The Federal Reserve has evolved since the “Great Inflation” of the 1970s. With new tools and a deeper understanding of the importance of transparency, it is better prepared to meet the dual mandate goals of price stability and full employment, even in challenging times. The following is adapted from remarks by the president of the Federal Reserve Bank of San Francisco to the Los Angeles World Affairs Council & Town Hall on February 23.

It’s hard to believe it’s been almost two years since COVID-19 hit our shores. And while it’s not fully behind us, we’ve come a long way, especially in the economy. Growth is up. Unemployment is down. And people are getting back to their lives.

But as anyone who has shopped, bought gas, or paid rent lately knows, inflation is high—higher than it has been in nearly four decades.

For some, this is a sign that price stability is at risk. That, absent aggressive action by the Fed, the economy will be propelled into a 1970s-style “Great Inflation.”

Like many of you, I lived through that time. I remember my parents’ daily complaints about rising prices and rising bills, and the hours-long waits at gas stations in the hot Missouri sun, stuck to the vinyl seats of our station wagon.

High and rising inflation made life harder. And there was no end in sight.

But the picture today looks different. And so does the Federal Reserve. We have evolved as an institution, and our understanding and tools have evolved as well. I’ll spend my time today talking about how this evolution makes us better prepared to meet our dual mandate goals of price stability and full employment, even in these challenging times.

Then…

Before I talk about what’s different this time, let me talk about what exactly happened during the Great Inflation. What was it like?

From about the mid-1960s through the early 1980s, American households faced an unrelenting rise in prices. The worst of it came during the 1970s, when the cost of living for the average family more than doubled. This pace was three times faster than it had been the previous decade, based on the consumer price index (CPI). The stress in our nation was palpable. Businesses and families lost confidence, and many struggled simply to make ends meet.

People wondered how it had happened.

The answer, of course, is complicated. But I will focus on a few factors that I think are particularly relevant for today’s discussion. (For an overview of research about the Great Inflation, see Lansing 2000 and Bryan 2013.)

The first has to do with fundamental economic changes and our inability back then to measure and understand them in real time.

For example, after decades of rapid postwar GDP growth, led by booming technological advancements and rising labor productivity, U.S. productivity growth had started to slow. This meant that the capacity of the economy to expand without spurring inflation was much more limited than it had been in previous decades (Basu and Fernald 2002).

At the same time, the labor market was changing. Young baby boomers were joining the labor force in large numbers and altering the age composition and the dynamics of the workforce. In particular, they were taking longer to find jobs and churning through more opportunities as they found their preferred path. This behavior, which is completely natural, increased the “steady-state” rate of unemployment, a benchmark policymakers used to judge how close the economy was to full employment and full capacity (Crump et al. 2019).

Looking back, it’s clear that policymakers missed some critical shifts. Without the data, tools, and focus on real-time monitoring, they—and macro forecasters more broadly—expected the economy to behave as it had before, for inflation to fall as the economy and labor force grew (DeLong 1997 and Taylor 1997). These views, in part, kept the Fed from acting forcefully to offset rising inflation (Clarida, Galí, and Gertler 2000; Orphanides 2003; Primiceri 2006; Romer and Romer 2013; and, for the role of political pressures in the Fed’s decision to keep policy accommodative, Weise 2012).

But the story doesn’t end there. The Fed’s policy misses were amplified and perpetuated by institutional factors and by its own communication strategy.

Let’s start with institutional factors. At the time, there was a very tight link between price and wage inflation. Many employment contracts included automatic cost-of-living adjustments, or COLAs, which meant that when prices went up, wages soon followed (Ragan and Bratsberg 2000). Firms then passed on these increased labor costs to prices, and so it went, again and again, in a self-perpetuating upward inflation spiral.

When two oil price shocks created even higher inflation, prices and wages grew in near lockstep. And here is where the Fed’s own communication practices exacerbated things.

