Inflation expectations among businesses can affect how they set current prices. Firms’ expectations diverged from those of professional forecasters during the pandemic-era inflation surge and moved closer to household expectations. Analyzing firms’ survey data from 2018 to 2025 reveals three main patterns behind this shift: Businesses became more sensitive to current inflation perceptions, their longer-term expectations temporarily drifted up, and their perceptions of the Federal Reserve’s inflation goal increased. However, when inflation eventually moderated, the survey data show that firms’ inflation expectations largely returned to their characteristics from before the pandemic.

Expectations about future inflation affect people’s economic decisions today. For example, if they expect higher inflation, households may change their spending and businesses may preemptively raise prices, which could make inflation more persistent. Monetary policymakers routinely monitor inflation expectations of professional forecasters and households to assess if they are consistent with the Federal Reserve’s 2% goal. However, due to a lack of survey data, business expectations are less frequently considered, despite their direct role in shaping many macroeconomic outcomes, such as prices, wages, and investment.

In this Economic Letter, we examine quarterly data from the Federal Reserve Bank of Cleveland’s Survey of Firms’ Inflation Expectations (SoFIE), a large representative panel of U.S. manufacturing and service-sector businesses.

We use survey data between 2018 and 2025 to document how firms’ inflation expectations evolved during and after the pandemic-era inflation surge. Our analysis suggests that, while firms’ expectations temporarily drifted up during the large inflation shock, the subsequent decline in inflation and the Federal Reserve’s monetary policy response may have helped to lower their inflation expectations and thereby restore their pre-pandemic characteristics.

Firms’ inflation expectations differ from those of professional forecasters

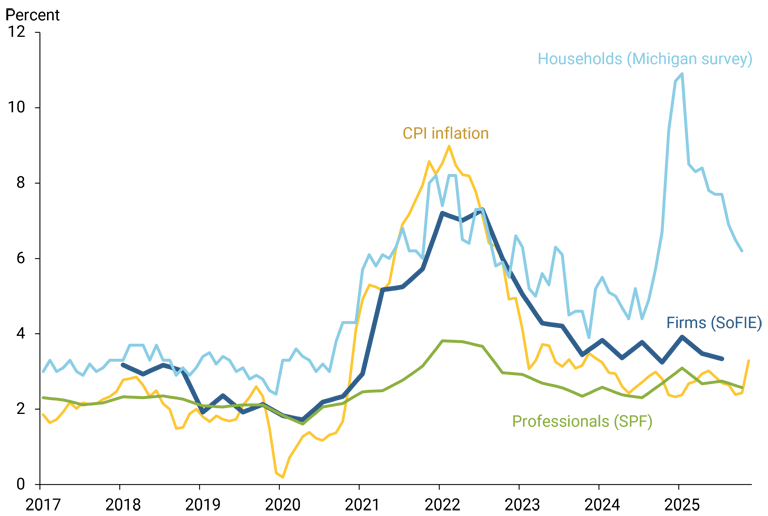

To analyze business inflation expectations, we focus on SoFIE’s quarterly responses by chief executive officers from a large group of U.S. manufacturers and service-sector businesses (see Candia, Coibion, and Gorodnichenko 2023 and Garciga et al. 2023 for survey details). Figure 1 compares the evolution of firms’ one-year-ahead inflation expectations from SoFIE to expectations captured by the University of Michigan Surveys of Consumers (also known as Michigan survey), which focuses on U.S. households, and the Philadelphia Fed’s Survey of Professional Forecasters (SPF), which focuses on professionals in finance and other related areas. The figure also reports realized consumer price index (CPI) inflation from the Bureau of Labor Statistics.

Figure 1

Average inflation expectations across surveys

Between 2019 and early 2020, firms’ one-year-ahead inflation expectations closely tracked professional forecasters’ expectations. Starting in early 2021, as inflation rose above 2%, business expectations abruptly disconnected from professional forecasters’ expectations and increased sharply to nearly 7% by 2022, similar to household expectations during the same period.

