The COVID-19 pandemic is causing severe disruptions to daily life and economic activity. Reliable assessments of the economic fallout in this rapidly evolving situation require timely data. Existing sentiment indexes are useful indicators of current and future spending but are only available with a lag or have a short history. A new Daily News Sentiment Index provides a way to measure sentiment in real time from 1980 to today. Compared with survey-based measures of consumer sentiment, this index shows an earlier and more pronounced drop in sentiment in recent weeks.

The COVID-19 pandemic is causing severe disruptions to daily life and economic

activity in the United States and around the world. These ruptures were

immediately evident in financial markets, with equity prices declining sharply

and market volatility spiking. It is also readily apparent that consumer

spending in sectors like leisure and hospitality is falling dramatically due

to shelter-in-place and other social distancing measures being imposed across

the country.

Assessing the timing and magnitude of the economic fallout in this rapidly

evolving situation has been hampered by the low frequency and lagged

availability of most macroeconomic data. In particular, so-called hard data

such as payroll employment, personal income, consumer spending, and business

investment are published with lags of weeks or months. Analysts and

policymakers are particularly interested in how consumer and business

sentiment is holding up right now given the well-documented links between

sentiment and economic activity (see, for example, Carroll, Fuhrer, and Wilcox

1994, Benhabib and Spiegel 2020, and Shapiro and Wilson 2017). Available

survey-based sentiment indexes are either low frequency, which limits their

usefulness in times of sudden change, or have a short history, which prevents

comparisons with past episodes.

In this Letter, we discuss the newly developed Daily News

Sentiment Index that provides real-time data from 1980 to today. The index was

developed and analyzed in Shapiro, Sudhof, and Wilson (2020). This daily index

is highly correlated historically with the monthly survey-based

University of Michigan Index of Consumer Sentiment and the Conference Board’s

Consumer Confidence Index.

Our Daily News Sentiment Index began falling sharply in January of this year,

coinciding with increasing news coverage of the coronavirus disease 2019

(COVID-19). This change appeared two months earlier than in the survey-based

sentiment measures. The decline in March was especially steep, consistent with

the large drop in consumer sentiment indexes in March.

Measuring news sentiment

Sentiment analysis is a rapidly developing field of natural language

processing and is now widely used in an array of business applications, such

as social media, algorithmic trading, customer experience, and human resource

management. The process allows one to directly quantify the emotional content

from any set of text. There are two general approaches. The first, known as

the lexical approach, relies on a predefined list of words associated with an

emotion, referred to as lexicons. For example, sentiment lexicons typically

classify words into three categories: negative, neutral, or positive. The

second, more nascent approach relies on machine-learning (ML) techniques to

predict the sentiment of a given set of text. ML techniques can, in principle,

learn sentiment weights for words and even entire phrases, then use those

weights to measure the sentiment of the given textual passage. The drawback of

the ML approach is that it requires large training data sets labeled for the

terms that are specific to the domain of interest—for example, business texts

or social media posts—which are time-consuming and expensive to construct.

The study by Shapiro, Sudhof, and Wilson (2020, hereafter SSW), constructs

sentiment scores for economics-related news articles using a lexical approach.

It uses a historical archive of news articles from 16 major U.S. newspapers

compiled by the news aggregator service LexisNexis. The newspapers cover all

major regions of the country, including some with extensive national coverage

such as the New York Times and the Washington Post.

SSW selected articles with at least 200 words where LexisNexis identified the

article’s topic as “economics” and the country subject as “United States.”

Combining publicly available lexicons with a news-specific lexicon constructed

by the authors, the study develops a sentiment-scoring model tailored

specifically for newspaper articles.

To assess the model’s accuracy, the authors compared sentiment scores from

this hybrid lexical model with human-provided sentiment scores for a random

sample of 800 news articles. These latter scores were generated by a team of

research assistants at the Federal Reserve Bank of San Francisco, who were

asked to rate articles on a scale of 1 to 5, from very negative to very

positive. The SSW hybrid lexical model was strongly correlated with the human

scores, performing better than any single lexical model and similar to or

better than models constructed using existing machine-learning techniques.

