The Earned Income Tax Credit (EITC) substantially subsidizes earnings for low- to moderate-income families with children in the United States. Research has established that the EITC has positive short-term effects on the employment of less-educated single mothers and reduces overall poverty. The EITC may also generate higher earnings in the long run, as the short-run positive employment effects for low-skilled women accumulate into greater labor market experience that makes them more productive.

The Earned Income Tax Credit (EITC) fundamentally differs from U.S. cash welfare programs, which provide income support to people who are not working or have insufficient earnings. In contrast, the EITC subsidizes earnings, encouraging more people to work. The subsidy is higher for families with children, particularly those with lower incomes; in practice, these families are more likely to be headed by single women.

The EITC encourages work by raising the effective wage a person earns in the labor market. Indeed, extensive research establishes the positive effects of the EITC on the employment of low-skilled single mothers (see, for example, Meyer 2010). Moreover, because it targets low-income families well, it is effective at reducing poverty, both through direct income transfers (Hotz and Scholz 2003) and work incentives (Neumark and Wascher 2011). In the research described in this Letter, we explore yet another potential benefit of the EITC.

The long-standing theory of human capital suggests that the accumulation of training and experience from working leads to higher productivity and, hence, higher wages (Mincer 1974). Moreover, the effect on earnings may be even stronger, because the higher wages generated in the long run create an incentive to work more hours. Acting through these channels, the pro-employment effects of the EITC suggest that it may also generate higher earnings in the long run, as the short-run effects on low-skilled women accumulate into greater labor market experience that makes them more productive. In recent research (Neumark and Shirley 2017), we provide the first evidence of the long-run effects of the EITC on the earnings of low-skilled women.

The Earned Income Tax Credit in practice

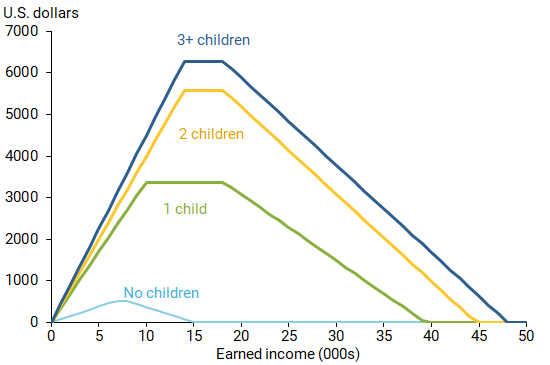

The EITC subsidizes a family’s earnings based on family income and number of children; the credit rapidly phases in as earned income increases from zero and gradually phases out at higher levels. Figure 1 displays the EITC schedules for 2016, the last year of our data, for different family incomes and numbers of children. As earned income rises from $0 for a low-income family, the EITC’s “phase-in” subsidy provides 34%, 40%, and 45% of earnings for families with one, two, and three or more children, respectively.

Figure 1

Federal EITC payments to families by income level

Eventually, the EITC payment reaches a maximum, shown by the flat regions in Figure 1. In 2016, the maximum credits for families with one, two, and three or more children were $3,373, $5,572, and $6,269, respectively. For those with two or more children, the maximum credit was first reached at earnings of $13,930. After the plateau, the credit phases out at about half the rate it phased in until a family is no longer eligible for EITC payments.

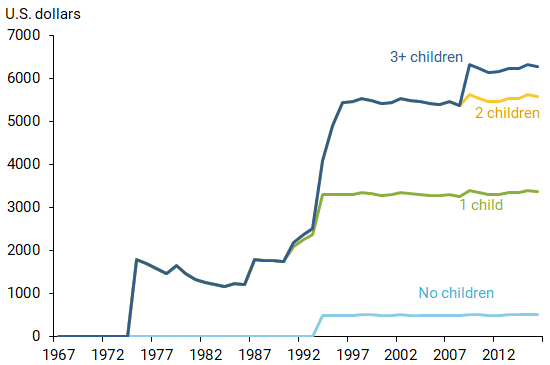

In its early years, the federal program was much less generous, paying benefits only to families with children, with no adjustment based on number of children. Figure 2 graphs (in 2016 dollars) the maximum credits by number of children since the program began in the mid-1970s. Today, in addition to the generous federal program, around half of states provide their own supplements to the EITC, usually as a fixed percentage of a tax unit’s federal EITC payment.

