Labor productivity gains over the past three years helped the U.S. economy expand steadily, even with near-zero employment growth. Combined with substantially increased business investment in artificial intelligence technology, these conditions have raised the question of whether the economy is entering a high-productivity growth period. Two well-known productivity measures do not yet provide strong evidence of this shift. However, recent patterns resemble the mixed signals during the early stages of the 1990s productivity surge before a sustained high-growth period materialized, giving reason for cautious optimism about future productivity growth.

The U.S. economy expanded at a relatively steady pace of around 2.5% per year over the past three years, even though employment growth slowed to near zero. This combination suggests that productivity improvements may be playing an increasingly important role in output growth.

Over the same time, substantial business investment in artificial intelligence (AI) technology and associated infrastructure has led many to speculate that the economy may be entering a new era of elevated productivity growth, similar to the 1990s. However, incoming data has been mixed so far. For example, labor productivity—which measures output per hour of work—has shown solid gains in recent years. Meanwhile, another popular measure of productivity that adjusts for how much equipment, technology, and other resources workers have at their disposal—the San Francisco Fed’s Total Factor Productivity (TFP) index—has shown relatively modest growth over the same period.

Understanding whether productivity has entered an era of higher growth is important for policymakers and economists. However, determining whether a prolonged period of high growth has begun or not is difficult in real-time and is usually only obvious with the benefit of some hindsight. In the 1990s, it was only recognized after the productivity surge was well under way (Daly 2026). Incoming data often send mixed signals regarding the potential strength of future growth.

In this Economic Letter, we explore the divergence between these two measures and examine the latest evidence regarding whether the U.S. economy has entered a high-productivity growth regime. We use a regime-switching model (Foerster and Matthes 2022) to compare current patterns to the experience of the 1990s technology boom, when a similar divergence between labor productivity and TFP emerged before the full productivity benefits became more definitive. Our analysis provides a framework for interpreting recent productivity data and offers cautious optimism about future growth prospects.

Different productivity measures

Labor productivity and TFP are widely used measures of productivity but are different concepts. Labor productivity measures how efficiently workers use the capital available to them, such as equipment or software. As a result, business investment that increases the amount of capital used by workers can raise labor productivity. This situation is referred to as capital deepening.

TFP uses a broader view, measuring how efficiently the economy uses all inputs together, including both labor and capital. It is meant to capture genuine improvements to processes and technology and is therefore considered a key factor underlying the long-run growth of the economy.

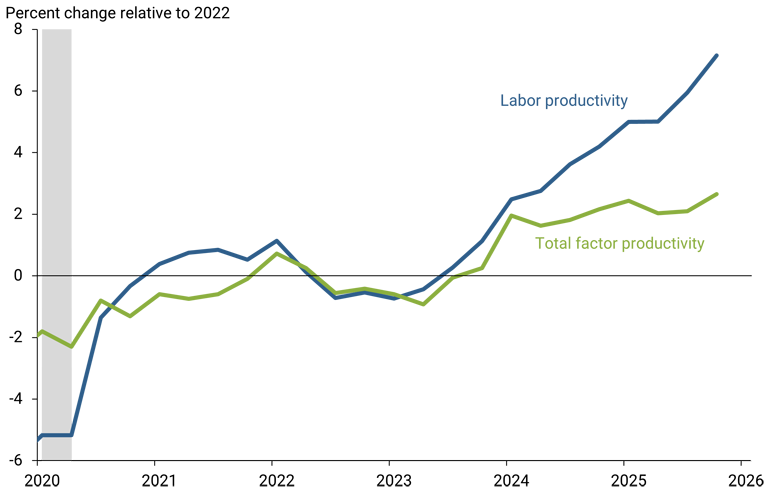

Figure 1 plots how labor productivity and TFP have evolved relative to 2022 values, right before the recent surge in labor productivity. While the measures moved in tandem during most of the period immediately following the pandemic, their paths have since diverged, with labor productivity growing at a faster pace in recent years. This divergence comes amid a surge in business investment in AI technology and infrastructure, such as data centers. The increased investment has coincided with more productive workers but has not yet produced the broader gains that TFP is designed to measure. This suggests that productivity improvements so far reflect better tools for workers rather than fundamental economic advancement.

Figure 1

Changes in measures of productivity relative to 2022

Periods of high and low productivity growth

The U.S. economy moves through sustained periods of higher or lower average productivity growth, known as productivity regimes. While productivity can vary from quarter to quarter, these regimes capture the idea that there will be some extended periods when technology undergoes relatively rapid advancements, and others when productivity advances more slowly. The U.S. economy has experienced several distinct productivity regimes over the past 70 years, including a high-growth period in the late 1990s, with the proliferation of computers and the internet, and a lengthy period of low average growth during the 2010s.

