Trend GDP growth has slowed about 2.3 percentage points to 1.7% since 1950. Different economic sectors have contributed to this slowing to varying degrees depending on the distinct trends of technology and labor growth in each sector. The extent to which sectors influence overall growth depends on the degree of spillovers to other sectors, which amplifies the effect of sectoral changes. Three sectors with slowing growth and linkages to other sectors—construction, nondurable goods, and professional and business services—account for 60% of the decline in trend GDP growth.

The current economic expansion has been notably long but has also been characterized by relatively slow growth (see Fernald et al. 2018). However, the growth rate in GDP has been declining throughout the post-World War II era. While the average growth rate from 1950 to 2016 was 3.3% per year, splitting the full period into smaller samples shows a general downward trend. For example, from 1950 to 1965 the average growth rate was 4.5% per year. This moderated to between 3-4% from 1966 to 2000, and fell to around 1.7% average growth since 2000. Therefore, the trend in GDP growth rates appears to have been declining for decades.

In this Economic Letter, we summarize our recent research (Foerster et al. 2019) that breaks this slowing in trend growth into changes at the sectoral level and studies which sectors play key roles in the decline. The main drivers of growth across sectors are technology and labor, which follow different trends in each sector. Moreover, sectors do not exist independently within the economy but instead have spillovers due to linkages in the production process. As a result, changes in trend productivity or labor growth in one sector propagate to different degrees to other sectors and therefore affect trend GDP growth to varying extents. Our estimates imply that trend GDP growth has declined 2.3 percentage points since 1950, consistent with the period averages. Of this decline, 60%, or 1.4 percentage points, is explained by slower trend growth of productivity and labor input in three sectors: construction, nondurable goods, and professional and business services. These three sectors account for a large share because of their slowing growth individually but also due to the extent of their spillovers.

Measuring sectoral trend growth

Economic theory suggests that two factors are key drivers of economic growth. The first is increases in total factor productivity (TFP), a broad measure of the productivity of the inputs used in a sector. The second is increases in labor input, that is, hours worked adjusted for the influence of education and experience levels on worker productivity. These growth rates differ, sometimes drastically, across sectors. As a first step, we use a statistical model to isolate trends in the growth rate of productivity and labor. We then determine the extent to which sector-specific versus common factors account for each sector’s change. We separate growth across sectors into four components: a common trend across sectors, sector-specific trends, a common temporary change across sectors, and sector-specific temporary changes. Our analysis focuses on the long-term rather than temporary changes, so we consider how the first two—common and sector-specific trends—affect GDP growth. We then isolate which sector-specific trends play the largest role in explaining slowing GDP growth.

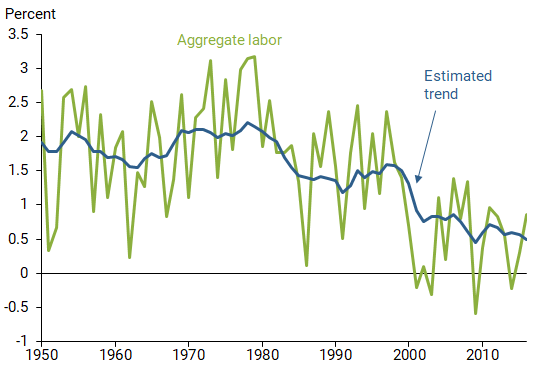

Figure 1 shows the annual growth rate in labor aggregated across sectors (green line) and the estimated trend growth rate from our statistical model designed to remove temporary movements from more persistent ones (blue line). The trend shows a clear downward trajectory over time, especially in recent years, in total dropping from about 2% to around ½%. Changes in this trend reflect both common and sector-specific factors. Common factors are those that affect all sectors, although possibly to varying degrees; these could include changes in labor force participation among women and baby boomers or changes in the education level of the overall workforce. Sector-specific factors are those that affect only a given sector, which could include shifting worker characteristics like the need for higher skill levels in a given sector. Put together, these factors contributed to relatively high growth early in the sample that abated after 1980 and dropped notably around 2000.