Figure 2

Federal EITC maximum credits according to family size

For women who would not work absent the EITC, the theory of labor supply unambiguously predicts that a more generous credit—in particular a higher phase-in rate—makes them more likely to work. Evidence on the short-run effects of the EITC confirms this prediction. For women who are already working, the extra income as well as the higher effective tax rate on the downward-sloping part of the EITC schedule suggest that some women will reduce their work hours, especially in dual-earner households. Empirical research generally bears out both of these predictions, although evidence of married women reducing work hours is not strong statistically (Eissa and Hoynes 2004). Here we focus primarily on the positive employment incentives.

Estimating long-run effects of the EITC on low-skilled women

Our empirical approach requires long-term data on women, starting with young adults when they first begin working and as they start to have children and first experience the labor supply incentives of the EITC. We continue to track them until they are mature adults, when the long-run effects of the EITC would be more evident. In particular, we study women’s exposure to the EITC from ages 22 to 39, then use outcomes at age 40 to estimate long-run effects. We use long-run data in the Panel Study of Income Dynamics (PSID) from its inception in the late 1960s through the most recent data covering 2016.

We also need to track their state of residence in each year so we can assign the relevant state EITC parameters. The work incentives are more generous, and thus more relevant, for women with children. In addition, the predicted effects are likely to vary with marital status, increasing employment for unmarried women and reducing hours for married women. Thus, we also track whether they have children and their marital status in each year.

To account for all of these dimensions, we create variables that capture average differences in the generosity of the EITC for which women were eligible when they were unmarried or married and when they had children or did not have children, and further differentiate by whether the children were school age. The generosity measure we use for the EITC is the maximum credit, although results using phase-in rates are virtually the same. With this approach, our statistical models estimate the long-run effects of the EITC by comparing women who are similar in many dimensions but faced varying generosity of the EITC, for example unmarried women with and without children.

Results

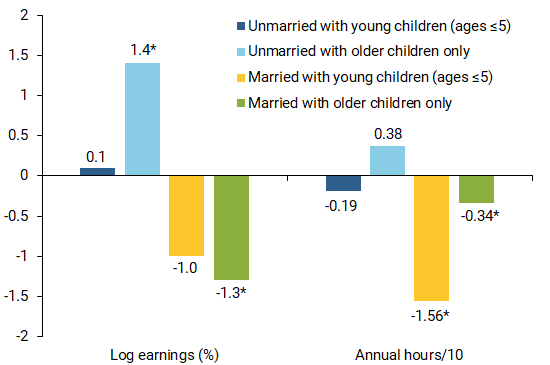

There are a number of different results to report, including estimates depending on long-run exposure to the EITC when unmarried or married and with or without children. We estimate models for four outcomes at age 40: employment, wages, earnings, and hours. For this Letter, we focus on the effects on earnings and hours, summarized in Figure 3.

Figure 3

Effects from one-year $1,000 increase in maximum credit

Notes: Estimates are computed for exposure at ages 22-39, with outcomes measured at age 40 using data from the Panel Survey of Income Dynamics. Bars marked with * indicate statistical significance at the 5% or 10% level.

We find higher earnings from exposure to a more generous EITC for unmarried women with children. Improvements in long-run earnings are consistent with short-run positive employment effects of the EITC translating into higher earnings at later ages, in part through accumulated work experience. The estimated effect is not statistically significant for exposure when children are younger than school age, but it is over ten times as large and statistically significant when children are of school age.

In contrast, married women who are exposed to a more generous EITC when they have children appear to have lower long-run earnings, regardless of the age of the children when exposed, though only the estimate for school-age children is statistically significant. The estimated absolute value of the magnitude is similar to the effect of exposure to a more generous EITC for unmarried women with school-age children, but negative rather than positive.

