The pace of business start-ups in the United States has declined over the past few decades. Economic theory suggests that business creation depends on the available workforce, and data analysis supports this strong link. By contrast, the relationship between start-ups and labor productivity is less well-defined, in part because entrepreneurs face initial costs that rise with productivity, specifically their own lost income from alternative employment. Overall, policies that incorporate improving labor availability may help to boost new business growth.

By many measures, the rate of U.S. business formation has declined over the past 30 years. This decline appears to be pervasive across industries and regions (Davis and Haltiwanger 2014). Considerable research has raised concerns that this may slow down long-run growth in the United States (see Decker et al. 2016 and Prescott and Ohanian 2014).

In this Letter, we examine the theoretical factors that determine the number of businesses in the economy: the size of the available workforce and the level of labor productivity. We compare predictions based on these factors with actual patterns of U.S. business formation. We find that population size is more important than productivity for explaining the number of businesses. This finding suggests that policies aiming to boost business formation are more likely to be effective if they also improve labor availability.

A theory of business formation

To think about how policies can boost business formation, it is useful to first understand conditions that affect the number of businesses in the economy. One common way of thinking about this in economics is the life cycle of businesses. This theory suggests that the decision of whether to operate a business depends on how potential costs compare with revenue.

The first type of cost is variable, meaning it increases with the size of the business. For example, raw materials and wages paid to employees are usually variable costs because they rise according to how much of its product the business can sell. The second type of cost is fixed and does not vary significantly with a business’s size. License fees are an obvious example. Others include certain capital expenses, such as the cost of the machines needed for production or the rent paid for the land or building. Less obvious fixed costs are the lost earnings that business owners give up by operating a business instead of working for someone else. Taken together, these fixed costs are essentially synonymous with start-up costs.

The other side of the equation in deciding to start a business revolves around demand for the product. To simplify, imagine that two businesses in a market each have a unique product. For example, Coke and Pepsi coexist because they are somewhat different and some customers prefer one to the other. Demand for a firm’s product depends not only on its price relative to competing products but also on the aggregate conditions of the economy. If the price of Coke increases more than Pepsi, some customers may switch to Pepsi and raise the relative demand for that product. The total demand for Coke and Pepsi, on the other hand, depends on the general economic conditions, such as the size of the population and the income of each person. All else equal, aggregate demand increases with population because more people means more customers. Demand also increases with income per person because each customer is likely to have more money to spend.

In the theory, entrepreneurs plan their production to maximize their gross profit, which is the difference between revenue and variable costs. They will start a business only if potential gross profits can cover the fixed costs of operating the business. When gross profits exceed fixed costs, more businesses will enter the market. Competition among more businesses for scarce resources will drive up costs and reduce gross profits. When fixed costs exceed gross profits, some businesses will close. Less competition drives down costs and raises gross profits. With a large number of businesses in the economy, the theory suggests that businesses on average can expect to break even. Note that in this theory, breaking even does not mean zero accounting profits: a business must report just enough positive accounting profit to cover fixed costs, such as the income the entrepreneur would make in an alternative pursuit, which is not part of the businesses accounts.

Fixed costs of businesses rise with growth

In this theory, the number of businesses in the economy adjusts through openings and closings such that, on average, gross profits equal fixed costs. What determines this level? Two factors that could determine business formation in the long run are the size of the population and labor productivity. A larger population increases the number of customers, which, all else equal, increases demand and thus encourages more businesses to form.

The effect of higher productivity on the number of businesses is less clear. On one hand, higher productivity translates into higher income per capita in the long run. This increases demand. Higher productivity can also reduce variable costs by lowering the amount of inputs needed to produce a unit of output. These forces raise gross profits and encourage more businesses to form. On the other hand, however, if a large part of the fixed costs are labor expenses, such as the forgone income of the entrepreneurs, then higher productivity could raise the income the owners could have earned as employees working for someone else. Importantly, this raises the fixed costs of business formation. Fixed costs may also increase with productivity if higher productivity is achieved through the use of more sophisticated, and more expensive, machinery. In short, under this theory, the number of businesses increases with population but not necessarily with productivity, if fixed costs increase with productivity.

The natural follow-up question is whether fixed costs rise with productivity. Measuring fixed costs directly is difficult because they include forgone income that is not observed. A less direct but more feasible method is to use gross profits to proxy for fixed costs. Recall that, in the model, entry and exit of businesses adjust such that fixed costs equal average gross profits. Bollard, Klenow, and Li (2016) applied this indirect approach to the U.S. manufacturing sector using firm-level data from the U.S. Census Bureau. They examined the period from the late 1960s to the present and found that their proxy for fixed costs rises strongly with labor productivity.

Unfortunately, data are not available to measure gross profits for other sectors in the U.S. economy. As an alternative approach, one can look at how the number of businesses varies with the number of workers and labor productivity. From the model, we would expect the number of businesses to rise with workforce size, all else equal, because higher workforce size increases product demand without raising costs. We would expect the number of businesses to rise with productivity, all else equal, only if fixed costs do not also rise with productivity.

