Central banks purchase bonds and other securities with their own reserves. In doing so, they expand the supply of safe assets in the economy, which should lower the premium investors are willing to pay for safety. Analysis confirms that bond purchases by the European Central Bank in 2015–2021 lowered safety premiums for investors, partially offsetting declines in bond yields as much as 30 basis points. The results suggest that such transactions essentially reduce a central bank’s effectiveness in using asset purchases to lower interest rates in safe bond markets.

When central banks purchase government bonds, they affect the cost for other investors seeking safe assets. The safety premium for buying such bonds reflects the amount investors are willing to pay in return for high-quality assets that can be sold at any time. These premiums rise when safe assets are scarce and fall when they are plentiful.

Central banks generally use bond purchases to reduce yields. However, paying for bonds using their own reserves, which are the safest and most liquid assets, has the potential to raise the amount of safe assets in the economy. The greater supply could make investors less willing to pay a relatively high price for bonds, putting downward pressure on the safety premium of safe assets. This thereby lowers their prices, or equivalently translates into higher yields, and hence provides an offset to the yield declines for very highly rated bonds.

In this Economic Letter, we examine how central banks affect safety premiums when they buy bonds and other safe assets. We describe our recent research in Christensen, Mirkov, and Zhang (2025) that focuses on bond purchases made by the European Central Bank (ECB) from 2015 to 2021. During that period, the ECB bought government bonds equivalent to roughly 30% of euro-area nominal GDP. The purchases included a significant portion of risky high-yield government bonds issued by euro-area peripheral countries. Because the ECB used reserves to pay for those bonds, this most likely increased the supply of safe assets in the euro area, which should have lowered safety premiums for investors both within and outside the euro area. Our results show that safety premiums in bond markets fell in response to the ECB asset purchases. To some extent, this lower cost partially offset the reduction in safe bond yields created by the ECB bond purchases.

The role of safety premiums

A safe asset is a financial instrument that retains its principal value throughout its life, even in times of crisis. As a result, investors are usually willing to pay a premium, known as a safety premium, to purchase the asset in return for its prime credit quality and the convenience of being able to sell it at any time (Christensen and Mirkov 2021).

Safety premiums rise and fall depending on the supply of safe assets. For example, before the COVID-19 pandemic, a global shortfall of safe assets led investors to bid up their prices, which drove down their yields and raised their safety premiums (Caballero et al. 2017). More recently, large public debt issuance in many countries has increased the supply of safe assets, which should lower safety premiums and result in lower prices and higher yields of safe bonds.

To examine the effects in global markets, our study measures safety premiums for highly safe bonds from four AAA-rated countries: Denmark, Germany, Sweden, and Switzerland. These bonds are nearly as safe as reserves, although they are subject to some modest resale risk. Furthermore, their prices may be sensitive to an increased supply of safe assets.

ECB bond purchases

The ECB bond purchases starting in 2015 aimed at stimulating the euro-area economy and combating deflationary pressures. At its peak in 2022, the Eurosystem held assets equivalent to about 37% of euro-area nominal GDP, with supranational and government bonds representing an amount equal to 32% of euro-area nominal GDP.

The ECB operated several bond purchase programs from 2015 to 2021. Its largest program, known as the Public Sector Purchase Programme, purchased government bonds across member states in proportion to each country’s share of the ECB’s total capital. As a consequence, these purchases included both safe low-yielding government bonds from core euro-area countries, such as Germany and France, as well as riskier high-yield government bonds from euro-area peripheral countries, such as Italy and Spain. Bonds from the periphery carried credit risk, meaning the risk of not receiving the promised payments, and redenomination risk, which is the risk of a country abandoning the euro and revaluing its debt in a new and depreciated national currency. These bonds therefore traded at notably larger spreads relative to German government bonds. In response to the COVID-19 pandemic, additional government bonds were acquired under the Pandemic Emergency Purchase Programme. Crucial for our analysis, all purchases were paid for by crediting banks with safe and liquid central bank reserves.