The Fed and many central banks at the time held the view that transparency and communication were more costly than beneficial. Central bankers actively avoided sharing information, believing that such communications might constrain their ability to nimbly adjust policy, or even dilute its impact (Cukierman and Meltzer 1986, Bernanke 2007a).

Because of this, the Fed operated largely behind closed doors. The public became aware of Fed policy actions by watching how markets reacted following Federal Open Market Committee (FOMC) meetings. And the main source of information that market participants, households, and businesses had about the Fed’s commitment to price stability was what they could glean from incoming inflation data.

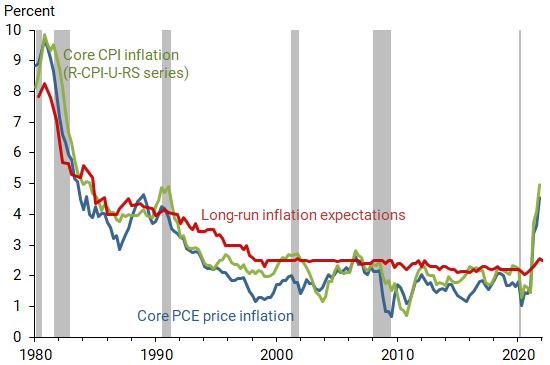

The result was predictable. And you can see it in Figure 1. The green and blue lines show two measures of actual inflation, and the red line shows inflation expectations.

Figure 1

Inflation: Actual versus expectations

Note: Gray bars denote NBER recessions. Long-run inflation expectations from Blue Chip (1980–1991) and Survey of Professional Forecasters (1991–present), median expected inflation over the next 10 years.

Sources: Williams (2006), Bureau of Economic Analysis, Bureau of Labor Statistics, Survey of Professional Forecasters, Blue Chip.

Clearly, the more inflation rose, the more consumers and businesses expected it to rise. As inflation moved up, so did inflation expectations (Cogley and Sbordone 2008 and Lansing 2009). These expectations of future inflation were then built into wage and price contracts.

Before long, inflation dynamics and future inflation were deeply intertwined with inflation psychology. And with the Fed offering little guidance or reassurance that it would do something about it, the situation snowballed.

It wasn’t until the Fed implemented a series of steep interest rate hikes that inflation finally started to recede.

…Now

Now inflation is high again and many are concerned that we could soon be facing another long and painful period, followed by another long and painful correction.

But that’s not what I see. Let me explain.

You’ve heard many, including me, talk about how inflation itself is different this time. It’s been pushed up by pandemic-related imbalances between policy-supported demand, which has remained robust, and COVID-disrupted supply, which has been slow to recover. Both of these factors should recede as the pandemic weakens its grip.

And the economy is also different. There are weaker links between wage and price inflation, greater global price competition, and a number of longer-term structural factors, including an aging population, that will continue to exert downward pressure on growth and inflation once the pandemic is behind us (Eichengreen 2015, Gordon 2015, and Laubach and Williams 2016).

But these are not the differences that matter most. The main reason I’m confident we are not heading for another 1970s-style Great Inflation is that the Federal Reserve is different. And I’m not referring to the people of the Fed, who clearly have changed, but to the practices and beliefs, which have changed even more.

One major evolution that separates today’s Federal Reserve from the Fed of 50 years ago is a deep understanding that inflation expectations infl

uence future inflation (Orphanides and Williams 2005 and Bernanke 2007b). If people expect inflation to persist, then it does (Gürkaynak, Levin, and Swanson 2010).

This understanding led the Fed, and economists more broadly, to a critical insight: in order to manage actual inflation, policymakers also have to manage inflation psychology, as former Fed Chair Paul Volcker (1979) observed at the time. The Fed has to enlist the help of households, businesses, and market participants in the job of fighting inflation, by communicating with them about its commitment to price stability and its plan to achieve it.

Acting on this insight required a radical transformation. The Fed had to break open its “black box” of decisionmaking and embrace transparency.

