Extreme heat decreases labor productivity in sectors like construction, where much work occurs outdoors. Because construction is an important component of investment, lost productivity today will slow how much capital is built up for future use and thus can have long-lasting impacts on overall economic outcomes. Combining estimates of lost labor productivity due to extreme heat with a model of economic growth suggests that, by the year 2200, extreme heat will reduce the U.S. capital stock by 5.4% and annual consumption by 1.8%.

Extreme heat makes it more difficult to perform physical labor. In the United States, this is particularly relevant for agriculture, mining, and construction, where a substantial share of production takes place outdoors. Data from the Bureau of Economic Analysis show that, of these three sectors, construction contributes the most to economic output, which suggests that the impact from lost labor activity due to extreme heat will largely be driven by the effects on the construction sector.

The labor productivity losses in construction today could have long-lasting effects on the U.S. economy because construction is important for investment. Investment is the purchase of capital in the form of goods or services. Thus, if extreme heat lowers investment today, then it will slow the accumulation of capital for future use and have long-lasting impacts on economic outcomes.

In this Economic Letter based on Casey, Fried, and Gibson (2024), we combine economic theory with findings from the climate science literature to project the future economic impacts of U.S. labor productivity losses from extreme heat. We find that future increases in days of extreme heat can be expected to reduce the amount of accumulated capital by approximately 5.4% in 2200 and reduce annual consumption by approximately 1.8%.

Extreme heat and worker productivity

When a person works on a physically intensive task, the body must release heat to maintain a safe internal temperature. If it is not possible to release enough heat, the person can suffer from heat stress. Scientists use wet bulb globe temperature (WBGT), which incorporates the ambient air temperature, humidity, wind speed, and solar irradiance, to determine when people are at risk of heat stress. Rising temperatures increase the risk of heat stress for workers in settings without climate control, such as those who work outdoors.

Worker safety organizations, such as the Occupational Safety and Health Administration, as well as the U.S. military provide guidelines for how much effort individuals can safely exert under different climate conditions. Dunne, Stouffer, and Johns (2013) analyze these guidelines and find that they are consistent across organizations. For “heavy work” that is characteristic of construction and agriculture, the guidelines suggest that heat stress becomes a concern at a WBGT of 25 degrees Celsius (°C), equivalent to 77 degrees Fahrenheit (°F), and that it is not safe to do any work outdoors when WBGT is above 33°C (91°F).

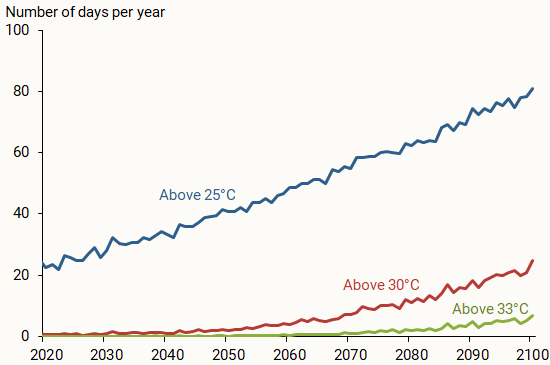

Figure 1 projects the future vulnerability to heat stress for an outdoor worker in the United States, measured in days above certain WBGT thresholds. To construct the figure, we use projections of future weather conditions at the county-level from Rasmussen, Meinshausen, and Kopp (2016). The projections are based on a scenario that assumes no large-scale efforts to limit carbon emissions. To aggregate these projections to the national level, we take a weighted average across counties, where the weights are fixed over time and determined by the current level of outdoor employment in each county.

Figure 1

Projected number of days above WBGT thresholds

Source: Author’s calculations using weather data from Rasmussen et al. (2016) and county-level outdoor employment form the U.S. Census Bureau.

The results suggest that future changes in climate will increase exposure to extreme heat for outdoor workers in the United States. The number of days above 25°C for these workers rises substantially between 2020 and 2100, from 22 days to 80 days per year. The number of days above 33°C increases from near zero to almost seven.

Why construction?

