Monetary policy surprises—changes in various interest rates around central bank communication events—reflect new information in monetary policy actions and communications. For the Federal Reserve, surprises around Federal Open Market Committee statements and post-meeting press conferences have, in recent years, often led to meaningful market surprises that capture policy news. Event-study analysis provides new market-based evidence of monetary policy transmission: Hawkish policy surprises lower market-based inflation expectations, while dovish surprises raise them, in line with standard monetary transmission. These effects are especially strong at longer horizons.

Central banks use changes in short-term interest rates as their primary monetary policy tool. However, effective transmission of monetary policy to the economy also depends on the ability of central banks to affect financial conditions more broadly, including long-term interest rates and prices in various financial markets. They accomplish this in large part by communicating the likely future path of policy rates and their assessment of risks around this outlook. If this communication is effective, financial markets respond and quickly incorporate the new information.

Two of the most important ways the Federal Reserve communicates with the public are the statements released after each Federal Open Market Committee (FOMC) meeting and the Chair’s post-meeting press conferences. The effectiveness of the Fed’s policy communications can be assessed by studying financial market changes around these events. While the FOMC generally seeks to avoid market volatility, and indeed transparent communication aids monetary policy transmission, some surprises are the inevitable result of news about the policy outlook. These market surprises are useful to researchers to assess the effects of monetary policy.

In this Economic Letter, we study the impact of Fed communication on market-based inflation expectations, which is particularly interesting given the heightened importance of inflation expectations and the abundance of financial data related to inflation. Our analysis is based on Acosta et al. (2025) and relies on empirical monetary policy surprises from our new U.S. Monetary Policy Event-Study Database (USMPD). We use these data to measure monetary policy news in FOMC statements and from post-meeting press conferences. Our evidence of the effects on market-based inflation expectations across horizons provides new insights related to the effectiveness and transmission of the Fed’s monetary policy.

High-frequency monetary policy surprises

A common approach to measuring the news contained in central bank communications uses monetary policy surprises: high-frequency changes in interest rates for short-maturity financial instruments around the time of monetary policy announcements. These measures capture new information about the Fed’s policy path relative to expectations right before the event. They have become popular in economic research because they help identify effects on financial markets, economic expectations, and macroeconomic indicators such as inflation (Bauer and Swanson 2023b).

The SF Fed’s USMPD—which is updated after every FOMC meeting—provides high-frequency changes for a wide range of interest rates and asset prices around FOMC statements, post-meeting press conferences, and releases of FOMC meeting minutes. Acosta et al. (2025) describe the database in detail and document new empirical results on the financial market effects of FOMC communications.

Using the data in the USMPD, we construct our surprise measure from changes in the interest rates of federal funds futures, Eurodollar, and Secured Overnight Financing Rate futures up to four quarters ahead. Essentially, the measure summarizes unexpected changes in the policy rate and expectations over a roughly one-year horizon. The changes are calculated over three different windows for each event: a 30-minute window around the release of the FOMC statement, a 70-minute window around the post-meeting press conference, and a “monetary event” window that covers both the statement and press conference and therefore captures all the policy news released after an FOMC meeting.

