The onset of the COVID-19 pandemic and the unprecedented slowing of economic activity that followed caused severe disruptions to labor markets around the globe. In contrast to the United States, European Union countries funded short-time work programs to maintain jobs during a period of lockdown that was expected to be transitory. This succeeded in avoiding sharp increases in unemployment early in the recession. However, if the pandemic leads to a permanent reallocation of economic activity, short-time work programs may slow the process of workers moving from shrinking to growing sectors of the economy.

Policymakers in the United States and the European Union (EU) responded aggressively to the onset of the COVID-19 pandemic. Along with lockdowns and other measures to control the spread of the virus, they enacted programs to preserve jobs and businesses. U.S. policymakers focused largely on income support to households, such as expanded unemployment insurance, and on lending to sustain businesses and existing employment relationships, such as the Paycheck Protection Program. By contrast, EU countries have relied more extensively on work-sharing programs that reduce hours worked per employee—known as short-time work (STW)—to avoid outright job cuts.

To assess the potential impact of the STW policies, this Economic Letter compares labor market outcomes in the United States and the EU during the pandemic. We find that the STW policies commonly used in EU countries to prevent job losses resulted in significantly different paths for employment over the course of the past year from that for the United States. We conclude by noting that work-sharing policies can be beneficial when businesses are facing transitory and short-lived slowdowns in economic activity. However, these policies can also reduce incentives for businesses and workers to adjust to changing needs in the economy. If firms and sectors face permanent changes in demand, work-sharing policies may make businesses and workers slower to adapt and may ultimately be harmful to employment and the productive capacity of the economy in the longer run.

Short-time work programs in the EU

Since the pandemic began, EU countries have largely relied on short-term work programs to maintain current relationships between employees and employers. STW programs provide a wage subsidy for hours not worked at businesses experiencing a temporary slowdown in business activity. This subsidy, which may last up to a year, is usually paid directly to employees after firms have applied to the program and specified the expected reduction in hours worked.

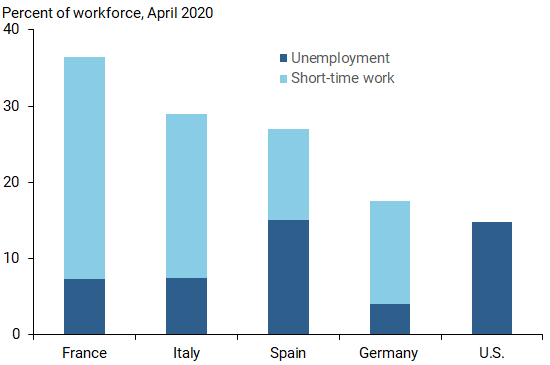

EU companies widely adopted STW programs during the pandemic. Nearly 30% of employees in France worked reduced hours on such a program in April 2020, along with just over 20% of employees in Italy, 13% in Germany, and 12% in Spain (light blue bars in Figure 1). The reliance on STW is much more extensive now than during the Great Recession of a decade ago, when it applied to approximately 5% of employees in Germany and Italy and 4% in France (Giupponi and Landais 2020).

Figure 1

Early pandemic effects on short-time work, unemployment

Note: Authors’ calculations from national statistical agency data.

The comparison in Figure 1 shows that the STW programs worked as they were intended. The initial lockdown was accompanied by a much smaller wave of layoffs and lower rise in unemployment in the EU than in the United States. The rate of unemployment in France, Italy, and Germany hardly changed during the lockdown. For instance, unemployment in France stood at 7.5% in February 2020 and 7.3% in April, while the corresponding rates in Germany were 3.6% and 4.0%. In stark contrast, unemployment in the United States, which had fallen to a historic low of 3.5% before the pandemic, immediately jumped to nearly 15% in April (dark blue bars in Figure 1).

