In official statistics, manufacturing is the top contributor to U.S. productivity growth despite its shrinking share of employment. However, official numbers tend to understate growth among new producers that improve on existing producers, which is more prevalent outside of manufacturing. Accounting for such missing productivity growth shows that it plays a larger role in sectors such as retail trade and services. Also, the relative contribution of manufacturing to productivity growth has dropped significantly. These findings suggest that nonmanufacturing may be an increasingly important engine of U.S. growth.

Recent debates surrounding trade policies raise questions about the consequences for the U.S. economy, particularly for manufacturers. Manufacturing is widely believed to be the main engine of aggregate productivity growth (see, for example, Sharma 2018). This belief is driven in part by studies using official statistics that show manufacturing has played an outsized role in driving productivity growth, even as its share of employment has steadily shrunk in advanced economies since 2000 (see Santacreu and Zhu 2018).

However, official statistics may not fully capture productivity growth stemming from creative destruction, as an earlier Economic Letter by Klenow and Li (2017) argued. This source of missing growth is likely to be larger for sectors outside of manufacturing, as shown by Aghion et al. (2019). I apply this analysis to reevaluate the contribution of nonmanufacturing to U.S. productivity growth in recent years in this Letter. I find, indeed, that official statistics may have drastically understated the contribution of nonmanufacturing to U.S. economic growth.

Measuring productivity growth

To evaluate official measures of productivity growth for different sectors, I use Bureau of Labor Statistics (BLS) data. I compare the contribution of nonmanufacturing over 1996–2005, when the United States had high aggregate productivity growth, to 2006–2013, when productivity growth was lower. The data end in 2013 to match the availability of data for calculating missing growth in Aghion et al. (2019).

The BLS classifies economic activities into 11 sectors: manufacturing, agriculture, mining, utilities, construction, wholesale trade, retail trade, transportation and warehousing, information, FIRE (finance, insurance, and real estate), and services, which contains producers not classified in the other sectors. For example, restaurants and hotels are in services, but banks are in FIRE, and Amazon is in retail trade.

I report growth individually for the three sectors with the largest employment shares—manufacturing, retail trade, and services, and combine the remaining sectors except for agriculture, which is not reported in Aghion et al. (2019). The three largest sectors accounted for almost 80% of private-sector nonfarm employment on average between 1989 and 2013. Growth in a sector is calculated as the difference between output growth and input growth in a sector adjusted for inflation; inputs are goods, capital, and labor used for production.

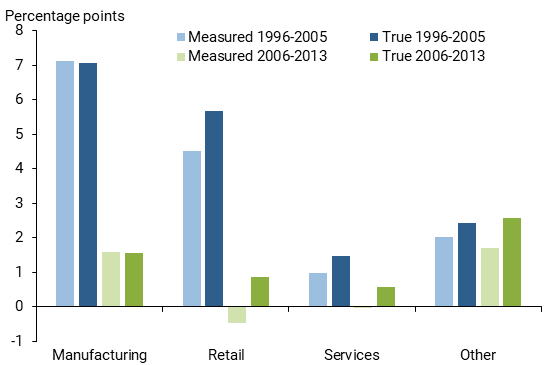

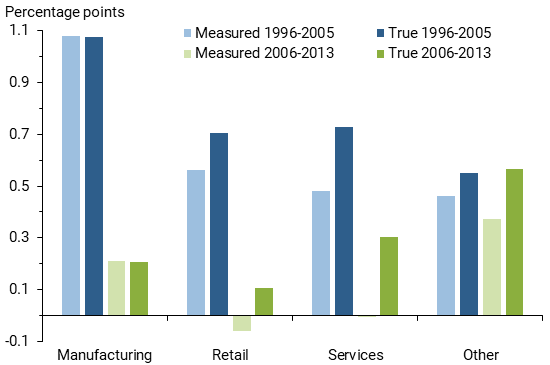

The light blue and green bars in Figure 1 display the measured productivity growth within manufacturing, retail trade, services, and other combined sectors for the two periods. The light blue and green bars in Figure 2 display the contribution of each of those sectors to productivity growth in percentage points, defined as the productivity growth in the sector multiplied by its employment share. Total U.S. productivity growth equals the average productivity growth over all sectors of the economy, weighting each sector by its employment share.

