Public institutions like the Federal Reserve must evolve to meet new challenges and allow for new possibilities. At the Fed, we have modernized and innovated over time, always grounding ourselves in our founding principles—to be regional in our work, independent in our thinking, and accountable to those we serve. The following is adapted from remarks by the president of the Federal Reserve Bank of San Francisco to the St. George Area Chamber of Commerce, in St. George, Utah, on April 8.

Good morning and thank you for inviting me to southern Utah. I am delighted to be here and look forward to a lively conversation.

The Federal Reserve has been in the news these days. There are questions about Fed independence, the structure of the Federal Reserve System, and the accountability of Fed policymakers to elected officials and to the American people. But what most people want to know is whether they can trust the Federal Reserve.

Today, I will try to address these issues and describe how the structure of the Federal Reserve, designed by Congress over 100 years ago, had these very concerns in mind. They realized then what we know today: Trust starts with representation and accountability. And that’s a key reason I’m here today.

Origins: Regional, independent, accountable

So, let’s talk about the structure of the Fed. I’ll start with representation. If you have been to Washington, DC, or New York City, you know that the rest of the country looks different. Indeed, the United States is a vast array of people, economies, experiences, and sensibilities.

Congress saw this. Previous attempts to form a U.S. central bank had failed, in large part because they were centered around DC and New York, prioritizing Wall Street over Main Street. As Paul M. Warburg (1930), a key advocate for reforming the nation’s banking system in the early 1900s and a member of the first Federal Reserve Board, wrote: “The view was generally held that centralization of banking would inevitably result in one of two alternatives: either complete governmental control, which meant politics in banking, or control by ‘Wall Street,’ which meant banking in politics.”

The final attempt remedied this. In 1913, the Federal Reserve was created, reflecting national and regional interests and public and private-sector perspectives. The final form of the Federal Reserve Act, as signed by President Woodrow Wilson in 1913, was a product of years of debate and deliberation. (For more information, see the Federal Reserve History project by the Federal Reserve Bank of Kansas City 2013.)

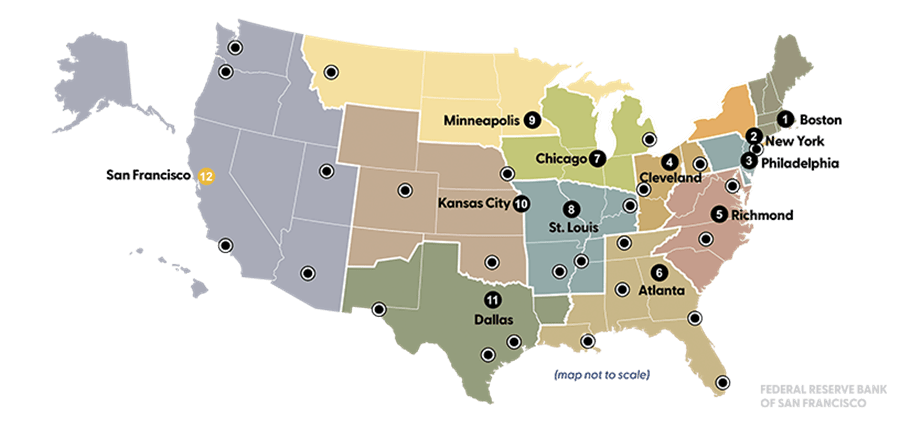

These elements are evident in the Federal Reserve’s structure and footprint (Figure 1; see U.S. Congress 1913 and Ghizoni 2013). There is a Board of Governors in Washington, D.C., and 12 regional Reserve Banks. Together, the 12 regional banks, with their branches and operational locations, represent the United States.

Figure 1

Map of the Federal Reserve Districts

The designers didn’t stop there. They also recognized that, to be effective, the central bank had to be independent. Members of Congress debated over time the degree of influence federal government officials, such as the Secretary of the Treasury and the Comptroller of the Currency, and financial sector executives should have on Federal Reserve decisions (Todd 2012; Goodfriend 2000; Bordo and Prescott 2022; and Richardson and Wilcox 2025).

