Do extended periods of negative policy interest rates continue to encourage commercial bank lending? A large panel of European and Japanese banks provides evidence on the impact of negative rates over different lengths of time. Analysis suggests that both bank profitability and bank lending activity erode more the longer such negative policy rates continue, primarily due to banks’ reluctance to pass negative rates along to retail depositors. This appears to negate one of the main arguments for moving policy rates below the zero bound.

With U.S. policy rates back in the neighborhood of zero, there has been renewed discussion of the potential efficacy of negative monetary policy rates. However, Fed policymakers have expressed skepticism about lowering the federal funds rate into negative territory. Fed Chair Jerome Powell recently stated that “the [Federal Open Market] Committee’s view on negative rates really has not changed. This is not something we are looking at” (Reuters 2020). Meanwhile, Vice Chair John Williams has argued that guidance about the interest rate path or asset buying are more robust policy tools (Wall Street Journal 2020).

One long-standing reservation about negative policy rates is their potentially adverse impact on bank profitability and intermediation activity. It has been well-documented that negative rates squeeze net bank interest margins. Moving policy rates below zero typically push down all lending rates, reducing bank revenue. However, banks—with few exceptions—have been reluctant to alienate their household clients by paying negative nominal rates—effectively charging rather than paying interest—on standard deposits. As a result, banks’ revenue falls more than their funding cost, lowering lending profitability.

In this Economic Letter, we revisit the question of bank performance under extended negative policy rate episodes in foreign countries and assess recent evidence on bank activity. Our results indicate that both bank profitability and bank activity deteriorate over the course of negative rate episodes. In particular, while negative rates raise bank net income in the first year, they begin to drag on profits over time. We find this effect is statistically significant for the banks in our sample that have been under negative rates for the longest time. We also find that bank lending—which is often the motivation for negative policy rates—increases only during the first year under negative rates. Lending declines over the next two years, more than reversing any initial gains.

Evidence on negative rates

In a recent paper, Lopez, Rose, and Spiegel (2020, hereafter LRS) find that banks’ recent experiences under negative rates in terms of profitability have been relatively benign. While negative rates are associated with reduced net interest margins for banks, they appeared to have more than made up for those losses through gains in noninterest income, particularly capital gains on securities holdings as rates went negative. That paper cautions that bank profitability appeared to deteriorate over time, particularly due to the disappearance of early noninterest income gains. However, the periods of negative rates in that paper were too short to reach any definitive conclusions.

For this Letter, we use an expanded sample that contains evidence on more lengthy negative policy rate episodes. Moreover, our sample period is likely to be the longest one available that will be able to avoid the impact of the coronavirus pandemic coloring any conclusions about bank performance. Our analysis extends the large cross section of global banks in LRS (2020) from the Fitch global database, using the same method for accounting issues. We include annual data from 27 European countries and Japan from 2010 through 2018. The data set includes banks from four countries—Denmark, Japan, Sweden, and Switzerland—as well as the European Monetary Union (EMU) that maintained negative domestic policy rates at some point during our sample period.

Overall, our analysis examines over 39,000 annual observations for profitability and lending activity from more than 5,300 banks. In particular, relative to LRS (2020), our extended sample contains 2,854 additional observations for banks under extended durations of five years or more under negative policy rates.

As a control, our sample also includes banks from a number of European countries that do not experience negative rates. Because banks are under negative rates at different points in time, our analysis allows us to control for global economic conditions. We also control for characteristics of individual banking firms that don’t change over time; see an online appendix for more details.

To evaluate the impact of negative rates on bank profitability, we follow the approach detailed in LRS (2020). We run a regression analysis to evaluate the relationship between bank profitability and three indicators, in addition to the individual bank controls. First, we check an indicator of the presence of negative policy rates to isolate their effects. Second, we use an indicator of the length of time in years that banks have been under negative interest rates to capture the impact of the episode duration. Finally, we use the square of the duration of time that banks have been under negative rates to capture the degree to which the impact of negative rate duration increases over time.

Bank profitability under negative rates

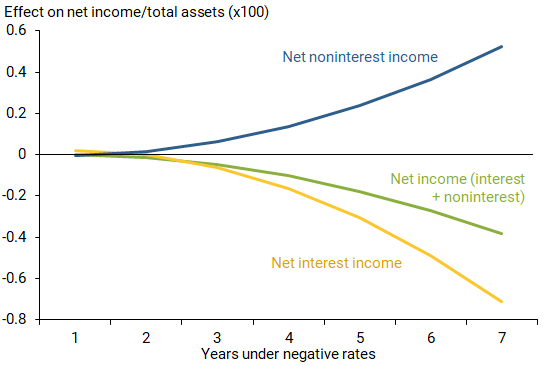

We first consider bank profitability under negative policy rates, looking at the impact on overall profitability, as well as a breakdown of profits from interest versus noninterest income. We measure all values as shares of a bank’s total assets to acknowledge differences in bank size. Our results based on point estimates are shown in Figure 1.

Figure 1

Negative nominal interest rate duration and bank income

Note: Point estimates for regression of net income/total assets on years under

negative nominal interest rates. See text and online appendix for details.

Coefficients multiplied by 100 for presentation, following LRS (2020).

As in LRS (2020), we initially find that banks experience modest increases in profitability under negative rates. While banks suffer losses on net interest income, due in part to their reluctance to pass negative interest rates along to retail depositors, they more than offset those losses through increases in profits on noninterest income. In particular, banks charge higher fees and experience capital gains on securities holdings when rates go negative.

However, the data clearly show that losses on interest income accelerate over time and begin to outweigh the gains from noninterest income. As a result, the impact on overall profitability falls below zero. Our regression analysis for the impact on overall bank profitability becomes negative on average with statistical significance after five years under negative interest rates; we detail our method in the appendix.