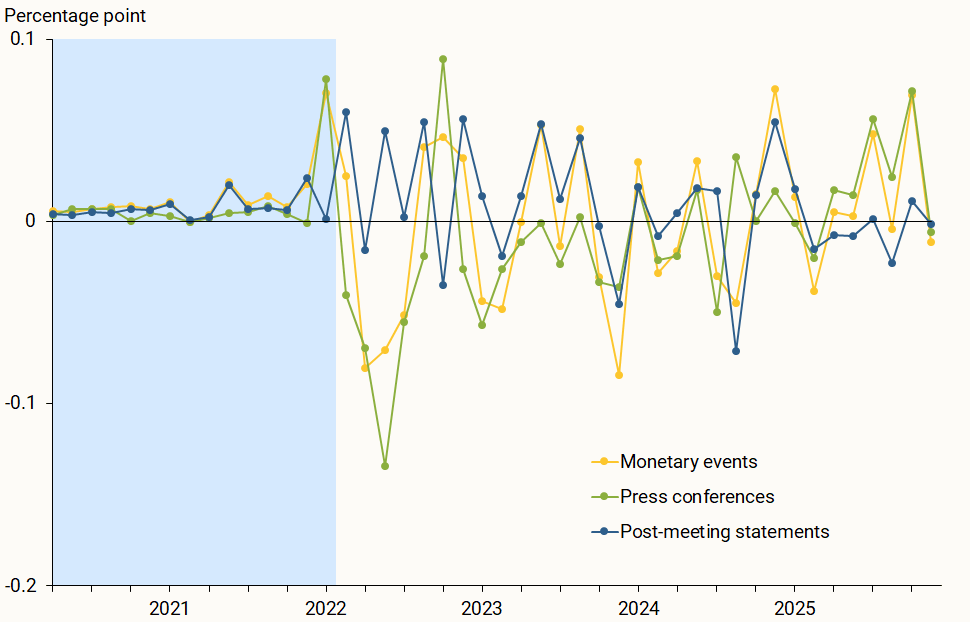

Figure 1

Recent monetary policy surprises

Figure 1 shows the recent evolution of the surprises for FOMC statements, press conferences, and monetary events. Positive values reflect hawkish surprises, when the FOMC’s action led to a surprise increase in the policy rate or in expectations for its future path; similarly, negative values reflect dovish surprises, or surprise decreases in the policy rate or expectations.

Figure 1 depicts several large policy surprises starting in 2022, when the Fed raised its policy rate from the near-zero level that it had maintained since the onset of the COVID-19 pandemic. During the 2022–23 period of policy tightening, the changes sometimes exceeded and sometimes fell short of expectations, leading to both positive (hawkish) and negative (dovish) market surprises. Both FOMC statements and press conferences caused such surprises, in some cases pushing financial markets in opposite directions following a single meeting. Since 2022, press conference surprises were about 40% larger than statement surprises. While empirical studies of FOMC communications have traditionally focused on the market effects of post-meeting statements, Figure 1 demonstrates the importance of accounting for policy surprises from press conferences.

Breakeven inflation rates

To study the effects of monetary policy on market-based inflation expectations, we use daily data for breakeven inflation (BEI) rates from the Federal Reserve Board’s Yield Curve Models and Data website. These BEI rates are calculated as the difference between nominal and real Treasury yields, the latter based on Treasury Inflation-Protected Securities (TIPS). BEI rates, also known as inflation compensation rates, include not only investors’ inflation expectations but also risk and liquidity premiums. Nevertheless, they are commonly used to measure and monitor market-based inflation expectations.

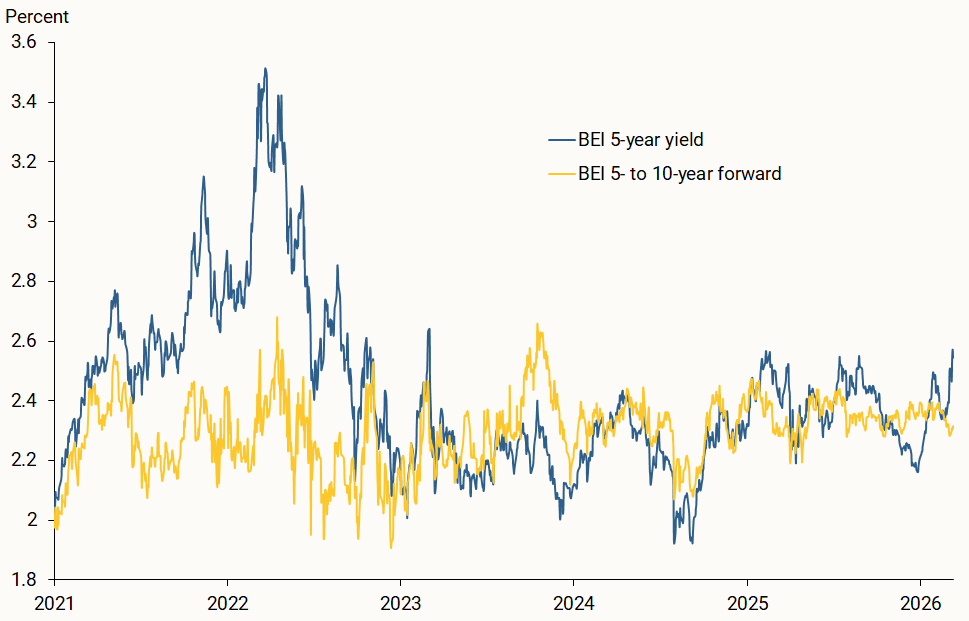

Figure 2

Market-based inflation expectations

Source: Federal Reserve Board.

The recent evolution of BEI rates provides useful context for our empirical analysis. Figure 2 shows two commonly studied BEI rates from 2021 to 2026. The five-year BEI rate (blue line), which represents market-based expectations for inflation over the following five years, rose moderately in early 2025; it then fluctuated between 2.4% and 2.6% during a period of rising concerns about tariff effects and persistently higher inflation. While these expectations declined over the second half of 2025, they have picked up since the beginning of 2026, likely reflecting shifting perceptions about a risk of higher inflation. The five-to-ten-year forward BEI rate (gold line) captures long-run inflation expectations as reflected in bond prices. This rate has generally remained in a range that, considering the usual difference between the CPI and PCE measures of inflation, is broadly consistent with the FOMC’s longer-run inflation target of 2%.