Comparing news sentiment with survey-based consumer sentiment

SSW next aggregated the individual article scores into daily and monthly

time-series measures of news sentiment, relying on a statistical adjustment

that accounts for changes over time in the composition of the sample across

newspapers. In this Economic Letter, we extend and augment the

SSW daily sentiment measure in two ways. First, we update the set of news

articles from LexisNexis to the present, since the news archive used in SSW

was only through mid-2015. Second, because the day-to-day fluctuations in the

sentiment measure tend to be noisy, we construct a smoothed daily index as a

trailing weighted average of the raw data, with weights that decline

geometrically with the length of time since the article’s publication. This

weighted average is analogous to how capital stocks are generally measured

from past vintages of investment: older investments contribute less according

to an assumed depreciation rate. We assume a depreciation rate of 5%; that is,

with each passing day, articles become 5% less relevant for today’s sentiment.

Our results in this Letter are not particularly sensitive to the exact

depreciation rate used.

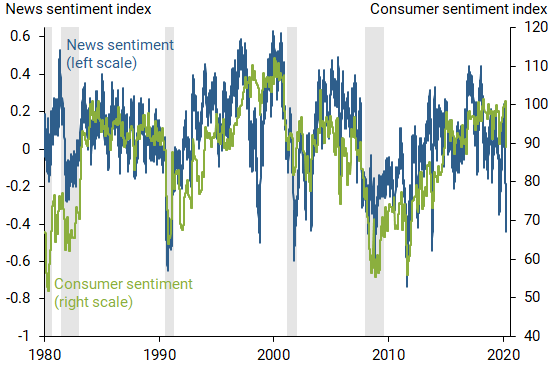

Figure 1 shows the resulting Daily News Sentiment Index over time (blue line).

Updates to this index are provided regularly on the San Francisco Fed’s

new data page. Figure 1 also includes the University of Michigan’s Index of Consumer

Sentiment, which is derived from a survey and is available at a monthly

frequency (green line). For both indexes, higher values indicate more positive

sentiment. Though the units of the two indexes are not directly comparable, it

is interesting to consider how each index has moved in relation to the

business cycle and around the time of major events. It is also interesting how

each index has moved recently, compared with responses to past events.

Figure 1

Daily news sentiment versus monthly consumer sentiment

Note: Moving average of daily news sentiment; see Shapiro, Sudhof, and

Wilson (2020) for methodology. Gray bars indicate NBER recession dates.

Source: Daily News Sentiment Index and Michigan survey.

The news sentiment index correlates strongly with the survey-based consumer

sentiment measure, and both are strongly procyclical, dipping during

recessions and rising during economic expansions. We found similar results

using the Conference Board’s Consumer Confidence Index (not shown). The news

sentiment index also tends to move with key historical events that have

affected economic outcomes and financial markets, such as the start of the

first Gulf War in August 1990; the Russian financial crisis in August 1998;

the terrorist attacks of September 11, 2001; the Lehman Brothers bankruptcy in

September 2008; and the October 2013 federal government shutdown. So far in

the recent daily results, the news sentiment index has not yet fallen to the

low points of the past three recessions, though it may well fall further in

the days and weeks ahead.

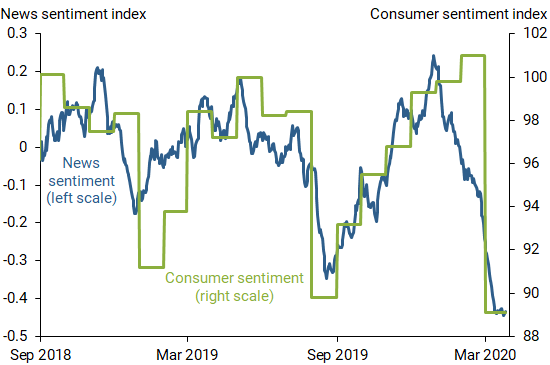

Sentiment in the time of COVID-19

Figure 2 zooms in on the last 18 months of data from Figure 1 to focus on the

most recent movements in sentiment. The Michigan Consumer Sentiment Index

remained elevated through February. However, March saw the fourth largest

one-month decline in the index since 1980. The Daily News Sentiment Index, on

the other hand, shows a sharp drop in sentiment beginning in early January and

steepening further in the first two weeks of March.

Figure 2

Sentiment indexes for past 18 months

Note: Moving average of daily news sentiment; see Shapiro, Sudhof, and

Wilson (2020) for methodology.

Source: Daily News Sentiment Index and Michigan survey.