By mid-2022, after CPI inflation peaked, firms’ expectations started to decline. Relative to household expectations, business expectations fell faster, closely following the path of realized inflation and moving back toward the levels of professional forecasters. Through the end of 2025, household expectations remained elevated and even rose further amid tariff-related uncertainty, while firms’ expectations continued to decline.

The behavior of firms’ inflation expectations during the pandemic-era inflation surge indicates that they can deviate substantially from professionals’ expectations and move closer to those of households, especially when inflation rises sharply.

Firms’ inflation expectations became more sensitive to current inflation

The stark difference between firms’ and professional forecasters’ short-term inflation expectations during the pandemic-era inflation surge raises some questions about what was influencing firms’ views at the time. To better understand the dynamics in firms’ inflation expectations during this period, we explore the variation across firms by splitting the sample into two groups, small businesses and medium to large firms.

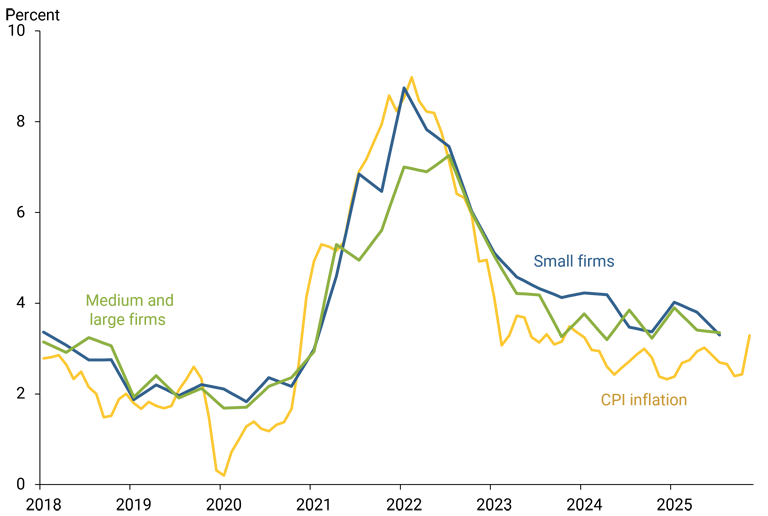

Figure 2 shows inflation expectations by firm size. During the pandemic-era inflation surge, inflation expectations of small firms with 1 to 19 employees increased faster and more strongly than expectations of larger firms with 20 or more employees. The difference in inflation expectations between the two groups reached roughly 2 percentage points at the peak of the inflation surge in 2022. Thereby, small firms’ inflation expectations behaved more similarly to household expectations, while medium to large firms’ expectations remained somewhat closer to those of professional forecasters.

Figure 2

Average inflation expectations by firm size

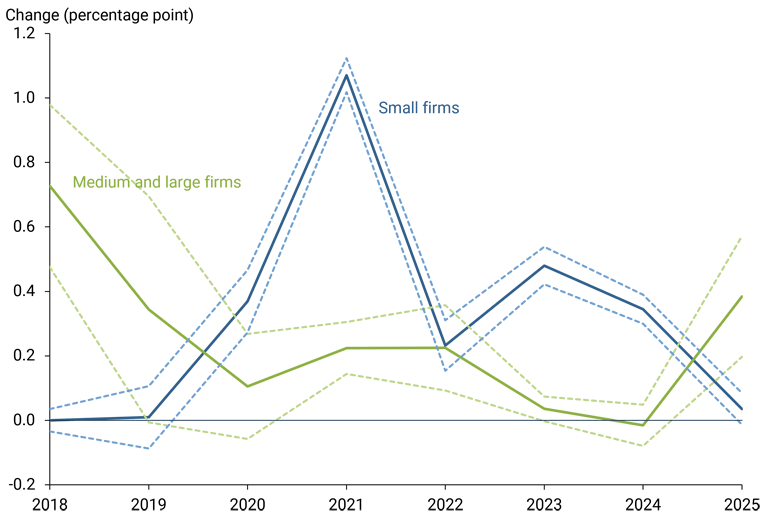

To better understand this divergence, we next analyze the estimated sensitivity of firms’ inflation expectations to their perceptions about current CPI inflation over time. Inflation expectations can be shaped by firm-specific perceptions of inflation if those firms don’t have access to complete information about overall inflation (Baumann et al. 2026). An example of this is the economic volatility during the inflation surge.