To understand the magnitude of this transformation, you have to recall that, for most of its history, the Fed was uncommunicative.

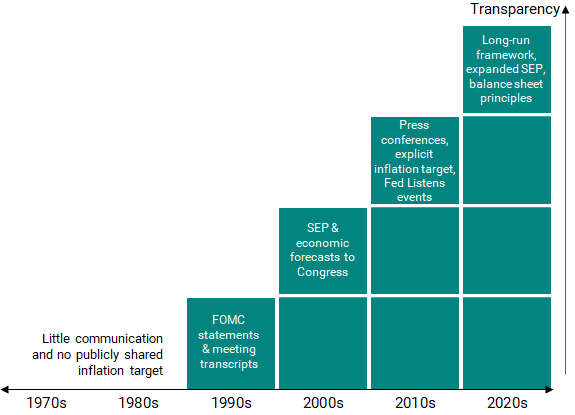

The first step in its communications “revolution,” as Yellen (2012) called it, came in 1994, when the Fed began releasing post-FOMC meeting statements (see Figure 2). In the mid-2000s, the Fed went further, publishing the Summary of Economic Projections to provide the public with information about the expected path of the economy and interest rates. In 2012, the Fed announced its first explicit inflation target, 2%.

Figure 2

Timeline: Federal Reserve’s transparency highlights

Source: Federal Reserve Board of Governors.

And in 2020, we introduced a new monetary policy framework, which outlined principles for managing our inflation and employment mandates in a variety of economic conditions.

As the figure illustrates, the Fed went from being mostly silent to explicitly and intentionally transparent.

The effects of these efforts can be seen in the data (see Figure 1). With greater transparency came more stable inflation expectations, which, since the late 1990s, have remained well anchored around 2% through spikes or drops in the inflation rate (Williams 2006, Bernanke 2007b, and Jørgensen and Lansing 2022).

Even today, with inflation at a 40-year high, long-run inflation expectations of businesses have remained quite stable (see Survey of Professional Forecasters). And financial market expectations have also been well anchored, as evidenced by long-term interest rates staying low despite the current inflation shock.

This tells us that businesses and markets are listening. They’re hearing the Fed’s communications and believe that we will act on our commitments.

In practice, greater transparency, better communication, and the era of well-anchored inflation expectations built Fed credibility. And this credibility provides an important insurance. It makes the economy more resilient and less vulnerable to painful periods like the one we experienced in the 1970s (see Bernanke 2003) And it gives all economic agents, not just the Fed, a role to play in helping the economy smooth through inflation and other shocks, making it more resilient to whatever changes are on the horizon.

Most importantly, greater transparency and a strong commitment to achieving our goals assures Americans that periods of high inflation or unemployment will not last forever; that there is an end in sight.

Focused and aware

But transparency is not a destination, it’s a practice. And it requires ongoing communication if we are to keep the credibility that we so value.

In that spirit, let me tell you about how I see the economy today and the policy adjustments that will be needed to move us to a sustainable path.

Let’s start with the economy. By almost any measure, it is doing well. GDP growth, consumer spending, and business investment are all up, and the labor market continues to post solid job gains, low unemployment, and strong wage growth. Importantly, labor market gains have been broad based, occurring for a wide range of groups, including those who are traditionally disadvantaged—African Americans, Hispanics, and people with less than a college education.

Of course, as everyone knows, inflation is too high, and inflation pressures have begun to spread outside of sectors most directly affected by pandemic-related disruptions (Lansing, Oliveira, and Shapiro 2022). Most strikingly, average Americans, like my parents five decades ago, are worrying about rising prices and rising bills.

This means it is time to move away from the extraordinary support that the Fed has been providing during the pandemic and bring monetary policy in line with the challenges of today. Absent any significant negative surprises, I see our next meeting, in March, as the appropriate time to begin this adjustment.