One way independence shows through is in how monetary policymakers are selected. In Washington, DC, members of the Board of Governors are nominated by the President and confirmed by the Senate. They serve long and staggered 14-year terms to insulate them from undue influence of any given Administration. Reserve Bank presidents are chosen by their Bank’s board of directors (with the concurrence of the Board of Governors), which are made up of leaders of businesses, civic organizations, and banks. This process honors the commitment to regionalism and private-sector governance. (Pursuant to the Dodd-Frank Act, directors representing District member banks may not participate in the appointment of Reserve Bank presidents and first vice presidents; see Board of Governors 2024.)

Finally, to ensure accountability, Congress set the Federal Reserve’s mission and goals. For example, it was through the 1977 Federal Reserve Reform Act that Congress first directed the Federal Reserve to promote the goals of maximum employment, stable prices, and moderate long-term interest rates.

Congress also kept the right to regularly review the Federal Reserve’s performance. The Federal Reserve Act requires the Federal Reserve Board to submit written reports to Congress containing discussions of the conduct of monetary policy, economic developments, and prospects for the future. Since 1979, this report, called the Monetary Policy Report, is submitted semiannually along with testimony from the Federal Reserve Board Chair. The Federal Reserve also publishes other reports and briefs directed to Congress as required by law or in the spirit of transparency.

At the Reserve Banks, a private-sector Board of Directors oversees operations and, along with Reserve Bank leadership, is accountable to the Board of Governors. Reserve Bank directors, by federal law and Federal Reserve policy, must adhere to strict conflict of interest standards in the fulfillment of their duties. Reserve Bank directors may not be involved in, nor be consulted about, the supervision and regulation of financial institutions and may not receive or have access to confidential supervisory information. (See Board of Governors 2017 and Federal Reserve Bank of San Francisco 2024, 2026.)

The current structure and responsibilities of the Federal Reserve have evolved over time through several pieces of legislation, including the 1935 Banking Act, the 1978 Humphrey-Hawkins Act, and the 2010 Dodd-Frank Act (Todd 2012). Although the system has evolved over time, these principles remain: regionalism, independence, and accountability.

The Federal Reserve in practice

That’s how the Federal Reserve was formed, but what does it do? To understand that, we have to go back to 1913 and why Congress created a central bank—to quell financial panics and bank failures and ensure that the U.S. had a common currency, accepted anywhere in the nation (Lowenstein 2015 and Dudley 2016). The solutions are reflected in the Fed’s core responsibilities—managing payments, regulating and supervising banks, and conducting monetary policy.

Let’s start with payments. The Federal Reserve processes around $5 trillion in payments each day and runs the key rails of payment services including cash, checks, automated clearing house transfers, instant payments, and wire transfers (see Federal Reserve Financial Services). Reserve Banks are responsible for most of these operations, ensuring efficiency, effectiveness, and resiliency across the nation.

A little-known fact is that the Federal Reserve manages cash distribution for the nation. It’s a large-scale logistical operation, one where being near your customers matters. Each Federal Reserve District operates cash facilities. You have one here in Utah, at our branch office in Salt Lake City.

Another large component of our work is bank regulation and supervision. The Federal Reserve Board in Washington, DC, and the Vice Chair for Supervision hold primary responsibility for this work. Supervision is a function of the Board, with Reserve Banks conducting supervision under the Board’s delegated authority. (See Board of Governors 2023a for more information.) That said, many of the examination teams sit in regional Reserve Banks, leveraging local knowledge about economic conditions to better serve the banks in their communities. (See Board of Governors (2023b) for more information.)

The rest of our work focuses on monetary policy. And here, a diversity of views supports better outcomes. In practice, this means each Reserve Bank has its own research team. The FOMC is made up of nineteen participants—the seven Board of Governors members and twelve Federal Reserve Bank presidents. The Committee meets eight times per year, during which Fed presidents have the opportunity to share insights and findings from their respective research teams that help inform and support monetary policy decisions.

This helps guard against groupthink and ensures that the system is debating and challenging institutional norms and perspectives. As Marvin Goodfriend (2000) noted, “one of the great strengths of policy made by representatives from a system of regional central banks is the diversity and number of points of view brought to the table…. A system of central banks promotes a healthy competition that stimulates innovative thinking on operational, regulatory, research, and policy questions.”

