dependent variable and a number of explanatory factors that are thought to matter for TIPS market liquidity specifically or bond market liquidity more broadly.

The results reveal that the TIPS liquidity premium has a positive correlation with factors tied to economic uncertainty such as the VIX stock market volatility index and with measures of financial market frictions such as the yield spread between newly issued Treasury securities and comparable more seasoned Treasuries, known as the on-the-run premium. Furthermore, there is evidence that large-scale asset purchases such as those the Fed used in response to the financial crisis of 2007–08 and its aftermath may affect financial market functioning. The figure shows a clear dip during the Fed’s second large-scale asset purchase program, commonly known as QE2, which included $26 billion in TIPS purchases. This is consistent with analysis in Christensen and Gillan (2016). They argue that a central bank launching a large-scale asset purchase program acts as a large committed buyer with unusual preferences in that it trades strategically to raise asset prices. This effectively eliminates the most severe downside risk of the targeted securities while the program is in operation, which reduces investors’ fear of unfavorable liquidity squeezes and temporarily lowers the liquidity premiums in the targeted securities.

Model-implied inflation expectations

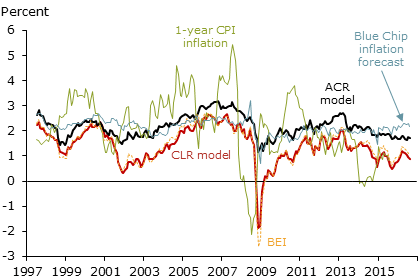

We next address how adjusting for liquidity premiums in TIPS prices affects the model’s assessment of the outlook for inflation underlying Treasury and TIPS prices. Figure 2 shows the model estimate of financial market participants’ expected inflation for the following year. The red line indicates the estimate from the CLR model that makes no adjustment for the liquidity risk in TIPS prices, while the black line shows the estimate from the ACR model that adjusts for TIPS liquidity premiums.

Figure 2

One-year expected inflation

First, we note that both series vary substantially as expected given the changing economic environment over the past 20 years. Second, the liquidity-adjusted estimate from the ACR model is higher and smoother, averaging about 0.75% above the CLR model estimate. The differences between the two series are largest whenever TIPS liquidity premiums tend to be above average, as in the early 2000s and around the peak of the financial crisis in late 2008. Intuitively, these are the times when accounting for liquidity premiums in TIPS prices matters most. Importantly, though, even outside these periods there is typically a sizable wedge between the two estimates of inflation expectations.

Second, we note that the calculated one-year BEI (yellow dashed line) is close to the one-year expected inflation from the CLR model. Due to the lack of liquidity adjustment in this model, the difference between these two series equals the inflation risk premium, which is small at the one-year horizon. Hence, for understanding the variation in BEI, TIPS liquidity premiums are an order of magnitude above the inflation risk premium in importance.

Unlike the CLR model, the one-year expected inflation from the ACR model is close to the one-year inflation expectations reflected in surveys of economic forecasters such as the Blue Chip Economic Indicators (light blue line). Assuming the survey forecasts are accurate, this evidence suggests that the adjustment for TIPS liquidity premiums in the ACR model could improve its ability to predict future inflation. However, since both model series represent full sample estimates, they cannot be used in a formal forecast evaluation. Still, comparing them with the subsequent year-over-year CPI inflation (green line) can help assess whether the estimates are reasonable. The one-year expected inflation from the CLR model is further away from the CPI measured by both mean differences and root mean squared differences. Thus, this also suggests that accounting for TIPS liquidity could help improve the ACR model’s ability to forecast inflation. However, given that the model series are full sample estimates, we caution against drawing final conclusions from this comparison and leave it to future research to formally evaluate their out-of-sample inflation forecast performance.

Conclusion

In this Letter, we describe new research that uses a novel term structure model of nominal and real yields to estimate the liquidity premium embedded in TIPS prices; we then use these estimates to adjust market-based measures of inflation compensation and extract investors’ embedded inflation expectations. The results show that TIPS liquidity premiums have varied quite notably since the inception of the TIPS market in 1997. Thus, liquidity represents a significant risk factor in the pricing of TIPS. We also demonstrate that accounting for the liquidity premium changes the model’s assessment of market participants’ inflation expectations materially. Specifically, the outlook for inflation one year ahead average about 0.75% higher once we account for the liquidity premium. These findings underscore that market-based measures of inflation compensation such as BEI should not automatically be equated with investors’ inflation expectations.

Martin M. Andreasen is a professor at Aarhus University, Denmark.

Jens H.E. Christensen is a research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Andreasen, Martin M., Jens H.E. Christensen, and Simon Riddell. 2016. “The TIPS Liquidity Premium.” Unpublished manuscript, FRB San Francisco.

Christensen, Jens H.E. and James M. Gillan. 2016. “Does Quantitative Easing Affect Market Liquidity?” FRB San Francisco Working Paper 2013-26.

Christensen, Jens H.E., Jose A. Lopez, and Glenn D. Rudebusch. 2010. “Inflation Expectations and Risk Premiums in an Arbitrage-Free Model of Nominal and Real Bond Yields.” Journal of Money, Credit and Banking 42 s1, pp. 143–178.

Fleming, Michael J., and Neel Krishnan. 2012. “The Microstructure of the TIPS Market.” FRB New York Economic Policy Review 18(1), pp. 27–45.

Gürkaynak, Refet S., Brian Sack, and Jonathan H. Wright. 2007. “The U.S. Treasury Yield Curve: 1961 to the Present.” Journal of Monetary Economics 54(8), pp. 2,291–2,304.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org