Figure 1

Measured vs. estimates of true productivity growth

Figure 2

Measured vs. estimates of true contributions to total growth

According to the BLS data, manufacturing productivity grew 7.1% per year during the earlier period and only 1.6% per year during the later period. Accounting for its share of the economy, manufacturing contributed 1.1 percentage points out of the 2.6% overall growth in the high-growth period and 0.2 percentage point of the 0.5% growth during the low-growth period. That is, even though manufacturing’s employment share shrank from 16% to 11% between the two periods and its productivity growth declined significantly, manufacturing still accounted for slightly over 40% of the overall productivity growth in the later period, just as it did in the earlier period.

The persistently outsized role of manufacturing in the official statistics is due to the lackluster measured growth in other major sectors. For example, while the services sector has a 49% share of employment in the early period and 54% later, its productivity growth was less than 1% in the early period and practically zero later. As a result, manufacturing contributed more to productivity growth than its share of employment and sustained its contribution even as its productivity growth and employment share fell.

Accounting for creative destruction

The findings based on official BLS data are in line with the conventional thinking that manufacturing is the main engine of U.S. productivity growth today as it was in the past. However, Aghion et al. (2019) found that official statistics understate growth in sectors outside of manufacturing.

They consider two types of innovation: creative destruction and in-house. Creative destruction involves new producers taking part of the market share from existing producers by creating products that are either of higher quality at a similar price or similar quality at a lower price. For example, new retail stores and restaurants enter the market by adding establishments. This is an example of creative destruction in that new stores capture market share from existing local stores. In contrast, the second type involves existing producers improving their own products through research and development. For example, Intel rolls out faster CPUs (central processing units) every year.

In manufacturing, new innovative products often emerge in-house from existing firms and are produced by existing production plants. On the other hand, in nonmanufacturing sectors, innovation tends to occur more frequently through creative destruction. Official statistics can measure in-house innovation with various methods, but it is more difficult to evaluate productivity improvement from creative destruction because the creatively destroyed products often disappear. As a result, official statistics may miss more growth from nonmanufacturing sectors and understate their contribution to total growth.

To adjust for missing growth, I use the results from Aghion et al. (2019), who calculated missing growth using the change in the market share of incumbent producers based on employment share. The idea behind this approach is that changes in market share reflect how innovative incumbents are relative to new producers. Standard measurement assumes they are equally innovative, which implies stable incumbent market share. A shrinking incumbent market share is a sign that these existing producers are not as innovative as new ones, which in turn would imply that standard measurement understates growth from creative destruction. For a summary of the method I use, see Klenow and Li (2017).

The darker blue and green “true” bars in Figure 1 display the sum of measured growth and the missing growth in each sector as reported in Aghion et al. (2019). The true manufacturing bars are very close to the measured bars. That is, manufacturing has very little missing growth in both periods. On the other hand, the retail trade and services sectors have significant missing growth. For example, the early period shows that 0.5 percentage point of growth is missed in the services sector. According to Aghion et al. (2019), much of this missing growth comes from accommodations and restaurants, where the net entry of establishments tends to be quite rapid and contributes to high levels of creative destruction. There is a similar gap between the measured and true numbers for services, suggesting that missing growth in services has persisted into the low-growth period.

Turning to retail trade, Figure 1 shows there was more than 1 percentage point of missing growth in both the high- and low-growth periods; this sector is also characterized by high levels of creative destruction via entry and exit. In total, correcting for missing growth increases U.S. productivity growth from 2.6 to 3.1% in the high-growth period and from 0.5 to 1.2% in the low-growth period.

The darker blue and green bars in Figure 2 display the contribution of each sector to overall productivity growth after accounting for missing growth. The differences between the heights of the true and measured bars capture each sector’s contribution to total missing growth. The figure shows very little missing growth from manufacturing but considerable missing growth from retail trade, services, and the remaining sectors, with the services sector contributing the most. In fact, in the official statistics, productivity growth in retail and services together is negative in the post-2006 period, while the missing growth analysis suggests that retail and services contributed positively to aggregate productivity growth in the later period.