To identify these productivity regimes, we update the statistical model described in Foerster and Matthes (2022) and Foerster, Matthes, and Seitelman (2020). This regime-switching model analyzes historical productivity data to detect periods of consistently higher or lower growth. The model recognizes that, while productivity growth can fluctuate from quarter to quarter due to temporary factors, the underlying trend tends to remain relatively stable for extended periods before shifting to a new level. By examining patterns in the data, the model calculates the probability that the economy is currently in a high-growth regime versus a low-growth regime. These probabilities are not definitive predictions, but rather statistical assessments based on recent productivity trends and historical patterns.

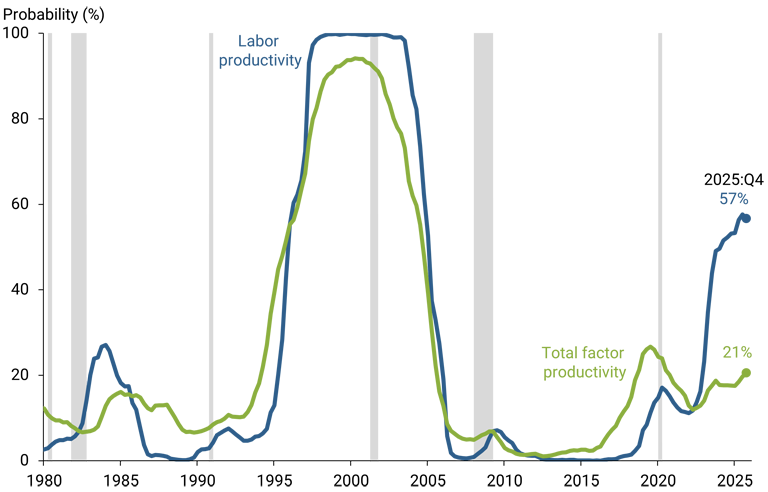

Figure 2 shows the model-implied probability of the U.S. economy being in a high-productivity growth regime using labor productivity (blue line) and TFP (green line). The two measures have largely moved in tandem for much of the past 50 years, with both indicating that the economy was in a high-productivity growth regime in the mid-1990s and early 2000s. More recently, the probabilities based on these two measures have picked up to varying degrees: around 57% based on labor productivity and 21% based on TFP as of the fourth quarter of 2025.

Figure 2

Two measures of high-growth regime probability

Despite the recent increases in these two measures, neither sends a strong enough signal to indicate that the economy has definitively entered a high-productivity growth regime. Perhaps more pessimistically, TFP, which can be seen as the more fundamental driver of economic growth, shows a relatively low probability that we are experiencing a sustained productivity surge.

Is there a reason for cautious optimism?

Despite the mixed signals from current productivity data, the recent increase in probabilities provides some reason for cautious optimism that the U.S. economy may be entering an extended period of higher productivity growth. The strong pace of investment in AI technology and infrastructure may indicate that businesses expect a productivity boom (Kalyani and Li 2026). They are investing heavily now with an eye on the near future, which might help explain why labor productivity is currently sending a stronger signal than TFP.

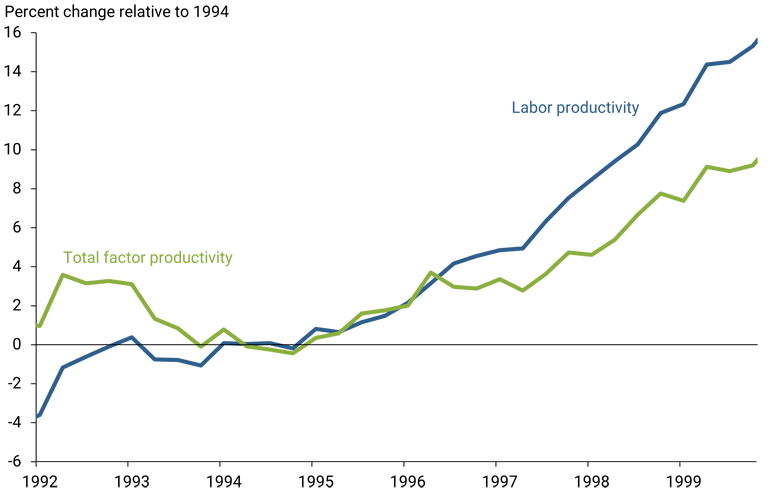

The computer and internet boom of the 1990s can serve as a useful historical parallel for understanding what might lie ahead. Figure 3 shows the changes in labor productivity and TFP relative to 1994 levels. The revised data tell a clearer story about productivity than the data that were available at the time (Daly 2026); for this reason, uncertainty about productivity was even higher at that time than it looks in retrospect. Both measures moved closely together at first, similar to the trend shown in Figure 1. Starting around mid-1996, labor productivity began accelerating more rapidly than TFP, similar to the diverging pattern we observe today. This divergence suggests the current moment may resemble the early stages of the 1990s technology boom, when the full productivity benefits had not yet materialized in overall data but were reflected in business investment decisions.