Impact of negative rates on lending activity

One primary motivation for using negative monetary policy rates is to stimulate bank lending activity through the “bank lending channel” (see, for example, Bernanke and Gertler 1995). All else being equal, lowering interest rates raises banks’ returns from loans relative to other investments, as funding costs tend to fall faster than lending rates. As a result, theory suggests that banks would respond to lower monetary policy rates by expanding lending to businesses and households.

This reasoning should include declines that push policy rates below zero. However, when rates are near the zero bound, banks have been reluctant to push rates on retail deposits below zero. As economies experience persistent periods of negative rates, some exceptions have emerged. Still, recent data demonstrate that retail commercial bank deposit rates generally appear to hit a hard limit at zero. This means that pushing policy rates below zero reduces bank revenue more than it reduces funding costs, reducing lending profitability.

Given the limited ability to substitute fees or other sources of revenue to recoup losses on net lending below the zero bound, the bank lending channel may be disrupted. If so, this channel may weaken, as found in Ulate (2019), or even reverse, as in Brunnermeier and Koby (2019). Moreover, as the duration of the negative rate period increases, banks may make more costly adjustments towards other investments and away from lending.

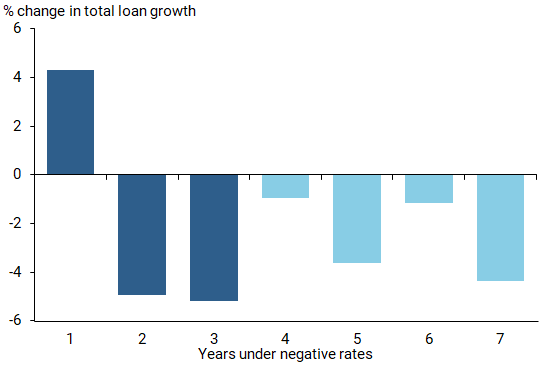

We evaluate the impact of negative rates on lending activity at the individual bank level by examining total bank lending. In addition to controls for bank and time fixed effects, we run a regression to understand how lending under negative rates changes depending on how many years it has been in place. We estimate a range of one to seven years of possible negative rate durations in our sample. Details of our method and results are also available in our appendix.

Figure 2 illustrates the estimated differences in total bank loan growth as a function of the duration of the negative interest rate policy. Our results confirm that bank lending expands 4.3% during the first year under negative interest rates. However, this growth more than reverses over the following two years, by 4.9% and 5.2% respectively. From year four on, our estimates are statistically insignificant but uniformly negative, with lending growth declining 2.5% on average.

Figure 2

Impact of negative policy rate duration on bank lending

Note: Dark blue bars reflect statistically significant results.

We concentrate on our results up to the fifth year under negative rates, because we have a large set of observations from EMU banks for those durations in our unbalanced sample; the banks in our sample with six to seven years under negative rates are less useful for cross-country comparison because they are all from Denmark. Over the fourth and fifth years under negative rates, bank lending declines 2.3% on average per year. These results differ qualitatively from a number of studies in the literature, which look at the lending impacts of negative versus positive rates without accounting for duration (see, for example, Demiralp, et al. 2019). Those studies generally find a positive impact of negative policy rates on lending.

Conclusion

In this Economic Letter, we revisit a large cross-country data set of banks from 27 countries, most of which experienced negative monetary policy rates during the previous decade. Our combination of countries that did and did not have negative rates, as well as countries entering negative rates at different points in time, allow us to analyze different experiences for individual banks and monetary policy regimes.

Our results suggest that banks can only mitigate losses on interest income through charging fees on deposits and enjoying capital gains on securities holdings for short periods of negative interest rates. As durations of negative policy rates lengthen, the gains from these adjustments become increasingly inadequate to offset the growing losses on interest income due to banks’ limited abilities to pass along negative rates to depositors. The result is that, as negative rates persist, they drag on bank profitability even more. Moreover, we find that banks expand lending only temporarily under negative rates. While lending initially increases under negative rates, our analysis implies that gains are more than reversed as negative rates persist.

Overall, our results suggest that caution is warranted when considering negative monetary policy rates to encourage additional bank lending. Under extended negative rate episodes, evidence shows that both bank profitability and bank lending activity decline. This calls into question one of the primary motivations for negative policy rates.

Remy Beauregard is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Mark M. Spiegel is a senior policy advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Bernanke, Ben S., and Mark Gertler. 1995. “Inside the Black Box: The Credit Channel of Monetary Policy Transmission.” Journal of Economic Perspectives 9(4, Fall), pp. 27–48.

Demiralp, Selva, Jens Eisenschmidt, and Thomas Vlassopoulos. 2019. “Negative Interest Rates, Excess Liquidity and Retail Deposits: Banks’ Reaction to Unconventional Monetary Policy in the Euro Area.” European Central Bank Working Paper 2283, May.

Lopez, Jose A., Andrew K. Rose, and Mark M. Spiegel. 2020. “Why Have Negative Nominal Policy Rates Had Such a Small Effect on Bank Performance? Cross Country Evidence.” European Economic Review 124, pp. 1–17.

Reuters. 2020. “Less than Zero? Fed’s Powell Shows No Love for Negative Rates.” May 13.

Ulate, Mauricio. 2019. “Going Negative at the Zero Lower Bound: The Effects of Negative Nominal Interest Rates.” FRB San Francisco Working Paper 2019-21.

Wall Street Journal. 2020. “Fed’s Williams: Economy Has Likely Seen ‘Low Point’ in Continuing Crisis.” June 30.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org