Measuring bond safety premiums

To analyze how the added supply of safe assets affected the euro area, we estimate the safety premiums embedded in government bond prices from Denmark, Germany, Sweden, and Switzerland. We use a standard yield curve model, augmented with a bond-specific risk factor as described in Andreasen, Christensen, and Riddell (2021). We focus on these four countries because they are highly rated sovereigns with plentiful bond-level prices suitable for estimating safety premiums. Moreover, they span a spectrum of integration with the euro area, namely a core member (Germany), a euro-pegged nonmember (Denmark), and two closely linked neighboring countries with independent floating exchange rates (Sweden and Switzerland). This allows us to study both domestic and cross-border safety premium effects of the ECB bond purchases.

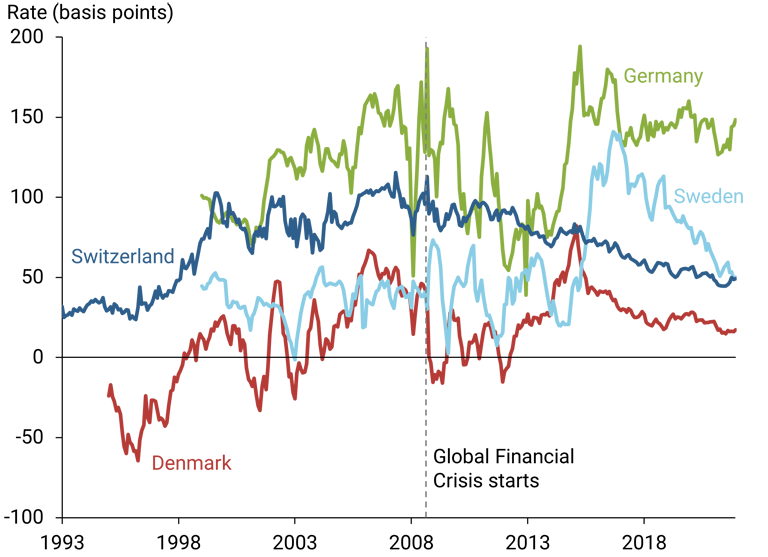

Figure 1 shows the estimated safety premiums for each of the four government bond markets. Positive values indicate that the yield of a bond from that country is lower than it would be without a safety premium. Germany has the highest safety premium among the four countries with an average of 124 basis points (hundredths of a percentage point), followed by Switzerland at 70 basis points and Sweden at 54. Denmark has the lowest average safety premium of 16 basis points. These magnitudes seem reasonable given that Germany has the safest and most liquid government bond market in the euro area, while Switzerland has a long history of being considered a safe haven in times of crisis. For reference, Krishnamurthy and Vissing-Jorgensen (2012) estimate that safety premiums of U.S. Treasury securities range from 27 to 73 basis points.

Figure 1

Estimated government bond safety premiums

During the Global Financial Crisis, Danish safety premiums fell, while those in Germany, Sweden, and Switzerland rose. A likely reason is that investors considered Denmark’s euro peg as a weaker safe haven at that time. By contrast, the onset of COVID-19 in spring 2020 had little effect on safety premiums across all four markets.

Effects of ECB bond purchases on safety premiums

We test whether changes in the supply of safe assets in Europe, driven by the ECB’s bond purchases, are linked to our estimated safety premiums. We quantify this link using a statistical model to explore the variation across countries and across time. In the model, we relate the safety premiums of government bonds from Denmark, Germany, Sweden, and Switzerland to ECB bond purchases measured as a fraction of euro-area nominal GDP.

It is important to acknowledge that a variety of factors could affect safety premiums, including investors’ risk sentiment and fluctuations in general financial market uncertainty. To account for such effects, we incorporate a large number of additional variables into the model. This allows us to conclude with confidence that our results are unlikely to be driven by other factors.