Two contrasting paths for the labor market

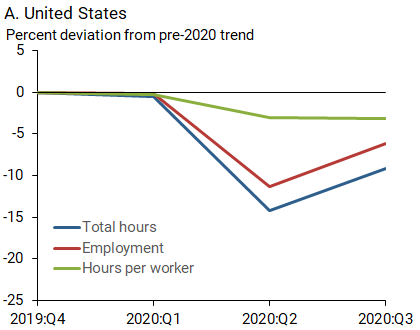

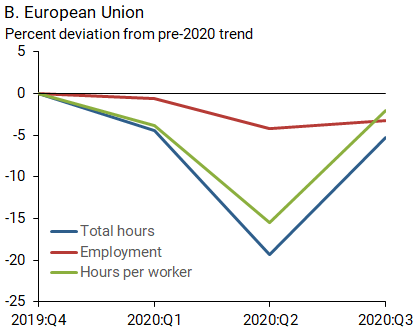

Movements in unemployment rates suggest the strict virus containment measures had a larger impact on economic activity in the United States than in the EU. However, combining the affected workforce from STW programs and unemployment suggests more similarity across these two regions than a comparison of job loss alone, as shown by the combined height of the bars in Figure 1. In fact, total hours of work—calculated as the product of the number of people employed and the number of hours worked per employee—have followed similar paths in the two regions during the pandemic. Figure 2 shows that total hours worked in the second quarter of 2020 fell 14% below their pre-pandemic trend in the United States and 20% below in the EU (blue lines). After the initial severe phase of containment measures eased, total hours recovered more rapidly in the EU than in the United States. By the third quarter of 2020, total hours were about 5% below the pre-pandemic trend in the EU, compared with 9% below the trend in the United States.

Figure 2

Effects of COVID-19 on total hours, employment, and hours per worker by region

Note: Percentage deviations from a pre-2020 deseasonalized trend. European Union reflects aggregated data for France, Germany, Italy, and Spain.

The use of STW programs in the EU helps explain the similar paths for total hours of work during the pandemic, despite the stark contrasts in unemployment rates in the two regions. Figure 2 also breaks down total hours of work into its component parts of employment and hours per employee. Employment (red lines) fell sharply in the United States but not in the subset of major EU countries: France, Germany, Italy, and Spain. U.S. employment fell 11% relative to trend in the second quarter and remained well below trend in the third quarter, whereas EU employment was only 3% below the pre-pandemic trend in the second and third quarters. Hours per worker (green lines) fell substantially in EU countries, dropping 16% below trend in the second quarter as expected, given the widespread adoption of STW programs. This was compared with only a 3% drop in the United States. Moreover, hours per worker recovered quickly in EU countries and were close to trend by the third quarter. It is also worth noting that these patterns did not occur during the Great Recession when STW policies were not as widely available and implemented.

Telework and economic activity

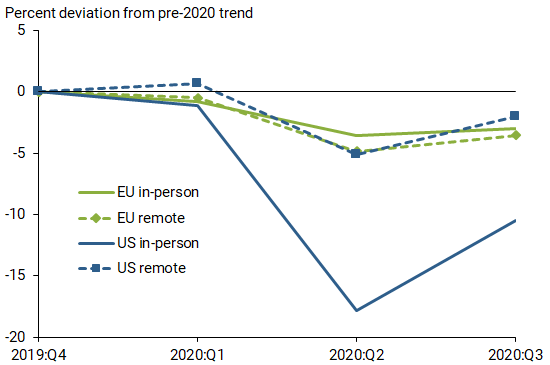

A unique feature of a pandemic economy are the restrictions imposed on in-person exchanges and work. This has reduced economic activity in general, though it has most severely affected sectors with limited ability to work remotely, also known as telework. The differences become apparent when we sort sectors by the degree to which employees can telework using a classification that largely follows the work of Dingel and Neiman (2020). We label sectors with a low ability to telework and require a physical presence of employees as “in person.” We label sectors with a high ability to perform work remotely as “remote.” We then select a cutoff proportion of jobs that can be performed remotely within a sector and use that to divide total employment equally across the two sectors before the onset of the pandemic.

