Following the global financial crisis, U.S. monetary policy was constrained by the zero lower bound for short-term interest rates for many years. It has since lifted off and rates have gradually climbed. However, in light of the continuing economic expansion, it is relevant to ask how likely it is for the lower bound on interest rates to again become a constraint on monetary policy. Analysis using several different approaches suggests that there currently appears to be a low risk of the economy returning to the zero lower bound for at least the next several years.

Economic growth was slow in the aftermath of the global financial crisis in part because monetary policy was constrained by the effective lower bound in several major currency areas, including the United States. This constraint reflects an unavoidable consequence of currency being a readily available storage of wealth: if investors can hold cash, then it’s less attractive for them to tie up their money without earning interest in return. This effectively limits how low nominal interest rates can go.

Safe short- and medium-term interest rates remain near historical lows in many developed countries. This raises concerns about whether monetary policy could provide enough stimulus during any future economic downturns. Therefore, more than 10 years after the crisis, it remains relevant for the Federal Reserve to ask what the risk is of the overnight federal funds rate—the main policy rate in the United States—again being constrained by the zero lower bound (ZLB).

In this Letter, I consider evidence regarding this question from three different sources. I use an established dynamic model of the Treasury yield curve to assess the risk of the Fed’s policy rate returning to the ZLB. My results are consistent with evidence from the New York Fed’s Survey of Primary Dealers and with analysis based on a Federal Reserve Board model of the overall economy (Nakata 2017). Despite notable differences across the three sources, they all suggest that the risk of returning to the ZLB within the next three years is low and should not pose a concern for monetary policy at this time.

The yield curve model

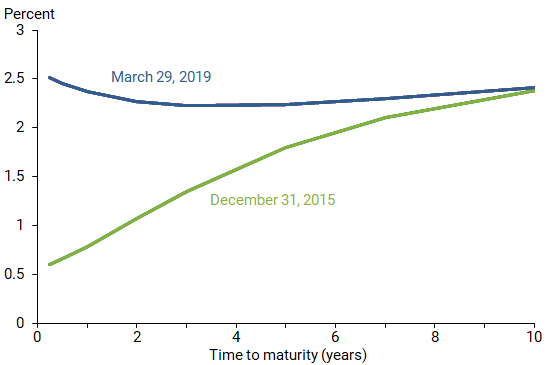

The odds of returning to the ZLB are partly a function of the level of interest rates; those rates, in turn, reflect the current and expected future economic conditions. Figure 1 shows the change in the Treasury yield curve between the end of 2015—when the Fed started raising short-term rates, normalizing monetary policy after having been constrained by the ZLB for seven years—and the end of March 2019. Each line shows the yield to maturity of the range of three-month to 10-year Treasury bonds. Note that short-term yields have increased about 2 percentage points in tandem with the Fed’s normalization of monetary policy between those two dates. Medium- and longer-term yields have increased less. This shows that normalization has reduced the immediate risk of the rate returning to zero. However, measuring this risk over the longer run requires disentangling the expectations about future short rates investors use when trading Treasury bonds from the premiums they demand for assuming the risk of holding those securities.

Figure 1

Change in the Treasury yield curve

To account for the variation in the Treasury yield curve and isolate the embedded information about bond investors’ expectations for future short-term rates, I use a model that describes the relationship between bond yields of different maturities, known as a term structure model. Specifically, I use the model of the Treasury yield curve identified by Christensen and Rudebusch (2012), denoted the CR model. This model assumes that yield variability can be summarized by three factors: the general level of interest rates, the slope of the yield curve, and any humps in the shape of the yield curve. The factors are latent and therefore only indirectly reflect the connection between the state of the economy and the stance of monetary policy. According to the model, the constellation of the three factors implied by the current Treasury yield curve and their historical dynamic relationship determine the probability of a given level and shape of the Treasury yield curve in the future.

With daily data on Treasury yields from December 1, 1987, through March 29, 2019, I use the model to estimate the shape of the Treasury yield curve and investors’ embedded forward-looking expectations as of March 29. Using these estimates, I project 10,000 possible paths for the Treasury yield curve up to 10 years ahead. Along each 10-year path, I project yields at monthly intervals, focusing on the model-implied overnight rate as a representative of the level of short-term interest rates in each period.

The median overnight rate projection indicates that the trend in short-term rates is expected to continue to climb modestly to a peak of 2.65% towards the end of 2019 before gradually falling back to a stable longer-run level close to 2.40%. Considering the range of results, the upper 95th percentile implies a much quicker and more forceful continued normalization of monetary policy with a peak well above 5% in the summer of 2025. In contrast, the lower 5th percentile shows monetary policy could become constrained by the ZLB within three years. This wide range of possible outcomes underscores the inherent uncertainty in making economic projections even in the near future. These simulations represent an update of the projections reported in Christensen (2018). From the point of view of the CR model, the recent slight inversion of the Treasury yield curve shown in Figure 1 was a very likely outcome given the shape of the yield curve as of the August 2018 update.

Risk of returning to the ZLB

To study the risk of short-term interest rates being constrained again by the ZLB and how its likelihood has varied over time, I follow Nakata (2017) and limit the time horizon to three years. This corresponds to the typical timeframe for a medium-term economic forecast. I consider the federal funds rate to be constrained by the ZLB if, at any time within the next three years, it falls below 0.25% and stays there for at least a quarter.