Figure 1

Aggregate labor growth and estimated trend

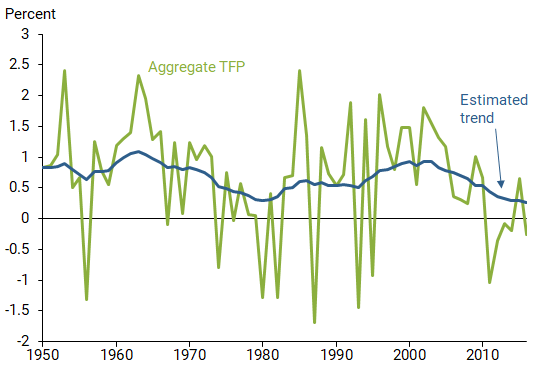

Figure 2 shows similar results for TFP growth. The changes in annual TFP growth fluctuate around a slow-moving trend that fluctuates—falling until about 1980, rising until the 2000s, and then falling again. Over the entire sample, it gradually declines around 0.5 percentage point. Again, this trend reflects both common and sector-specific factors. Common factors might include general-purpose technologies like computers, while sector-specific factors could be advances in production techniques that affect only a given sector.

Figure 2

Aggregate TFP growth and estimated trend

The effect of sectors on trend GDP growth

Given the declines in trend growth for TFP and labor, we next analyze to what extent that slower growth matters for declining trend GDP growth. In addition, since sector-specific trends in TFP and labor played an outsized role in accounting for the aggregate trend, we are interested in determining which sectors, if any, had particularly notable effects.

To translate trends in TFP and labor into trends in GDP, we rely on a conventional multisector economic model. The model uses growth in TFP and labor in each sector as inputs and produces the implied growth in value added at the sectoral level; we then aggregate these sectoral value-added results to find an implied measure of GDP growth. By considering only our estimates of trend growth shown in Figures 1 and 2, we can extract an estimate of trend GDP growth.

The economic model considers the effects of different sectors and their linkages in the production process. More specifically, each sector produces output that goes towards consumption by households, intermediate material inputs used in other sectors’ production, and investment goods. The linkages created by sectors using each other’s materials and investment products generates a propagation mechanism for the drivers of growth. If productivity growth falls in one sector, for example construction, that makes it relatively harder for other sectors to get intermediate material inputs and investment goods from construction, which will slow growth in the indirectly affected sectors, such as durable goods. If the durable goods sector then grows more slowly, other sectors such as utilities will have a harder time obtaining durable goods materials and investment products, hence utilities will grow more slowly, and so on. These multiple layers create feedback and spillover effects that depend on the relative importance of each sector as a supplier of intermediate materials and investment products.

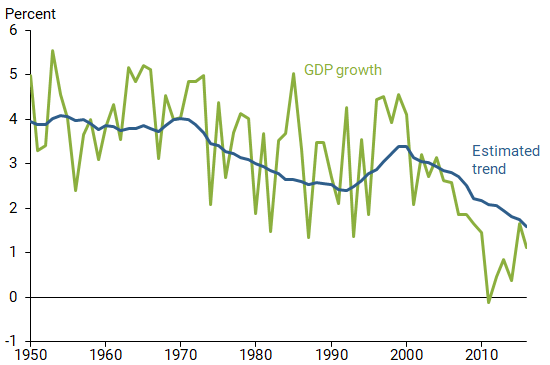

Figure 3 shows annual GDP growth (green line), along with the model-implied estimate of trend GDP (blue line). The annual growth rate of GDP shows significant fluctuations. The model estimate of trend growth, which we construct from the estimates of trend TFP and labor growth shown in Figures 1 and 2, looks similar to a moving average and highlights the decline since 1950. The trend estimate was around 4% in 1950 but steadily declined until a period of accelerating growth during the 1990s. Starting in 2000, the trend declined steadily again to the most recent estimate of 1.7%. We conclude from this estimate that trend GDP growth declined 2.3 percentage points from 1950 to 2016.