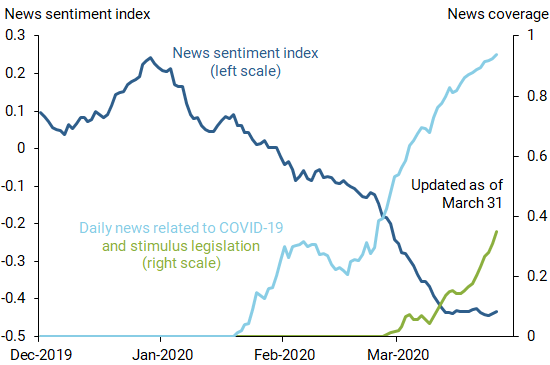

How much of the drop in news sentiment in recent weeks can be attributed to

the COVID-19 outbreak? To address this question, Figure 3 shows our index

(dark blue line) along with a measure of COVID-19 news coverage (light blue

line). For the latter, we calculate the fraction of economics-related news

articles that contain the terms “coronavirus” or “COVID-19.” The series in

Figure 3 is a trailing-average of this fraction, with weights that decline

geometrically for older articles, analogous to how we constructed the news

sentiment index. Articles mentioning the coronavirus and COVID-19 began around

January 20 and then rapidly increased. By late March, the percentage of

economics-related news articles mentioning the virus reached an astounding

95%. The figure clearly shows that the decline in sentiment through mid-March

coincided with the increased coverage of COVID-19. More recently, the news

sentiment index has flattened, coinciding with the rise in news coverage

related to fiscal stimulus legislation (green line). There was also a

temporary decline in sentiment in the first half of January, which was due to

the flare-up of U.S.-Iran hostilities and related disruptions in the oil

market.

Figure 3

News sentiment and growth in news of COVID-19

Note: Moving average of daily news sentiment; see Shapiro, Sudhof, and

Wilson (2020) for methodology.

Conclusion

The new Daily News Sentiment Index introduced in this Letter can

be especially useful in times of sudden economic change as we are experiencing

now. This index is constructed at a daily frequency from 1980 to today. By

contrast, existing survey-based sentiment indexes have either low frequency or

a short history. The Daily News Sentiment Index is highly correlated with

survey-based measures of consumer sentiment, but it shows an earlier and more

pronounced drop in recent weeks. This rapid decline in news sentiment has

coincided with the increasing news coverage of COVID-19.

Studies have documented a strong link between sentiment and subsequent

economic activity, especially business investment and consumer spending. For

example, Benhabib and Spiegel (2019), using state-level data, find that a

one-standard-deviation drop in consumer sentiment as measured by the Michigan

survey would be expected to result in a 2.3% drop in personal consumption

expenditures. The drop over the past two months in the Michigan Consumer

Sentiment Index has, in fact, been very close to one standard deviation. It is

therefore worth noting, for comparison, that our Daily News Sentiment Index

has fallen over the past two months by a little over three standard

deviations, which may portend a steep decline in consumer spending. It is

important to note that the current episode is particularly unique. Consumer

spending at the moment has been depressed for reasons beyond low sentiment. In

particular, government-imposed social distancing measures are directly

inhibiting spending on many types of discretionary goods and services, such as

those associated with leisure and hospitality.

In the weeks and months ahead, it will be important to monitor news and

consumer sentiment to see how much further sentiment will fall and when it

will start to turn around.

Shelby R. Buckman is research associate in the Economic Research Department of

the Federal Reserve Bank of San Francisco.

Adam Hale Shapiro is

research advisor in the Economic Research Department of the Federal Reserve

Bank of San Francisco.

Moritz Sudhof is cofounder and chief executive officer at Motive Software.

Daniel J. Wilson is

vice president in the Economic Research Department of the Federal Reserve Bank

of San Francisco.

References

Benhabib, Jess, and Mark M. Spiegel. 2019. “Sentiments and Economic Activity:

Evidence from U.S. States.” The Economic Journal 129(618,

February), pp. 715–733.

Carroll, Christopher D., Jeffrey C. Fuhrer, and David W. Wilcox. 1994. “Does

Consumer Sentiment Forecast Household Spending? If So, Why?”

American Economic Review 84(5), pp. 1,397–1,408.

Shapiro, Adam H., Moritz Sudhof, and Daniel J. Wilson. 2020.

“Measuring News Sentiment.”

FRBSF Working Paper 2017-01.

Shapiro, Adam, and Daniel J. Wilson. 2020.

“What’s in the News? A New Economic Indicator.”

FRBSF Economic Letter 2017-10 (April 10).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org