To examine this, we use the data SoFIE gathers by asking firms about their perceived CPI inflation rate over the previous 12 months. The perceived inflation rate is not necessarily the same as the realized inflation rate. Inflation perceptions can be different from actual, economy-wide inflation when firm managers observe specific sets of prices—for example, based on a company’s location or a different mix of production inputs across sectors. We estimate the relationship between one-year-ahead inflation expectations and perceived inflation for small and medium to large firms.

Figure 3 reveals that the sensitivity of inflation expectations to perceived inflation increased markedly for small firms in 2021. This timing coincides with when small firm inflation expectations diverged from those of larger firms. In 2021, a 1 percentage point increase in perceived inflation was associated with 1 percentage point higher one-year-ahead inflation expectations for small firms but with only 0.2 percentage point higher one-year-ahead expectations for larger firms. During the 2023-2025 period, the relative difference in sensitivity for small firms’ expectations declined. This helps explain why expectations across firm sizes mostly converged during the 2024-2025 period.

Figure 3

Sensitivity of inflation expectations to perceived inflation

Our findings suggest that small firms’ inflation expectations increased strongly because their overall sensitivity to current inflation was temporarily higher during the inflation surge. However, since then and through the end of 2025, both the levels of estimated sensitivity and the differences between small and larger firms’ inflation expectations have returned to pre-pandemic levels.

Did firms’ longer-term inflation expectations move?

While monetary policymakers expect short-run inflation expectations to change in response to the business cycle and various transitory shocks, changes in long-term inflation expectations are different. A key concern for monetary policymakers is ensuring that people continue to believe inflation is “well-anchored” and will return to the Fed’s 2% goal over time.

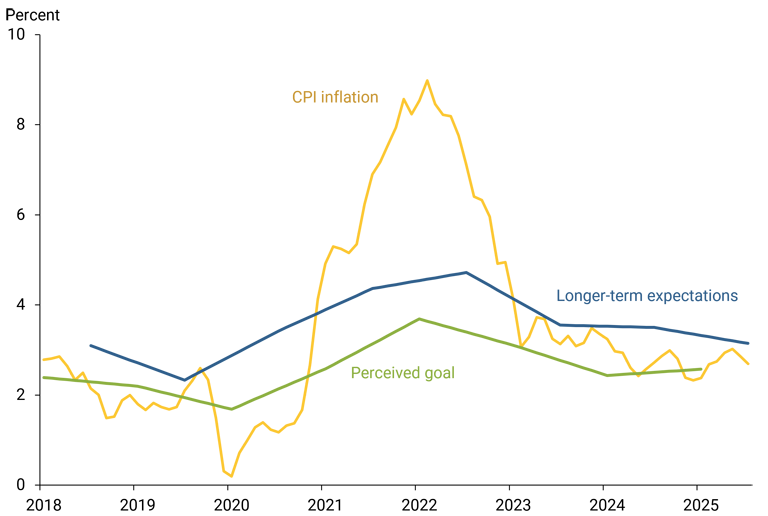

We construct a proxy for long-term inflation expectations based on firms’ one-year-ahead expectations, as analyzed above, and their five-year expectations, which are also available in SoFIE. We combine both expectations to calculate firms’ expected average inflation rate between one year and five years from the current period.

Figure 4 shows that average longer-term inflation expectations rose from slightly above 2% in late 2019 to 4.8% in late 2022. Since late 2023, longer-term expectations gradually fell and stood at 3.3% in late 2025.

Figure 4

Longer-term expectations and perceived inflation goal

Firms’ longer-term inflation expectations thus deviated from their pre-pandemic level. However, that deviation appeared to be temporary. Following a cycle of policy rate hikes and the ensuing disinflation, longer-term inflation expectations receded and approached pre-pandemic levels.