Figure 3

Annual GDP growth and estimated trend

To study which sectors play important roles in the declining trend, we incorporate a measure of the cumulative effect of each sector on GDP growth based on the economic model. Importantly, this measure includes direct and indirect effects. The direct effect is the share of each sector in total GDP. This highlights that slowing sectoral growth directly causes a decline in GDP growth based on the relative size of a sector, with bigger sectors having more pronounced effects. The indirect effect is the cumulative influence a sector has on other sectors through linkages in the production of intermediate and investment goods. These indirect channels highlight that slowing sectoral growth indirectly causes a decline in GDP growth based on how influential a sector is in the production of other sectors, with the more important sectors having more pronounced effects. A more detailed analysis of these direct and indirect sectoral multiplier effects is in Foerster, LaRose, and Sarte (2018).

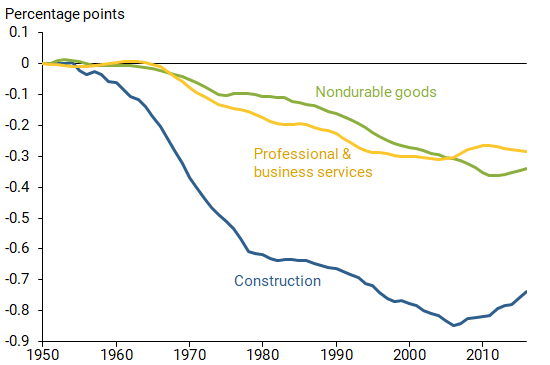

The effects of changing sectoral trends on trend GDP growth then depends on the interaction between two features: to what extent has each sector’s trend growth rate changed, and to what degree do those changes amplify across sectors. To identify which sectors account for large portions of the decline in trend GDP growth requires determining which sectors have both large declines in their own trend and relatively large sectoral multipliers. There are three such sectors: construction, nondurable goods, and professional and business services. Construction is relatively important to other sectors because it produces buildings and other structures that make production possible. Nondurable goods are important as intermediate inputs in the production process for many other sectors. Finally, professional and business services includes a range of activities such as accounting, management, and janitorial work that are used intensively by other sectors.

Figure 4 shows the contribution of each of the three key sectors to the 2.3 percentage point decline in trend GDP growth. Construction plays the largest role in this slowdown, as slowing sectoral TFP growth over that time and a relatively high importance as a supplier of investment goods imply a contribution of about ¾ percentage point, or about 30% of the decline. Of this decline, only about a quarter is due to direct effects on GDP, while three-quarters is due to indirect effects on other sectors. Nondurable goods and professional and business services each contributed about 0.3 percentage point to the decline, with direct effects accounting for about a quarter of the nondurable goods contribution and about four-tenths of the professional and business services contribution.

Figure 4

Contribution of select sectors to trend GDP growth

From our estimates, we conclude that these three sectors are responsible for about 1.4 percentage points, or about 60%, of the decline in trend GDP growth, and direct and indirect channels both played contributing roles.

Conclusion

Trend GDP growth declined by 2.3 percentage points from 1950 to 2016. Our estimates of the drivers of growth—TFP and labor—indicate that sector-specific trends play an important role in explaining aggregate trends. Using a macroeconomic model that accounts for linkages between sectors, we examine which sectors had particularly important influence on the decline in GDP growth, due not only to their slowing growth but also the extent of spillovers across sectors. The estimated decline in trend growth in the construction sector alone accounts for 30% of the decline in trend GDP growth. Taken together, construction, nondurable goods, and professional and business services account for about 60% of the total decline in trend growth.

Andrew Foerster is a research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Andreas Hornstein is a senior advisor in the Research Department of the Federal Reserve Bank of Richmond.

Pierre-Daniel Sarte is a senior advisor in the Research Department of the Federal Reserve Bank of Richmond.

Mark Watson is a professor of economics and public affairs at Princeton University.

References

Fernald, John, Robert E. Hall, James H. Stock, and Mark W. Watson. 2018. “The Disappointing Recovery in U.S. Output after 2009.” FRBSF Economic Letter 2018-04 (February 12).

Foerster, Andrew, Andreas Hornstein, Pierre-Daniel Sarte, and Mark Watson. 2019. “Aggregate Implications of Changing Sectoral Trends.” FRB San Francisco Working Paper 2019-16, May.

Foerster, Andrew, Eric LaRose, and Pierre-Daniel Sarte. 2018. “Idiosyncratic Sectoral Growth, Balanced Growth, and Sectoral Linkages.” FRB Richmond Economic Quarterly 104(2), pp. 79–101.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org