The timing and magnitude of future funds rate and balance sheet adjustments will depend on how the economy and the data evolve. And this will depend on how well we transition from pandemic to endemic; how much and how quickly supply chains recover; how rapidly workers sidelined by health, family care, or other COVID-related barriers return to the labor force; and how quickly the fiscal boost that aided spending in 2020 and 2021 fades. We will closely watch all of these developments and let the data determine the appropriate path of policy.

As we adjust policy and move into a post-pandemic world, we will also have to keep in mind that many of the challenges that existed pre-pandemic will likely still be with us. Notable for policy are slower global growth, less monetary and fiscal policy space, and the associated downward pressure on inflation (Fernald and Li 2019 and Elsby, Hobijn, and Şahin 2013). These and other developments help explain the steady decline in the neutral policy rate, which over the past 30 years has been more prone to reaching the zero lower bound (see Mertens and Williams 2021).

Against this backdrop, the next few years will require focused awareness; focus on bringing inflation back down to levels consistent with price stability and delivering a labor market that works for everyone; and awareness, of the uncertainty that lies ahead and the challenges that are surely before us.

Different never rests

That for me is the main lesson of the Great Inflation. It’s not really about the Fed. It’s not even really about economics.

It’s about humility.

It’s about knowing that ours is an economy in transition. And that none of us knows for sure what the new future holds.

We need to move forward with confidence—in our policy, in our tools, and in the credibility the Fed has built. But we also have to remember that evolution isn’t static. And to meet the needs of a constantly changing economy, we have to be constantly changing.

Today’s Federal Reserve looks different than it did 50 years ago. And I expect that it will look different again in 50 more.

And that will be a good thing. It will mean the evolution continued. And that next time will also be different.

Mary C. Daly is president and chief executive officer of the Federal Reserve Bank of San Francisco.

References

Basu, Susanto, and John G. Fernald. 2002. “Aggregate Productivity and Aggregate Technology.” European Economic Review 46(6, June), pp. 963–991.

Bernanke, Ben S. 2003. “‘Constrained Discretion’ and Monetary Policy.” Speech to the Money Marketeers of New York University, February 3.

Ber

nanke, Ben S. 2007a. “Federal Reserve Communications.” Speech at the Cato Institute 25th Annual Monetary Conference, Washington, DC, November 14.

Bernanke, Ben S. 2007b. “Inflation Expectations and Inflation Forecasting.” Speech at the Monetary Economics Workshop of the National Bureau of Economic Research Summer Institute, Cambridge, MA, July 10.

Bryan, Michael. 2013. “The Great Inflation.” Federal Reserve History Essay, November 22.

Clarida, Richard, Jordi Galí, and Mark Gertler. 2000. “Monetary Policy Rules and Macroeconomic Stability: Evidence and Some Theory.” Quarterly Journal of Economics 115(1), pp. 147–180.

Cogley, Timothy, and Argia M. Sbordone. 2008. “Trend Inflation, Indexation, and Inflation Persistence in the New Keynesian Phillips Curve.” American Economic Review 98(5, December), pp. 2,101–2,126.

Crump, Richard K., Stefano Eusepi, Marc Giannoni, and Ayşegül Şahin. 2019. “A Unified Approach to Measuring u*.” Brookings Papers on Economic Activity (Spring), pp. 143–238.

Cukierman, Alan, and Allan H. Meltzer. 1986. “A Theory of Ambiguity, Credibility, and Inflation under Discretion and Asymmetric Information.” Econometrica 54(5, September), pp. 1,099–1,128.

DeLong, J. Bradford. 1997. “America’s Peacetime Inflation: The 1970s.” In Reducing Inflation: Motivation and Strategy, eds. Christina Romer and David Romer. Chicago: University of Chicago Press, pp. 247–280.

Eichengreen, Barry. 2015. “Secular Stagnation: The Long View.” American Economic Review 105(5, May), pp. 66–70.

Elsby, Michael W.L., Bart Hobijn, and Ayşegül Şahin. 2013. “The Decline of the U.S. Labor Share.” Brookings Papers on Economic Activity 2013(2), pp. 1–63.

