Climate change describes the current trend toward higher average global temperatures and accompanying environmental shifts such as rising sea levels and more severe storms, floods, droughts, and heat waves. In coming decades, climate change—and efforts to limit that change and adapt to it—will have increasingly important effects on the U.S. economy. These effects and their associated risks are relevant considerations for the Federal Reserve in fulfilling its mandate for macroeconomic and financial stability.

To help foster macroeconomic and financial stability, it is essential for Federal Reserve policymakers to understand

how the economy operates and evolves over time. In this century, three key forces are transforming the economy: a

demographic shift toward an older population, rapid advances in technology, and climate change. Climate change has

direct effects on the economy resulting from various environmental shifts, including hotter temperatures, rising sea

levels, and more frequent and extreme storms, floods, and droughts. It also has indirect effects resulting from

attempts to adapt to these new conditions and from efforts to limit or mitigate climate change through a transition to

a low-carbon economy. This Economic Letter describes how the consequences of climate change are relevant for

the Fed’s monetary and financial policy.

Climate change and the transition to a low-carbon economy

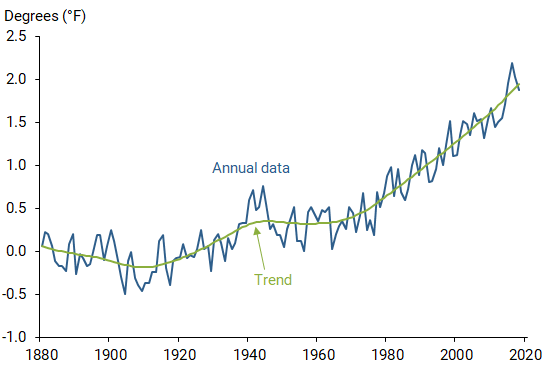

Surface temperatures were first regularly recorded around the world in the late 1800s. Since then, the global average

temperature has risen almost 2°F (Figure 1) with further increases projected (IPCC 2018). Based on extensive

scientific theory and evidence, a consensus view among scientists is that global warming is the result of carbon

emissions from burning coal, oil, and other fossil fuels. Indeed, as early as 1896, the Swedish chemist Svante

Arrhenius showed that carbon emissions from human activities could cause global warming through a greenhouse effect.

The underlying science is straightforward: Certain gases in the atmosphere, such as carbon dioxide and methane,

capture the sun’s heat that is reflected off the Earth’s surface, thus blocking that heat from escaping into space.

These greenhouse gases act like a blanket around the earth holding in heat. As more fossil fuels are burned, the

blanket gets thicker, and global average temperatures increase. Other empirical measurements have confirmed many

related adverse environmental changes such as rising sea levels and ocean acidity, shrinking glaciers and ice sheets,

disappearing species, and more extreme storms (USGCRP 2018).

Figure 1

Change in global average temperature relative to 1880–1900

Note: Global average surface temperature based on land and ocean data from the National Aeronautics and Space Administration (NASA).

Climate change also affects the U.S. economy. The latest National Climate Assessment, a 1,515-page

scientific report produced by 13 federal agencies as required by law, summarized this impact:

Without substantial and sustained global mitigation and regional adaptation efforts, climate change is

expected to cause growing losses to American infrastructure and property and impede the rate of economic growth over

this century (USGCRP 2018, pp. 25–26).

Economists view these losses as the result of a fundamental market failure: carbon fuel prices do not properly

account for climate change costs. Businesses and households that produce greenhouse gas emissions, say, by driving

cars or generating electricity, do not pay for the losses and damage caused by that pollution. Therefore, they have no

direct incentive to switch to a low-carbon technology that would curtail emissions. Without proper price signals and

incentives in the private market, some kind of collective or government action is necessary. One solution would be to

charge for the full cost of carbon pollution through an extra fee on emissions—a carbon tax—that would account for the

costs of climate change on the economy and society. Many leading economists are calling for a carbon tax to correct

market pricing (Climate Leadership Council 2019, Fried, Novan, and Peterman 2019).