Figure 3 shows the evolution of employment in the remote and in-person sectors during the pandemic in the United States and the European Union. U.S. employment displays the expected pattern: employment fell dramatically in the in-person sectors in the second quarter, about 17%, and remained 10% below its pre-pandemic trend in the third quarter (solid blue line). U.S. employment in remote sectors, on the other hand, shows more resilience against the COVID-19 shock with a 3% decline in employment (dashed blue line). This contrasts with changes in employment in the EU, where remote and in-person sectors display almost identical dynamics (solid and dashed green lines, respectively). On the one hand, the availability of STW subsidies helped preserve employment for in-person sectors in the EU. On the other hand, the persistent decline in employment in the United States for in-person sectors is likely to reflect a more permanent aftereffect on jobs from the COVID-19 shock. This may have implications for future employment trends in both regions.

Figure 3

COVID-19 and employment in remote and in-person sectors

Note: Percentage deviations from a pre-2020 deseasonalized trend. EU

reflects aggregated data for France, Germany, Italy, and Spain.

Implications for labor markets going forward

The pandemic has accelerated the shift of consumer spending away from in-person and toward online purchases. It may also have permanently shifted spending away from businesses that involve direct interaction with the public, such as airline travel, hotels, restaurants, and in-person entertainment (Barrero et al, 2020). In this sense, the COVID-19 pandemic represents a “reallocation shock” that requires labor to shift across different industries and occupations. Some of these shifts may be permanent, necessitating alterations to educational requirements and additional training for existing workers and new hires.

In the face of a such a reallocation shock, STW policies remove the incentives for workers to quickly transition out of struggling, low productivity firms and toward thriving, high productivity firms. This effectively reduces overall productive efficiency. In fact, Cooper et al. (2017) estimate that this misallocation led to significant losses in potential output in Germany following their use of STW policies during the Great Recession.

In addition, the ability and earnings consequences of switching industries or occupation depends on the worker’s type of human capital. Job protection policies—and by extension STW policies—increase the incentive to invest in human capital, or skills, that are specific to a particular industry, rather than general human capital, which are a set of skills that can be applied to a job in a new industry. This slows the process of labor reallocation (Wasmer 2006) and increases the earning costs of switching occupations. These considerations become even more stark for low-skilled workers who face greater retraining costs.

Conclusions

The EU’s short-time work programs during the pandemic recession preserved employment relationships by subsidizing workers’ wages. U.S. policy instead has focused on income support to households through, for example, expanded unemployment insurance programs under the CARES Act. Such income support to individuals facing job displacement may be preferable in the face of a shock that reallocates economic activity across different sectors of the economy and requires workers to move to new and growing businesses. The overall labor market implications of the COVID-19 pandemic will depend in part on how much labor reallocation is required to meet the demands of a changed economy and the set of policies used to support workers’ transitions to new sectors of business activity.

Jean-Benoît Eyméoud is an economist at the Banque de France.

Nicolas Petrosky-Nadeau is a vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Raül Santaeulàlia-Llopis is a Beatriz Galindo Senior Research Professor in Economics at UAB and affiliated research professor at the Barcelona GSE.

Etienne Wasmer is a professor of economics in the Social Science Division at NYUAD.

References

Barrero, José María, Nick Bloom, and Steven J. Davis. 2020. “COVID-19 Is Also a Reallocation Shock.” Brookings Papers on Economic Activity Conference Draft, Summer.

Cooper, Russell, Moritz Meyer, and Immo Schott. 2017. “The Employment and Output Effects of Short-Time Work in Germany.” National Bureau of Economic Research Working Paper 23688, August.

Dingel, Jonathan I., and Brent Neiman. 2020. “How Many Jobs Can Be Done at Home?” Journal of Public Economics 189 (September).

Giupponi, Giulia, and Camille Landais. 2020. “Subsidizing Labor Hoarding in Recessions: The Employment and Welfare Effects of Short Time Work.” CEPR Discussion Paper 13310.

Wasmer, Etienne. 2006. “General versus Specific Skills in Labor Markets with Search Frictions and Firing Costs.” American Economic Review 96(3), pp. 811–831.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org