The magnitudes displayed in Figure 3 come from using the estimates from our models to calculate the implied long-run effects of a one-year, $1,000 (in 2016 dollars) increase in the maximum credit, which corresponds to about a 20% increase relative to its 2016 value. For unmarried women with school-age children, the implied effect is 1.4% higher earnings; for married women, the estimated effect is negative regardless of age of children, but larger for women who only have school-age children, with 1.3% lower earnings.

For hours, the most notable result is the lower number of hours worked at age 40 by women exposed to a more generous EITC when they were married with young children. Translating this into the effect of one year of exposure to a $1,000 higher maximum credit when children were young, the implied impact is a reduction of 15.6 hours. This effect is generated by fewer work hours for those working, rather than by fewer women working.

Some of these estimates may seem small, but they compute the effects of a one-year, $1,000 increase in the maximum credit. We can use the model to estimate the effects of a permanent increase of this size over the entire 22-39 age range, to get an idea of the long-run effects from making the EITC substantially more generous. It is a bit more complicated to estimate these effects, since we need to make an assumption about the ages women married and had children. To do this more simply, we compare women who had two children early—at ages 22 and 24—and were either married or unmarried the entire time. We find effects that are roughly ten times as large as those in Figure 3.

Our research also considers a number of potential reasons we might fail to estimate the true effects of the EITC. We rule out several alternative explanations, including that our effects are driven by the EITC influencing marriage and childbearing directly, as well as that women with different work behaviors migrate across states based on EITC differences.

Our estimates are largely consistent with expectations: theory predicts and existing evidence establishes that the EITC boosts current employment of unmarried women with children. Through the effects on human capital, this would imply higher earnings from long-run exposure to a more generous EITC. The EITC is also more likely to reduce work hours among married women with children, which would have the opposite long-run effect. Although the evidence on short-run reductions in hours for married women is weaker, these small effects could accumulate into larger long-run effects.

Implications

Our results support the conclusion that a more generous EITC does more than simply boost employment of low-skilled, single mothers in the short term—which existing research has already established. Indeed, long-term exposure to a more generous EITC appears to boost the earnings of this group in the long run. Thus, the EITC may have more benefits beyond just the short-run employment-increasing and poverty-reducing effects documented in past research.

In addition, policymakers and the public are concerned with low wages at the bottom of the wage distribution, which exacerbate earnings inequality. Long-run effects of the EITC that increase earnings of low-skilled single mothers may help address this problem for some workers.

David Neumark is Distinguished Professor of Economics and Co-Director of the Center for Population, Inequality, and Public Policy at University of California, Irvine, and a Visiting Scholar at the Federal Reserve Bank of San Francisco.

Peter Shirley is a Research Associate at the Luxembourg Institute of Socio-Economic Research.

References

Eissa, Nada, and Hilary Williamson Hoynes. 2004. “Taxes and the Labor Market Participation of Married Couples: The Earned Income Tax Credit.” Journal of Public Economics 88(9-10), pp. 1,931–1,958.

Hotz, V. Joseph, and John Karl Scholz. 2003. “The Earned Income Tax Credit.” In Means-Tested Transfer Programs in the United States, ed. R. A. Moffitt. New York: Russell Sage Foundation, pp. 141–198.

Meyer, Bruce D. 2010. “The Effects of the Earned Income Tax Credit and Recent Reforms.” In Tax Policy and the Economy, Volume 24, ed. J.R. Brown. Chicago: University of Chicago Press, pp. 153–180.

Mincer, Jacob. 1974. Schooling, Experience, and Earnings. Cambridge, MA: National Bureau of Economic Research, Inc.

Neumark, David, and Peter Shirley. 2017. “The Long-Run Effects of the Earned Income Tax Credit on Women’s Labor Market Outcomes.” NBER Working Paper 24114.

Neumark, David, and William L. Wascher. 2011. “Does a Higher Minimum Wage Enhance the Effectiveness of the Earned Income Tax Credit?” Industrial and Labor Relations Review 64(4), pp. 712–746.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org