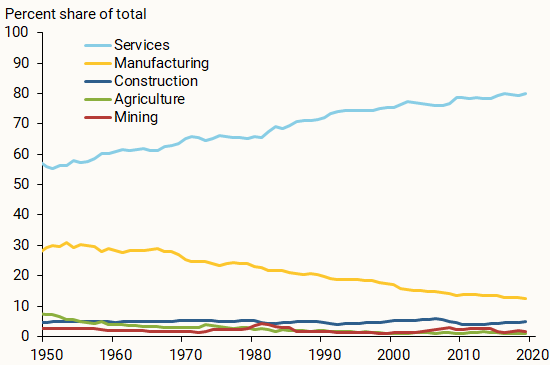

To understand how labor productivity losses from extreme heat could affect the economy, Figure 2 divides U.S. economic output from 1950 to 2019 into five sectors: services, manufacturing, construction, mining, and agriculture.

Figure 2

Composition of U.S. economic output

Services (light blue line) and manufacturing (yellow line) play the largest role in the U.S. economy, but they are unlikely to be highly affected by heat. This is because work in these sectors is largely performed indoors and U.S. businesses generally have access to air conditioning (Nath 2022). On the other hand, agriculture, construction, and mining are more likely to entail outdoor work. Among these outdoor sectors, construction makes up the largest share of overall U.S. output. The construction share (dark blue line) has been relatively constant over time, equal to approximately 4%. In contrast, the share of agriculture (green line) has fallen over time and equaled less than 0.2% of output in 2019. The share of the mining sector (red line) has been consistently less than 1%. Projecting these trends into the future, we expect that construction is likely to determine the overall vulnerability of U.S. production to extreme heat.

These results do not imply that the impact of extreme heat on U.S. agriculture and mining is unimportant. Extreme heat’s impact on U.S. agricultural productivity could affect food prices around the world, which could have a disproportionate effect on low-income individuals in the United States and in developing countries. Moreover, these impacts could have negative consequences for U.S. workers in agriculture and their local communities. Relative to the larger share of construction, however, agriculture and mining are not as likely to drive national outcomes.

Consumption versus investment

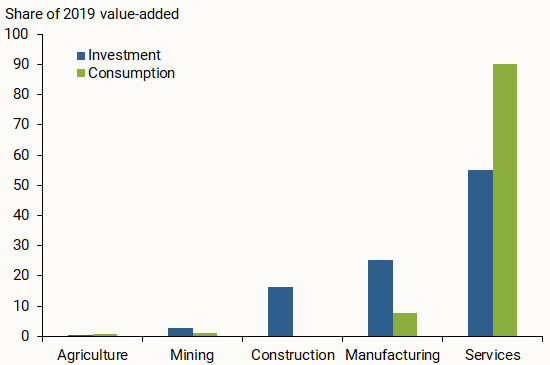

Economic output can be used for consumption or for investment. Consumption refers to households’ purchases of goods and services, such as food or haircuts, that increase well-being today. Investment refers to purchases of goods and services that are used to produce output in the future, and thus increase well-being in the future. This includes spending by businesses on things like factories and software, as well as the purchase of homes by households. The distinction between consumption and investment matters because a decrease in consumption reduces well-being today but has no impact on future economic outcomes. In contrast, a decrease in investment has no impact on well-being today, but it reduces the accumulation of capital, making it harder to produce both consumption and investment goods and services in the future.

Figure 3 shows the contribution of the five sectors from Figure 2 to consumption and investment. The construction sector is an important component of U.S. investment, accounting for over 20% of investment value-added. Thus, a decrease in construction productivity from extreme heat would reduce investment and thereby have a long-lasting impact on the economy.

Figure 3

Composition of U.S. consumption and investment

The future consequences of increases in extreme heat

To determine the impact of labor productivity losses from extreme heat, we build and simulate an economic model designed to study the impact of sectoral productivity on macroeconomic outcomes. Dunne et al. (2013) provide estimates of how WBGT affects labor productivity in outdoor work. We combine these estimates with the future paths of WBGT shown in Figure 1 to project future changes in productivity in the outdoor sectors. We then feed these reductions in outdoor productivity into our model.