A carbon tax that is set at the proper level can appropriately incentivize innovations in clean technology and the

transition from a high- to a low-carbon economy. Such a carbon tax should equal the “social cost of carbon,” which

measures the total damage from an additional ton of carbon pollution (Auffhammer 2018). A crucial consideration in

calculating this cost is that carbon pollution dissipates very slowly and will remain in the atmosphere for centuries,

redirecting heat back toward the earth. Consequently, today’s carbon pollution will create climate hazards for many

generations to come. A second difficulty in calculating the social cost of carbon is tail risk, namely, the

possibility of catastrophic future climate damage (Heal 2017). A final complication is that the causes and

consequences of climate change are global in scope. The resulting intergenerational and international market failure

is so problematic that some economists doubt that a carbon tax alone would suffice (Tvinnereim and Mehling 2018).

Instead, a comprehensive set of government policies may be required, including clean-energy and carbon-capture

research and development incentives, energy efficiency standards, and low-carbon public investment (Gillingham and

Stock 2018).

Climate change and the Fed

Given the role of government in addressing climate change, how does the Federal Reserve fit in? In particular, how

does climate change relate to the Fed’s goals of financial and macroeconomic stability? With regard to financial

stability, many central banks have acknowledged the importance of accounting for the increasing financial risks from

climate change (Scott, van Huizen, and Jung 2017, NGFS 2018). These risks include potential loan losses at banks

resulting from the business interruptions and bankruptcies caused by storms, droughts, wildfires, and other extreme

events. There are also transition risks associated with the adjustment to a low-carbon economy, such as the unexpected

losses in the value of assets or companies that depend on fossil fuels. In this regard, even long-term risks can have

near-term consequences as investors reprice assets for a low-carbon future. Furthermore, financial firms with limited

carbon emissions may still face substantial climate-based credit risk exposure, for example, through loans to affected

businesses or mortgages on coastal real estate. If such exposures were broadly correlated across regions or

industries, the resulting climate-based risk could threaten the stability of the financial system as a whole and be of

macroprudential concern. In response, the financial supervisory authorities in a number of countries have encouraged

financial institutions to disclose any climate-related financial risks and to conduct “climate stress tests” to assess

their solvency across a range of future climate change alternatives (Campiglio et al. 2018).

Some central banks also recognize that climate change is becoming increasingly relevant for monetary policy (Lane

2017, Cœuré 2018). For example, climate-related financial risks could affect the economy through elevated credit

spreads, greater precautionary saving, and, in the extreme, a financial crisis. There could also be direct effects in

the form of larger and more frequent macroeconomic shocks associated with the infrastructure damage, agricultural

losses, and commodity price spikes caused by the droughts, floods, and hurricanes amplified by climate change (Debelle

2019). Even weather disasters abroad can disrupt exports, imports, and supply chains close to home. As a much more

persistent factor, Colacito et al. (2018) found that the current trend toward higher temperatures on its own has

slowed growth in a variety of sectors. They estimated that increased warming has already started to reduce average

U.S. output growth and that, as temperatures rise, growth may be curtailed by more than ½ percentage point later in

this century.

On top of these direct effects, climate adaptation—with spending on equipment such as air conditioners and resilient

infrastructure including seawalls and fortified transportation systems—is expected to increasingly divert resources

from productive capital accumulation. Similarly, sizable investments would be necessary to reduce carbon pollution and

mitigate climate change, and the transition to a low-carbon future may affect the economy through a variety of other

channels (Batten 2018). In short, climate change is becoming relevant for a range of macroeconomic issues, including

potential output growth, capital formation, productivity, and the long-run level of the real interest rate.

Nevertheless, some view the economic and financial concerns surrounding climate change as having either too short or

too long a time horizon to affect monetary policy decisions. Indeed, at the short end, monetary policy typically does

not react to temporary disturbances from weather events like hurricanes or blizzards. However, climate change could

cause such shocks to grow in size and frequency and their disruptive effects could become more persistent and harder

to ignore. At the long end, most of the consequences of climate change will occur well past the usual policy forecast

horizon of a few years ahead. However, even longer-term factors can be relevant for monetary policy. For example,

central banks routinely consider the policy implications of demographic trends, such as declining labor force

participation, which have long-run effects much like climate change. In addition, prices of equities and long-term

financial assets depend on expected future conditions, so even climate risks decades ahead can have near-term

financial consequences. Climate change could also be a factor in achieving and maintaining low inflation. It took a

decade or two—a relevant time scale for climate change—for the Fed to achieve its inflation objective after the Great

Inflation of the 1970s and the Great Recession. Finally, the economic research that quantifies optimal monetary policy

routinely uses a very long-run perspective that takes into account inflation and output quite far out in the future.