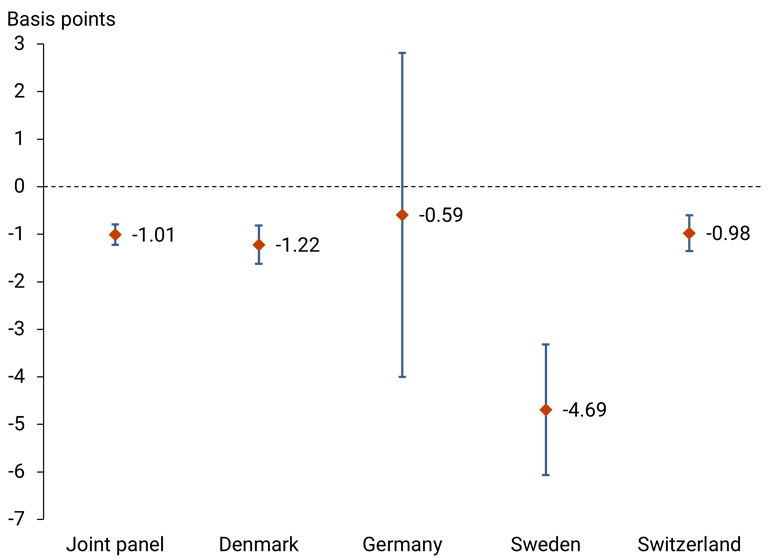

Figure 2 shows the estimated effects of the ECB’s bond holdings on safety premiums across bond markets, with 95% confidence bands showing the accuracy within the range of estimates. The results shown in the first data point indicate that an increase in the ECB bond purchases equal to 1 percentage point of nominal GDP in the euro area is associated with an average decline in the safety premium across the four countries of about 1 basis point (0.01 percentage point). We further analyze the data using separate country-specific statistical models, also shown in Figure 2. There are some notable differences in the estimated effects across countries, but the estimates are reliably negative.

Figure 2

Estimated effects on country-level safety premiums

To interpret the quantitative importance of these estimates, we note that the ECB’s net bond purchases for 2015–2021 totaled about 30% of nominal GDP in the euro area. Based on this, our estimates imply that the total effect lowered safety premiums, and thereby raised government bond yields, as much as 30 basis points. Since the average safety premium on government bonds from these four countries in the sample period is 66 basis points, the cumulative net effect amounts to almost half of this average level, which is an economically significant impact.

Overall, our evidence points to significant negative effects of increases in the ECB’s bond holdings on bond safety premiums. Because this measure represents a proxy for the amount of risky high-yield assets that was replaced by safe central bank reserves, the results suggest that the higher supply of safe assets materially lowered the safety premium on bonds of core European countries, partially offsetting the decline in yields.

Given the global integration of financial markets, our findings have broader implications and can provide a more complete understanding of the effects of central bank bond purchases on the prices of safe assets across countries. On a final note, we reiterate that this effect represents a partial offset to the general decline in European interest rates flowing from the ECB’s bond purchases (see Altavilla et al. 2021).

Conclusion

In this Letter, we describe how large-scale central bank bond purchases can alter the supply of safe assets available in international bond markets and thereby affect the prices of safe assets. Specifically, when a central bank buys risky high-yield assets in exchange for truly safe assets in the form of central bank reserves, the outstanding amount of safe assets increases. This should reduce the additional price premiums that highly safe assets can command in financial markets. Our analysis of bond safety premiums from four highly rated countries confirms this conjecture in the context of the ECB’s 2015–2021 bond purchases.

These findings point to an important international spillover of central bank bond purchases: The impact on the relative scarcity of safe assets partially offsets the decline in yields for other safe government bond markets. This mechanism can, to some extent, lessen the effectiveness of central bank asset purchases in lowering the very safest government bond yields.

References

Altavilla, Carlo, Giacomo Carboni, and Roberto Motto. 2021. “Asset Purchase Programs and Financial Markets: Lessons from the Euro Area.” International Journal of Central Banking 17(4), pp. 1–48.

Andreasen, Martin M., Jens H.E. Christensen, and Simon Riddell. 2021. “The TIPS Liquidity Premium.” Review of Finance 25(6), pp. 1,639–1,675.

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas. 2017. “The Safe Assets Shortage Conundrum.” Journal of Economic Perspectives 31(3), pp. 29–46.

Christensen, Jens H.E., and Nikola Mirkov. 2021. “Exploring the Safety Premium of Safe Assets.” FRBSF Economic Letter 2021-13 (May 10).

Christensen, Jens H.E., Nikola Mirkov, and Xin Zhang. 2025. “Quantitative Easing and the Supply of Safe Assets: Evidence from International Bond Safety Premia.” Journal of International Economics 157(104146).

Krishnamurthy, Arvind, and Annette Vissing-Jorgensen. 2012. “The Aggregate Demand for Treasury Debt.” Journal of Political Economy 120(2), pp. 233–267.

Data

Download data for figures (Excel file, 205 KB)

Visiting researcher, Belgrade Banking Academy, Serbia

Research Advisor, Research Division, Sveriges Riksbank, Sweden

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org