Federal Open Market Committee. 2003. “Minutes of the Federal Open Market Committee Meeting on June 24-25.”

Fernald, John, and Huiyu Li. 2019. “Is Slow Still the New Normal for GDP Growth?” FRBSF Economic Letter 2019-17 (June 24).

Gordon, Robert J. 2015. “Secular Stagnation: A Supply-Side View.” American Economic Review 105(5), pp. 54–59.

Gürkaynak, Refet S., Andrew Levin, and Eric Swanson. 2010. “Does Inflation Targeting Anchor Long-Run Inflation Expectations? Evidence from the U.S., U.K., and Sweden.” Journal of the European Economic Association 8(6), pp. 1,208–1,242.

Jørgensen, Peter Lihn, and Kevin J. Lansing. 2022. “Anchored Inflation Expectations and the Slope of the Phillips Curve.” Federal Reserve Bank of San Francisco Working Paper 2019-27 (revised January 2022).

Lansing, Kevin J. 2000. “Exploring the Causes of the Great Inflation.” FRBSF Economic Letter 2000-21 (July 7).

Lansing, Kevin J. 2009. “Time-Varying U.S. Inflation Dynamics and the New Keynesian Phillips Curve.” Review of Economic Dynamics 12(2), pp. 304–326.

Lansing, Kevin J., Luiz E. Oliveira, and Adam Hale Shapiro. 2022. “Will Rising Rents Push Up Future Inflation?” FRBSF Economic Letter 2022-03 (February 14).

Laubach, Thomas, and John C. Williams. 2016. “Measuring the Natural Rate of Interest Redux.” Business Economics 51, pp. 57–67.

Mertens, Thomas M., and John C. Williams. 2021. “What to Expect from the Lower Bound on Interest Rates: Evidence from Derivatives Prices.” American Economic Review 111(8), pp. 2,473–2,505.

Orphanides, Athanasios. 2003. “The Quest for Prosperity without Inflation.” Journal of Monetary Economics 50(3), pp. 633–663.

Orphanides, Athanasios, and John C. Williams. 2005. “Imperfect Knowledge, Inflation Expectations, and Monetary Policy.” In The Inflation-Targeting Debate, eds. Ben S. Bernanke and Michael Woodford. Chicago: University of Chicago Press, pp. 201–244.

Primiceri, Giorgio E. 2006. “Why Inflation Rose and Fell: Policy-Makers’ Beliefs and U.S. Postwar Stabilization Policy.” Quarterly Journal of Economics 121(3), pp. 867–901.

Ragan, James F., and Bernt Bratsberg. 2000. “Un-Cola: Why Have Cost-of-Living Clauses Disappeared from Union Contracts and Will They Return?” Southern Economic Journal 67(2), pp. 304–324.

Romer, Christina D., and David H. Romer. 2013. “The Most Dangerous Idea in Federal Reserve History: Monetary Policy Doesn’t Matter.” American Economic Review 103(3), pp. 55–60.

Taylor, John B. 1997. “Comment on ‘America’s Peacetime Inflation: The 1970s’ by J. Bradford DeLong.” In Reducing Inflation: Motivation and Strategy, eds. Christina Romer and David Romer. Chicago: University of Chicago Press, pp. 276–280.

Volcker, Paul A. 1979. “Statement before the Joint Economic Committee.” October 17. Accessible on FRASER, Federal Reserve Bank of St. Louis.

Weise, Charles L. 2012. “Political Pressures on Monetary Policy during the U.S. Great Inflation.” American Economic Journal: Macroeconomics 4(2), pp. 33–64.

Williams, John C. 2006. “Inflation Persistence in an Era of Well-Anchored Inflation Expectations.” FRBSF Economic Letter 2006-27, October 13.

Yellen, Janet. 2012. “Revolution and Evolution in Central Bank Communications.” Speech at Haas School of Business, University of California, Berkeley, November 13.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org