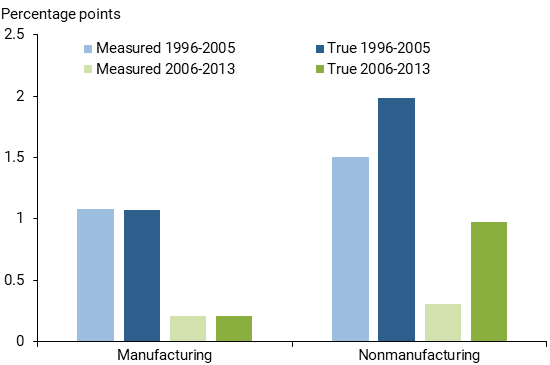

To highlight the contrast between manufacturing and nonmanufacturing, I combine the nonmanufacturing sectors in Figure 3. The figure shows that essentially all of the missing growth can be attributed to the nonmanufacturing sectors. Accounting for creative destruction boosts the contribution of the nonmanufacturing sectors to overall productivity growth from 58% to 65% in the earlier period and from 59% to 82% in the later period. Unlike the official statistics, I find a larger and increasing contribution to productivity growth from nonmanufacturing activities.

Figure 3

Manufacturing, nonmanufacturing contribution to total growth

What if the nonmanufacturing share of employment did not increase?

I calculate the contribution of a sector to productivity growth by multiplying the sector’s productivity growth by its employment share. Hence, an increase in nonmanufacturing’s contribution to productivity growth can come from both an increasing share of workers in nonmanufacturing and an increase in nonmanufacturing productivity growth relative to manufacturing. To distinguish between these two channels, I calculate what the productivity contribution from the nonmanufacturing sectors would have been had this group’s employment share stayed at its average over 1996–2005. This means moving 5% of workers to manufacturing.

Using only BLS data, nonmanufacturing’s contribution to productivity growth decreases 0.015 percentage point while manufacturing contribution increases 0.084 percentage point. On net, aggregate productivity growth is 0.07 percentage point or 13% higher. The contribution of nonmanufacturing to aggregate productivity growth changes from 59% to 50%.

After accounting for missing growth from creative destruction, however, nonmanufacturing contribution declines 0.049 percentage point. On net, aggregate productivity growth increases 0.03 percentage point or only 3%. The contribution of nonmanufacturing falls from 83% to 76%, which is still significantly higher than the 65% in the high-growth period. Thus, using our corrected productivity figures, an employment shift back to manufacturing would have virtually no effect on aggregate productivity growth.

Conclusion

This Letter shows that, when one accounts for the productivity growth from creative destruction that is missed by official statistics, the contribution of nonmanufacturing sectors to aggregate productivity growth rises substantially, particularly after 2006. This increase is mostly due to the increase in nonmanufacturing productivity growth relative to manufacturing, not its expanding share of total employment. Contrary to much economic commentary, continued expansion of the nonmanufacturing sector’s share of the U.S. economy could actually boost true U.S. productivity growth if this process of creative destruction continues. Sectors such as services may have overtaken manufacturing as the engine of growth.

Huiyu Li is an economist in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Aghion, Philippe, Antonin Bergeaud, Timo Boppart, Peter J. Klenow, and Huiyu Li. 2019. “Missing Growth from Creative Destruction.” Forthcoming, the American Economic Review.

Klenow, Peter J., and Huiyu Li. 2017. “Missing Growth from Creative Destruction.” FRBSF Economic Letter 2017-31 (October 23).

Santacreu, Ana Maria, and Heting Zhu. 2018. “Manufacturing and Service Sector Roles in the Evolution of Innovation and Productivity.” FRB St Louis Economic Synopses 2018(2).

Sharma, Prerna. 2018. “Manufacturing Jobs: Implications for Productivity and Inequality.” Brookings Blog, Up Front, May 1.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org