Figure 3

Changes in productivity measures relative to 1994

But what about regime probabilities? Although Figure 2 shows that the probability of being in a high-productivity growth regime based on the two measures moved in tandem during the 1990s productivity surge, some of this alignment is due to the benefit of hindsight.

For any given quarter, the model-based probabilities shown in Figure 2 use information from the entire sample period, which goes through 2025. In other words, when the model assesses whether the economy was in a high-productivity regime in 1995, it already considers that the economy indeed experienced a surge in productivity in the late 1990s and early 2000s. This makes the computer and internet boom more obvious in retrospect than it actually was at the time.

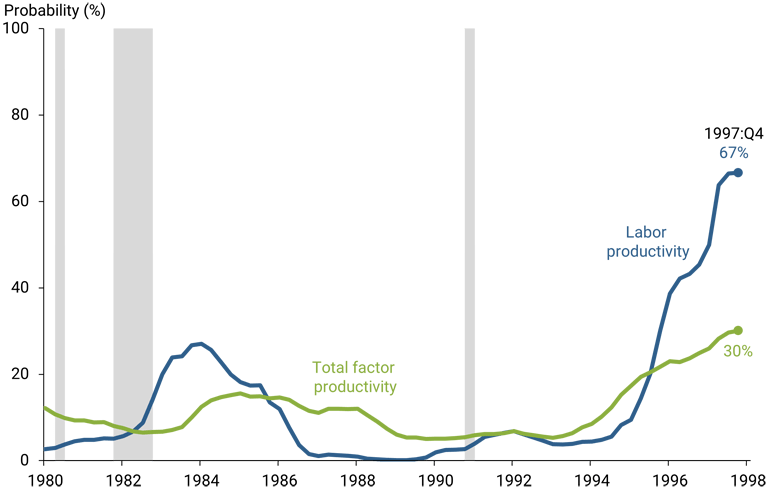

To see how the probabilities would have appeared if we had run the model in the 1990s, Figure 4 removes the benefit of hindsight and restricts the data used for determining the regime probability to end in 1997. With this restriction, the picture is notably less clear. In 1996 and 1997, both measures showed rising probabilities, with labor productivity sending a more optimistic signal than TFP. There was no certainty that the economy had already entered a period of sustained high productivity growth. This result is compounded by the fact that our estimates use currently available data that have been revised; thus, our estimates understate the uncertainty at the time, which were based on unrevised, preliminary data estimates.

Figure 4

High-growth regime probabilities: Data through 1997

The dynamic then was similar to what we have seen in recent years. If today mirrors what we experienced in the mid-1990s, we may be in the early stages of a productivity boom driven by AI that will only become clear in retrospect.

Takeaways

Our analysis in this Letter indicates that the current data on productivity do not yet provide definitive evidence that the U.S. economy has entered a period of high productivity growth. The divergence between strong labor productivity growth and more modest TFP growth suggests that recent investments related to AI might be making workers more productive by providing them with better tools, such as new software and expanded computing capacity, but broader efficiency gains remain unrealized so far.

Nonetheless, our regime-switching statistical model is responding to incoming data similarly to how it would have in the mid-1990s. This provides some reason for cautious optimism that the U.S. economy could be starting to experience a period of sustained high productivity growth. As more data become available, it will be important to continue to monitor whether current patterns represent the early stages of a new era of booming productivity or merely a temporary uptick in an otherwise slow-growth environment.

References

Daly, Mary. 2026. “The AI Moment? Possibilities, Productivity, and Policy.” FRBSF Economic Letter 2026-06 (February 23).

Fernald, John. 2014. “A Quarterly, Utilization-Adjusted Series on Total Factor Productivity.” FRB San Francisco Working Paper 2012-19.

Foerster, Andrew, and Christian Matthes. 2022. “Learning about Regime Change.” International Economic Review 63(4), pp. 1,829–1,859.

Foerster, Andrew, Christian Matthes, and Lily Seitelman. 2020. “The Highs and Lows of Productivity Growth.” FRBSF Economic Letter 2020-21 (August 3).

Kalyani, Aakash, and Huiyu Li. 2026. “Is Optimism for Artificial Intelligence Boosting Investment?” FRBSF Economic Letter 2026-13 (May 18).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org