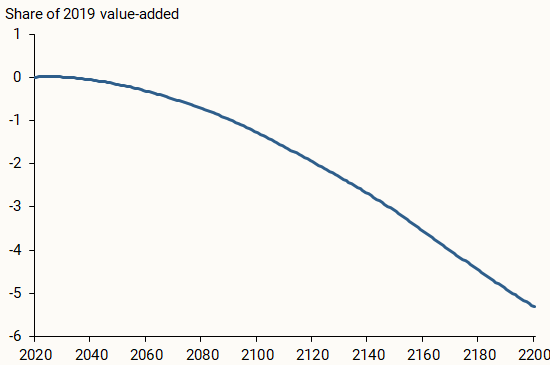

Figure 4 shows the impact of extreme heat on the capital stock in our model. The capital stock is the value of accumulated investment, an important determinant of an economy’s ability to produce output. We compare the size of the capital stock under the scenario depicted in Figure 1 to the size of the capital stock when there is no change in extreme heat exposure after 2019. We find that future increases in extreme heat would lower the capital stock by about 1.4% in 2100 and by 5.4% in 2200. The lower capital stock reduces the economy’s ability to produce output, which in turn reduces consumption. Thus, we find that extreme heat reduces annual consumption by 0.5% in 2100 and 1.8% in 2200.

Figure 4

Impact of extreme heat on capital accumulation

The WBGT paths in Figure 1 and our results in Figure 4 correspond to the most likely climate outcome given a particular path of carbon emissions. However, there is considerable uncertainty over these climate outcomes. As a result, some economists argue that it is important to consider the consequences of other less likely but still possible outcomes (Weitzman 2009). To do so, we simulated the economic effects of an alternative outcome with only a 5% likelihood that retains our given path of carbon emissions but has a larger increase in number of extreme heat days. For example, in that outcome, the number of days with WBGT greater than 25°C increases from 22 in 2020 to 125 in 2100, as opposed to from 22 to 80 as assumed in our main analysis. The outcome would lead to considerably larger consequences from extreme heat, reducing capital accumulation by 18% in 2200 and consumption by 7%.

Some caveats are in order when interpreting the magnitudes from our analysis. We abstract from some ways that companies could adapt to extreme heat, such as relocating production to cooler parts of the United States or shifting work hours to cooler parts of the day. Additionally, while our focus is on the overall consequences of extreme heat on U.S. labor productivity, the effects could vary across income groups and regions of the country. One could also consider the effects of extreme heat in other countries. For example, the impacts are likely to be larger in developing countries, where agriculture is a bigger fraction of output and where work in manufacturing and services is less likely to take place in climate-controlled environments. Finally, the increases in extreme heat days that we study could be paired with decreases in extreme cold days, which could in turn have different implications for labor productivity.

Conclusion

This Letter studies the impact of extreme heat on long-run economic outcomes in the United States. Extreme heat is most likely to affect economic outcomes through the construction sector for two reasons. First, construction makes up a larger share of economic output than other vulnerable sectors, like agriculture. Second, decreases in construction productivity slow capital accumulation and therefore have long-lasting effects on macroeconomic outcomes. Our findings suggest that, under a scenario with no large-scale efforts to reduce carbon emissions, future increases in extreme heat would reduce the capital stock by 5.4% and annual consumption by 1.8% by the year 2200.

References

Casey, Gregory, Stephie Fried, and Matthew Gibson. 2022. “Understanding Climate Damages: Consumption versus Investment.” FRB San Francisco Working Paper 2022-21.

Dunne, John P., Ronald J. Stouffer, and Jasmin G. John. 2013. “Reductions in Labour Capacity from Heat Stress under Climate Warming.” Nature Climate Change 3(6), pp. 563–566.

Nath, Ishan B. 2022. “Climate Change, the Food Problem, and the Challenge of Adaptation through Sectoral Reallocation.” National Bureau of Economic Research Working Paper 27297.

Rasmussen, D.J., Malte Meinshausen, and Robert E. Kopp. 2016. “Probability-Weighted Ensembles of U.S. County-Level Climate Projections for Climate Risk Analysis.” Journal of Applied Meteorology and Climatology 55(10), pp. 2,301–2,322.

Weitzman, Martin L. 2009. “On Modeling and Interpreting the Economics of Catastrophic Climate Change.” Review of Economics and Statistics 91(1), pp. 1–19.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org