These patterns suggest that, while longer-term expectations temporarily rose during the inflation surge, the disinflation and surrounding policy actions may have contributed to restoring stability in longer-term expectations. Our result echoes findings in Cline et al. (2026), who consider an anchoring measure to capture both the level and dispersion in firms’ longer-term inflation expectations.

Role of firms’ perceptions of the Federal Reserve’s inflation goal

Beyond the influence of fluctuations in current inflation rates, economic theory suggests that firms’ beliefs about the central bank’s inflation goal matter for their longer-term inflation expectations.

To collect firms’ perceptions of the Fed’s inflation goal, SoFIE respondents were asked about the inflation rate that the Fed is trying to achieve on average. The co-movement between firms’ longer-term expectations and their perception of the Fed’s inflation goal indicates to what extent changes in longer-term expectations can be explained by changing perceptions of the inflation goal.

Figure 4 shows firms’ average perceptions of the inflation goal and their longer-term inflation expectations. During the pre-pandemic period up until 2021, the perceived inflation goal was relatively stable. However, following the sharp increase in inflation, both longer-term expectations and the perceived inflation goal increased in 2022 and 2023. This suggests that higher inflation goal perceptions appear to have contributed to higher longer-term inflation expectations. After 2023, following the policy rate hiking cycle and lower inflation rates, firms’ perceived inflation goal fell, potentially explaining the decline in longer-term inflation expectations towards pre-pandemic levels.

These findings indicate that, throughout the inflation surge, fluctuations in the perceived inflation goal itself played a role in forming longer-term inflation expectations among businesses. The observed fluctuations suggest that episodes of persistently elevated inflation can influence firms’ perceptions of the Fed’s inflation goal and that moderation in inflation can restore the accuracy of inflation goal perceptions.

Conclusion

Our analysis of firms’ inflation expectations during the 2018–2025 period in this Letter reveals several key patterns: Firms’ expectations were less stable than those of professional forecasters and became similar to the more volatile household expectations. This shift was more pronounced for small firms, whose sensitivity to current inflation perceptions increased especially strongly during the inflation surge. Firms’ longer-term inflation expectations also rose during 2021–2023 but both measures have since declined toward pre-pandemic levels. Some of the increase in firms’ longer-term inflation expectations can be accounted for by higher perceptions of the Federal Reserve’s inflation goal. However, the experience during the pandemic-era inflation surge suggests that disinflationary dynamics and monetary policy actions can also shape firms’ inflation expectations and their perceptions of the Federal Reserve’s inflation goal.

References

Baumann, Ursel, Annalisa Ferrando, Dimitris Georgarakos, Yuriy Gorodnichenko, and Timo Reinelt. 2026. “Firms’ Inflation Expectations in a Monetary Union.” Journal of the European Economic Association, jvag022.

Candia, Bernardo, Olivier Coibion, and Yuriy Gorodnichenko. 2023. “The Macroeconomic Expectations of Firms.” In Handbook of Economic Expectations, edited by R. Bachmann, G. Topa, and W. van der Klaauw. Academic Press, pp. 321–353.

Cline, Alexander, Christian Garciga, Ina Hajdini, Timo Reinelt, and Robert W. Rich. 2026. “The (Re-)Anchoring of U.S. Firms’ Inflation Expectations.” Federal Reserve Bank of Cleveland Economic Commentary 2026-11.

Garciga, Christian, Edward S. Knotek II, Mathieu Pedemonte, and Taylor Shiroff. 2023. “The Survey of Firms’ Inflation Expectations.” Federal Reserve Bank of Cleveland Economic Commentary 2023-10.

Kumar, Saten, Hassan Afrouzi, Olivier Coibion, and Yuriy Gorodnichenko. 2015. “Inflation Targeting Does Not Anchor Inflation Expectations: Evidence from Firms in New Zealand.” Brookings Papers on Economic Activity 46(2), pp. 151–225.

Data

Download data for figures (Excel, 591 kb)

Opinions expressed in this FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco, the Federal Reserve Bank of Cleveland, or the Board of Governors of the Federal Reserve System.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org