Reserve Banks also provide centers of expertise that serve the entire system, for example, financial markets at the New York Fed, energy studies at the Dallas Fed, and emerging technologies at the San Francisco Fed, just to name a few.

Reserve Banks also rely on regional engagement teams, who meet regularly with local businesses, bankers, and community groups to gather real-time information about the economy. The information used for monetary policy deliberations comes from multiple sources, including quantitative data and economic analyses, as well as qualitative information from ongoing engagement with our Regional Community and Economic Perspectives network. Conversations with our communities help us understand the different economic experiences of the people we serve, from households and consumers, small business owners, and large employers that drive local economic growth.

This has been one of the priorities of my presidency, putting people in the field to learn from the people we serve. Whether we are hosting roundtables, conducting surveys, or doing events like the one today, we are learning how the economy works in practice, not just in theory. Insights from our engagements are shared through our SF Fed blog post series and the Twelfth District Beige Book reports.

So, that’s the Federal Reserve. Our work reflects our founding principles. And it has stood the test of time.

The responsibility to evolve

So, what does our future hold? As a longtime public servant, I know that public institutions are pillars of democracy. But to remain strong, they must evolve—ready to meet new challenges and allow for new possibilities.

The Federal Reserve is no exception.

In my 30 years at the Fed, I have seen—and led—a lot of change, including efforts to modernize and innovate our practices, processes, and operations. In each of these efforts, the motivations were the same: to be more efficient, more effective, and more resilient.

But we are never done. The world is always changing, and the Federal Reserve must change with it, always grounded in our principles—the ones that Congress established: to be regional in our work, independent in our thinking, and accountable to those we serve. Thank you. I look forward to our discussion.

References

Board of Governors of the Federal Reserve System. 2017. “Policies Governing Directors: Access to Confidential Supervisory Information.” Last update February 9, 2017; accessed April 6, 2026.

Board of Governors of the Federal Reserve System. 2023a. “Understanding Federal Reserve Supervision: About Bank Supervision.” Last update April 27, 2023; accessed April 6, 2026.

Board of Governors of the Federal Reserve System. 2023b. “Understanding Federal Reserve Supervision: Approaches to Bank Supervision.” Last update April 27, 2023; accessed April 6, 2026.

Board of Governors of the Federal Reserve System. 2024. “Overview: Federal Reserve System Boards of Directors.” Last update January 5, 2024; accessed April 6, 2026.

Bordo, Michael D., and Edward S. Prescott. 2022. “Federal Reserve Structure and Economic Ideas.” Federal Reserve Bank of Cleveland Working Paper 22-08.

Dudley, William C. 2016. “The Role of the Federal Reserve—Lessons from Financial Crises.” Remarks at the Annual Meeting of the Virginia Association of Economists, Virginia Military Institute, Lexington, VA, March 31.

Federal Reserve Bank of Kansas City. 2013. “Federal Reserve Act Signed into Law.” Federal Reserve History, accessed April 6, 2026.

Federal Reserve Bank of San Francisco. 2024. “Bylaws of the Federal Reserve Bank of San Francisco.” As amended February 2024, effective March 7, 2024.

Federal Reserve Bank of San Francisco. 2026. “Boards of Directors.” Accessed April 6, 2026.

Ghizoni, Sandra Kollen. 2013. “Reserve Bank Organization Committee.” Federal Reserve History, accessed April 6, 2026.

Goodfriend, Marvin. 2000. “The Role of a Regional Bank in a System of Central Banks.” Federal Reserve Bank of Richmond Economic Quarterly 86(1, Winter).

Lowenstein, Roger. 2015. America’s Bank: The Epic Struggle to Create the Federal Reserve. New York: Penguin Press.

Richardson, Gary, and David W. Wilcox. 2025. “How Congress Designed the Federal Reserve to Be Independent of Presidential Control.” Journal of Economic Perspectives 39(3), pp. 221–238.

Todd, Tim. 2012. The Balance of Power: The Political Fight for an Independent Central Bank, 1790-Present. Kansas City: Federal Reserve Bank of Kansas City.

U.S. Congress. 1913. “Federal Reserve Act.” Available via FRASER, St. Louis Fed, accessed April 6, 2026.

Warburg, Paul M. 1930. The Federal Reserve System: Its Origins and Growth. New York: The Macmillan Company.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org