While the effects and risks of climate change are relevant factors for the Fed to consider, the Fed is not in a

position to use monetary policy actively to foster a transition to a low-carbon economy. Supporting environmental

sustainability and limiting climate change are not directly included in the Fed’s statutory mandate of price stability

and full employment. Furthermore, the Fed’s short-term interest rate policy tool is not amenable to supporting

low-carbon industries. Wind farms in Kansas and coal mines in West Virginia face the same underlying risk-free

short-term interest rate. Instead, some have advocated that central banks use their balance sheet to support the

transition to a low-carbon economy, for example, by buying low-carbon corporate bonds (Olovsson 2018). Such “green”

quantitative easing is an option for some central banks but not for the Fed, which by law can only purchase government

or government agency debt.

Conclusion

Many central banks already include climate change in their assessments of future economic and financial risks when

setting monetary and financial supervisory policy. For the Fed, the volatility induced by climate change and the

efforts to adapt to new conditions and to limit or mitigate climate change are also increasingly relevant

considerations. Moreover, economists, including those at central banks, can contribute much more to the research on

climate change hazards and the appropriate response of central banks.

Glenn D. Rudebusch is senior policy advisor and executive vice president in the Economic

Research Department of the Federal Reserve Bank of San Francisco.

References

Auffhammer, Maximilian. 2018. “Quantifying Economic

Damages from Climate Change.” Journal of Economic Perspectives 32(4), pp. 33-52.

Batten, Sandra. 2018. “Climate

Change and the Macro-Economy: A Critical Review.” Bank of England Staff Working Paper 706. January 12.

Campiglio, Emanuele, Yannis Dafermos, Pierre Monnin, Josh Ryan-Collins, Guido Schotten, and Misa Tanaka. 2018.

“Climate Change Challenges for Central Banks and Financial Regulators.” Nature Climate Change 8, pp. 462–8.

Climate Leadership Council. 2019. “Economists’ Statement on

Carbon Dividends,” as appeared in the Wall Street Journal, January 17, 2019.

Cœuré, Benoît. 2018. “Monetary Policy and Climate Change.” Speech at “Scaling up Green Finance: The Role

of Central Banks” conference hosted by Deutsche Bundesbank, Berlin, Germany, November 8.

Colacito, Riccardo, Bridget Hoffmann, Toan Phan, and Tim Sablik. 2018. “The

Impact of Higher Temperatures on Economic Growth.” FRB Richmond Economic Brief EB18-08, August.

Debelle, Guy. 2019. “Climate Change and the

Economy.” Speech at public forum hosted by Centre for Policy Development, Sydney, Australia, March 12.

Fried, Stephie, Kevin Novan, and William Peterman. 2019. “The Green

Dividend Dilemma: Carbon Dividends versus Double-Dividends.” Federal Reserve Board of Governors FEDS

Notes, March 8.

Gillingham, Kenneth, and James H. Stock. 2018. “The

Cost of Reducing Greenhouse Gas Emissions.” Journal of Economic Perspectives 32(4), pp. 53-72.

Heal, Geoffrey. 2017. “The Economics of the

Climate.” Journal of Economic Literature 55 (3), pp. 1046–63.

IPCC. 2018. Global Warming of 1.5°C. Intergovernmental Panel

on Climate Change Special Report. Geneva, Switzerland.

Lane, Timothy. 2017. “Thermometer

Rising—Climate Change and Canada’s Economic Future.” Speech to the Finance and Sustainability Initiative,

Montréal, Québec, March 2.

NGFS. 2018. First

Progress Report. Network for Greening the Financial System, October.

Olovsson, Conny. 2018. “Is

Climate Change Relevant for Central Banks?” Sveriges Riksbank Economic Commentaries 13 (November 14).

Scott, Matthew, Julia van Huizen, and Carsten Jung. 2017. “The

Bank of England’s Response to Climate Change,” Bank of England Quarterly Bulletin, Q2, pp. 98–109.

Tvinnereim, Endre and Michael Mehling. 2018. “Carbon Pricing and

Deep Decarbonisation.” Energy Policy 121, pp. 185-9, October.

USGCRP. 2018. Impacts, Risks, and Adaptation in the United States:

Fourth National Climate Assessment, Volume II. U.S. Global Change Research Program, Washington, DC.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org