How does the FOMC affect inflation expectations?

To study how monetary policy affects market-based inflation expectations, we estimate market reactions to monetary policy communications using event studies. Specifically, we estimate how much different BEI forward rates—corresponding to inflation expectations for different horizons—change in response to monetary policy surprises. We consider policy surprises around FOMC statements separately from press conference surprises.

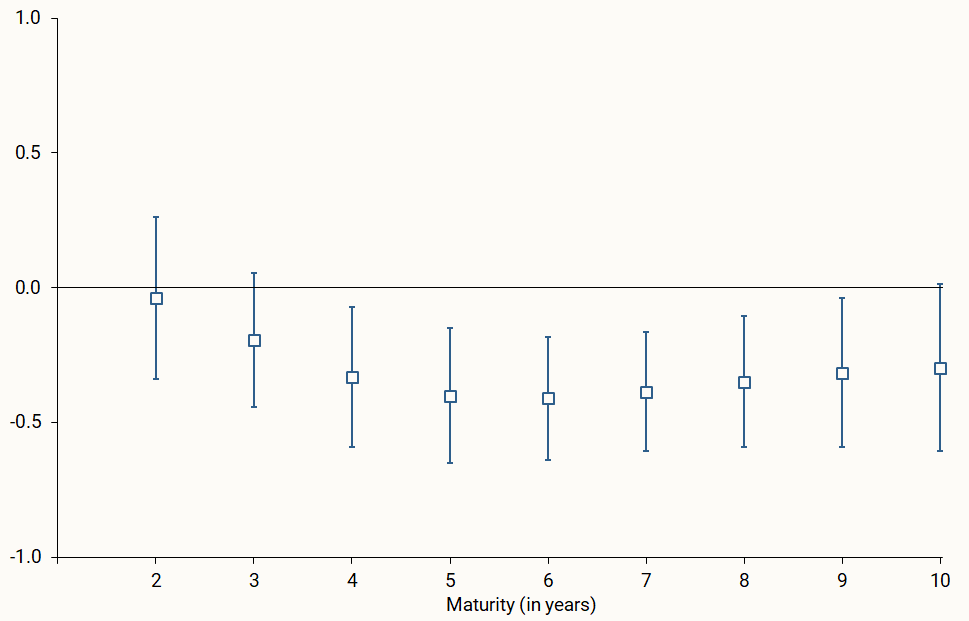

Figure 3

Response of BEI forward rates to statement surprises

For FOMC statement surprises, Figure 3 shows the size of the responses in BEI forward rates from two- to ten-year maturities. Each data point captures the daily response of market-based inflation expectations at a specific horizon. The magnitude of the effects is meaningful, with the largest effect being –0.45, implying that a 10 basis point (0.10 percentage point) hawkish surprise in the expected policy path leads to a roughly 4.5 basis point (0.045 percentage point) decline in market expectations for inflation at those horizons.

The negative estimated relationship means that hawkish monetary policy surprises lower inflation expectations and dovish surprises raise them. This direction is consistent with conventional transmission of monetary policy, according to which tighter (more restrictive) policy tends to reduce future inflation, and vice versa for easier policy. An alternative hypothesis—known as “Fed information effects”—implies that tighter policy could instead raise expectations of future inflation. The rationale is that observers might infer that the Fed has private information pointing to higher inflation underlying their decision—thus, based on this signal, those observers revise their own inflation expectations upward. The extent of such information effects is hotly debated, but our estimates show no evidence in support of this hypothesis, in line with other recent empirical studies (Bauer and Swanson 2023a).

The horizon pattern in Figure 3 shows that market expectations for inflation five to six years in the future have the strongest market reaction to FOMC surprises. Taken at face value, one might interpret this result as suggesting a significant expected delay in the transmission of policy changes to inflation. However, such long delays are inconsistent with the well-established empirical evidence on monetary transmission to inflation (see, for example, Bauer and Swanson 2023b).

An alternative interpretation appears more plausible: Monetary policy surprises contain signals about the broader policy strategy of the FOMC, including how it manages and responds to inflation risks. For example, a hawkish surprise during an episode with above-target inflation may be viewed as a signal that the FOMC will be more aggressive in fighting inflation than previously expected. Changing public perceptions about the policy reaction function would then cause investors and forecasters to lower their inflation expectations over the longer run. This channel—that is, the signals about the policy reaction function that consequently change public perceptions—is consistent with recent research on shifting perceptions about monetary policy (Bauer, Pflueger, and Sunderam 2024).