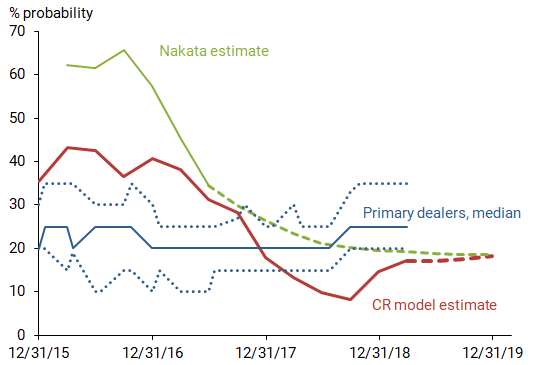

To assess the risk from December 2015 through March 2019, I estimate the CR model at the end of each quarter and repeat the model simulations. The solid red line in Figure 2 shows the probability of returning to the ZLB using these estimates. The likelihood started out high, around 40% right after liftoff in December 2015. Since then it has fallen steadily in tandem with the Fed raising rates, although it has ticked up modestly since the fall of 2018. As of March 29, 2019, it was 17%. I also use the CR model’s median to project the future risk estimates, shown with a dashed red line. It indicates a further slight uptick towards a longer-run level slightly below 20%; this is consistent with the model’s median projection that peaks close to 2.65% at the end of 2019 before reversing to a lower long-run level near 2.40%.

Figure 2

Probability of returning to the ZLB within the next three years

Comparison to surveys and a macro model

To put the estimated probabilities from the CR model into perspective, I compare them with two other sources. The first is the Survey of Primary Dealers (SPD), collected by the Federal Reserve Bank of New York before each scheduled FOMC meeting. Since before the liftoff, primary dealers—brokers or financial institutions that buy and sell Treasury securities directly with the Fed—have been asked how probable it is for rates to move back to the ZLB sometime in the next two or three years. Although the exact forecast horizon varies depending on the time of the year of the survey, I treat the results as reflecting three-year projections for simplicity.

In Figure 2, the solid blue line represents the median projection since December 2015, as well as the range of projections 25% above and below the median (dashed blue lines). The median projection has fluctuated in a narrow range between 20 and 25% probability and exhibits little sensitivity to the variation in the interest rate level.

The second source is based on the FRB/US model, which is an empirical macro model of the U.S. economy maintained by staff at the Federal Reserve Board. Nakata (2017) combines this model with the median projections for key economic variables reported in the SPD to estimate the risk of returning to the ZLB within the next three years. This macro-based estimate (green line) was above 60% during most of 2016 before declining to about 35% by mid-2017, which put it very close to the CR model estimate.

Nakata (2017) also projects the future risk (dashed green line) assuming the economy follows the median projection from the June 2017 SPD. The projection suggests that the probability of returning to the ZLB within three years will continue to decline and approach a long-run level slightly below 20%.

To summarize, all three sources suggest that there is a relatively small chance of the U.S. economy going back to the ZLB within the next couple of years, and this risk is likely to remain low in the foreseeable future.

An important caveat for the yield-based analysis is that long-term Treasury yields have been unusually low for many years (Bauer and Rudebusch 2016), which is reflected as increased factor persistence and lower factor mean values in the estimated model dynamics. This could be caused either by declines in the risk-free, or natural, real rate from low productivity or an aging population (Christensen and Rudebusch 2017), or by the massive long-term asset purchases by the world’s major central banks in the aftermath of the global financial crisis (Bonis, Ihrig, and Wei 2017). If these factors were viewed as transitory and expected to reverse within the forecast horizon, they would make the CR model overstate the chance of returning to the ZLB in that it would overstate the likelihood of simulated paths close to the ZLB. A caveat for the macro model is that the shocks used in the simulations may have excess volatility. Nakata (2017) demonstrates that dropping shocks from the volatile 1970s and 1980s lowers the risk of returning to the ZLB. Thus, adjusting for any of the above effects would be likely to lead to lower risk estimates.

Conclusion

In this Letter, I assess the risk of U.S. short-term interest rates being constrained by the zero lower bound as they were between 2009 and 2015. Based on analysis of a dynamic model of U.S. Treasury yields complemented with evidence from surveys and a standard macro model of the U.S. economy, I find a low likelihood of this outcome, particularly in the near future. Hence, at this time, it appears sensible not to put too much emphasis on this concern, especially in light of the potential for structural factors to cause the estimated risk to be overstated.

Jens H.E. Christensen is a research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Bauer, Michael D., and Glenn D. Rudebusch. 2016. “Why Are Long-Term Interest Rates So Low?” FRBSF Economic Letter 2016-36 (December 5).

Bonis, Brian, Jane Ihrig, and Min Wei. 2017. “The Effect of the Federal Reserve’s Securities Holdings on Longer-Term Interest Rates.” Federal Reserve Board of Governors FEDS Notes, April 20.

Christensen, Jens H.E. 2018. “The Slope of the Yield Curve and the Near-Term Outlook.” FRBSF Economic Letter 2018-23 (October 15).

Christensen, Jens H.E., and Glenn D. Rudebusch. 2012. “The Response of Interest Rates to U.S. and U.K. Quantitative Easing.” Economic Journal 122, pp. F385–F414.

Christensen, Jens H.E., and Glenn D. Rudebusch. 2017. “New Evidence for a Lower New Normal in Interest Rates.” FRBSF Economic Letter 2017-17 (June 19).

Nakata, Taisuke. 2017. “Model-Based Measures of ELB Risk.” Federal Reserve Board of Governors FEDS Notes, August 23.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org