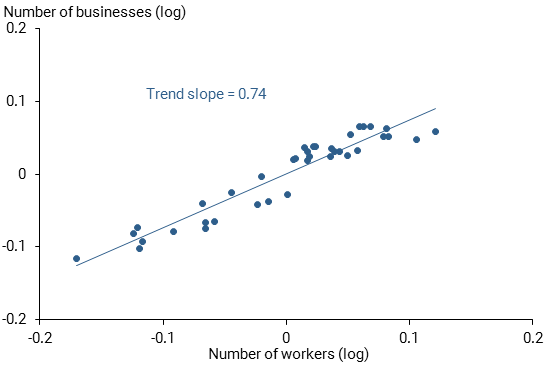

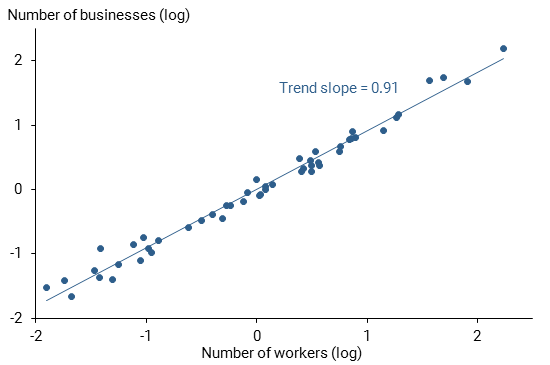

Figures 1 and 2 plot the relationship between the log number of employer businesses and the log number of employees for all U.S. private businesses after controlling for log labor productivity, defined as real output per worker. Figure 1 looks at the national level and covers the entire 1977 to 2014 period for which data are available. Figure 2 reports individual states in 2014, the latest year of our data sample. The slope reported in each graph captures the percent increase in the number of businesses associated with a 1% increase in the number of workers. It shows that, controlling for the growth rate of labor productivity, a 1% increase in the number of workers is associated with a 0.74% increase in the number of businesses at the national level and an almost 1% increase at the state level.

Figure 1

Number of U.S. businesses vs. workers, 1977 to 2014

Source: Census Bureau Business Dynamics Statistics, Bureau of Economic Analysis.

Figure 2

Number of businesses vs. workers across states, 2014

Source: Census Bureau Business Dynamics Statistics, Bureau of Economic Analysis.

Workforce size predicts over 90% of the variation in the number of businesses after controlling for labor productivity, both nationally over time and across states in 2014. In contrast, labor productivity predicts only 1% of the variation after controlling for workforce size at the national level, and only 5% of the cross-state variation in 2014. Notably, these cross-state patterns hold in every other year of our data sample as well. Over the past few decades, the number of businesses in the United States has moved much more closely with workforce size than with labor productivity, consistent with the theory of fixed costs rising with productivity.

This finding may seem somewhat surprising at the state level, considering the often large differences in regulations and taxes between states. For example, California requires businesses to cover broader employment insurance than other states (U.S. Small Business Administration 2016). One would expect the broader requirement to raise the cost of doing business in California relative to other states, discouraging business formation. However, as surveyed by Hathaway and Litan (2014), there is no consensus among research papers on the relationship between state policies and business formation. Instead, similar to the relationship we show in Figure 2, they find that business start rates are higher in states with higher population growth rates.

Policy implications

Taken together, the evidence suggests that the fixed costs of business formation have historically increased with labor productivity in the United States. This has important implications for the impact of policies on business formation. To see why, consider a policy that aims to stimulate business formation by subsidizing loans to businesses. In addition, suppose fixed costs increase with productivity because fixed costs include the forgone labor income of entrepreneurs. All else equal, this policy would encourage more businesses to form by reducing borrowing costs. However, if there were no change in the number of entrepreneurs available, then new businesses entering the market would increase labor demand relative to supply, putting upward pressure on wages and therefore fixed costs. As a result, this policy might not significantly increase business formation.

Our analysis suggests these types of policies might be more effective if they were paired with workforce development programs. Increasing the labor supply and hence the supply of potential entrepreneurs can stimulate business formation by increasing demand without raising costs. Possible strategies could include encouraging more immigration, later retirement, or higher labor participation among women. Other strategies could involve increasing the pool of effective labor through education, as in the recent proposal by Federal Reserve Chair Janet Yellen (Yellen 2017).

Conclusion

In this Letter, we discuss how business start-ups are theoretically linked to the availability of labor and to labor productivity. Historical data appear to support the theory that the fixed costs of operating businesses generally rise with productivity in the United States, which suggests improving productivity is not particularly helpful for boosting new business formation. One potential explanation is that fixed costs include the labor costs of business founders. However, workforce availability has a strong link to business start-ups in historical data. This finding suggests that policies to stimulate business formation are likely to be more effective if they include strategies that expand the labor supply. Increasing the workforce could not only raise the supply of available entrepreneurs but could also raise the demand for more businesses.

Patrick Kiernan is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Huiyu Li is an economist in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Bollard, Albert, Peter J. Klenow, and Huiyu Li. 2016. “Entry Costs Rise with Development.” Manuscript.

Davis, Steven J., and John Haltiwanger. 2014. “Labor Market Fluidity and Economic Performance.” In Re-Evaluating Labor Market Dynamics, conference proceedings of the 2014 Jackson Hole Economic Symposium. Kansas City: Federal Reserve Bank of Kansas City, pp. 17–107.

Decker, Ryan, John Haltiwanger, Ron Jarmin, and Javier Miranda. 2014. “The Role of Entrepreneurship in U.S. Job Creation and Economic Dynamism.” Journal of Economic Perspectives 28(3), pp. 3–24.

Hathaway, Ian, and Robert E. Litan. 2014. “What’s Driving the Decline in the Firm Formation Rate? A Partial Explanation.” Brookings Institution.

Prescott, Edward C., and Lee E. Ohanian. 2014. “Behind the Productivity Plunge: Fewer Startups.” Commentary, Wall Street Journal, June 25.

U.S. Small Business Administration. 2016. “Determine Your State Tax Obligations.”

Yellen, Janet. 2017. “Addressing Workforce Development Challenges in Low-Income Communities.” Speech at “Creating a Just Economy,” 2017 Annual Conference of the National Community Reinvestment Coalition in Washington, DC, March 28.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org