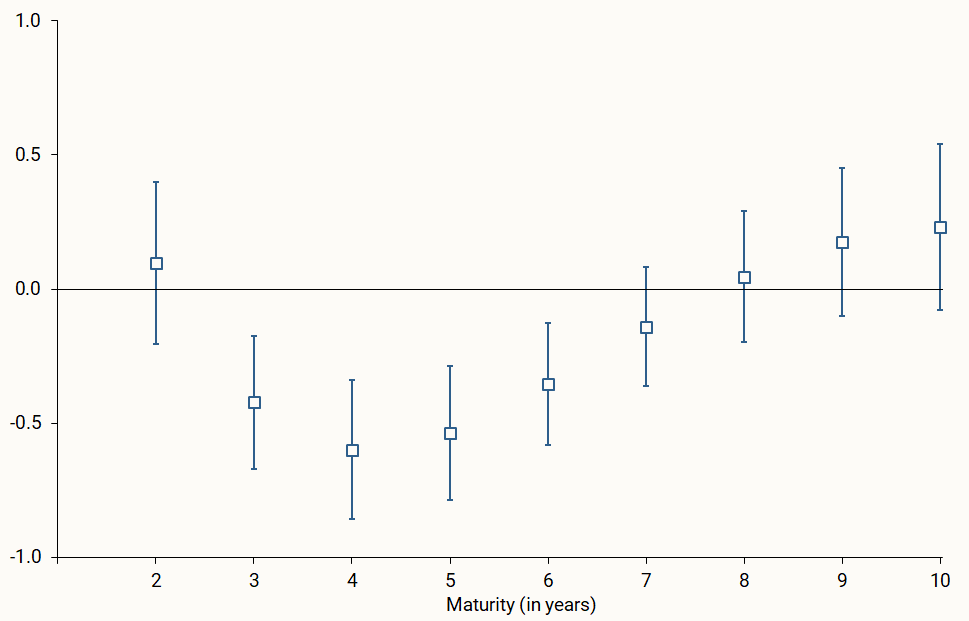

Figure 4

Response of BEI rates to press conference surprises

Figure 4 shows analogous event-study estimates for press conference surprises. The maximum impact is –0.6, implying that a 10 basis point (0.10 percentage point) hawkish press conference surprise leads to a roughly 6 basis point (0.06 percentage point) decline in market expectations for inflation at those horizons, slightly larger than the effects of statement surprises. Additional results in Acosta et al. (2025) show that press conference surprises tend to be stronger at affecting inflation expectations than statement surprises.

The largest response occurs at a slightly shorter horizon than for statement surprises, but this horizon of four years is still substantially longer than typical lags of policy transmission. This evidence confirms that the Chair’s remarks during the press conference can have strong effects on market-based inflation expectations and, more broadly, that the post-meeting remarks by the Fed Chair are another powerful channel for communicating about the Fed’s monetary policy.

Conclusion

This Letter uses data from the USMPD—an extensive new database and tool for researchers—to investigate monetary policy surprises and their transmission to market-based inflation expectations. The analysis shows that FOMC communications such as post-meeting statements and press conferences frequently lead to meaningful unexpected changes for the policy path. Our estimates show that FOMC communications affect market-based inflation expectations. The estimated effects are consistent with standard channels of monetary transmission and signals about the policy reaction function.

The effects are strong both for the information in the FOMC statements and for the news conveyed by the Chair in the post-meeting press conferences. While our analysis does not include the market reaction to speeches of FOMC participants, it is plausible that influential, market-moving speeches might have qualitatively similar effects on inflation expectations.

References

Acosta, Miguel, Andrea Ajello, Michael Bauer, Francesca Loria, and Silvia Miranda-Agrippino. 2025. “Financial Market Effects of FOMC Communication: Evidence from a New Event-Study Database.” Federal Reserve Bank of San Francisco Working Paper 2025-30.

Bauer, Michael, and Eric Swanson. 2023a. “An Alternative Explanation for the ‘Fed Information Effect.’” American Economic Review 113(3).

Bauer, Michael, and Eric Swanson. 2023b. “A Reassessment of Monetary Policy Surprises and High-Frequency Identification.” NBER Macroeconomics Annual 37.

Bauer, Michael, Carolin Pflueger, and Adi Sunderam. 2024. “Perceptions about Monetary Policy.” Quarterly Journal of Economics 139(4).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org