Mark Spiegel, vice president at the Federal Reserve Bank of San Francisco, provides his views on current economic developments and the outlook.

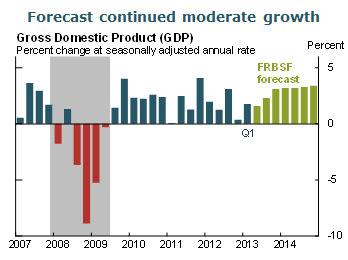

- Recent data have remained consistent with a moderate recovery. The latest Institute for Supply Management survey suggests a pickup in manufacturing activity in June after some softness earlier this year. We have also seen some bright spots in consumption. However, the economy is still experiencing a drag from fiscal austerity. As fiscal and other headwinds wane, we expect growth to pick up in the second half of this year and into next year. On balance, we continue to expect GDP growth to reach about 2¼% overall for 2013 and increase to 3¼% in the next year.

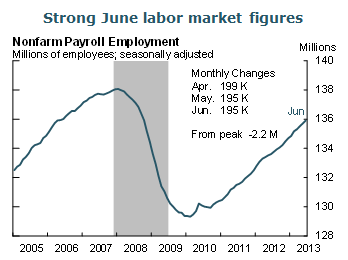

- The June employment report came in stronger than expected. Overall job gains were 195,000, far above the expected 165,000. In addition, April and May figures were revised upward. Overall, the economy has gained an average of approximately 200,000 jobs per month in the first half of 2013. The unemployment rate remained at 7.6%, primarily because of a modest uptick in labor force participation.

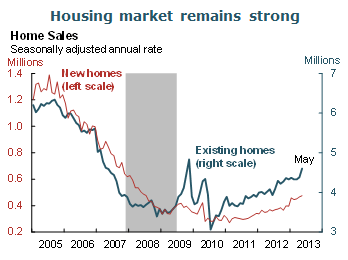

- Housing and real estate activity remain strong. The National Association of Realtors Pending Home Sales index rose 6.7% in May, far above expectations. Housing prices have also increased markedly, with the seasonally adjusted CoreLogic national Home Price Index increasing 1.1% from the previous month. Over the past year, this index is up about 12%.

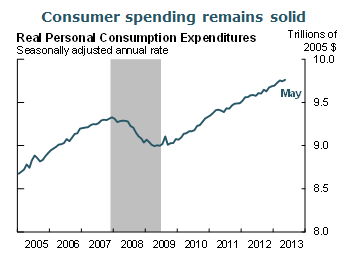

- Ongoing strength in housing appears to be playing a supporting role in maintaining consumption. Consumer sentiment, while modestly below its May high, remains strong. Personal consumption expenditures (PCE) continued to move up in May; combined with a downward revision to April figures, however, expenditures were essentially flat over the two months.

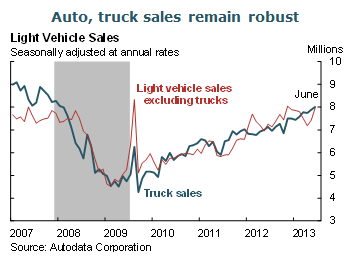

- Motor vehicle sales have been particularly strong. Light vehicle sales rose in June to their highest levels during the recovery, at a 15.96 million unit annual rate. Here again, the strength in the housing market, combined with low prevailing interest rates that ease the cost of auto finance, appears to be playing a role. The positive influence of housing on motor vehicle sales is reflected in the recent strong performance of truck sales, which may be motivated in part by housing-related activities such as construction.

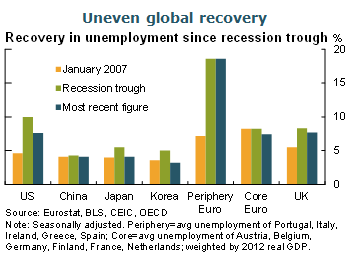

- The trade deficit grew to $45 billion in May. Exports of goods were close to flat, while imports continued to grow. Europe remains a source of substantial risk to our forecast. While the risks of euro-area dissolution appear diminished, European fiscal austerity measures—particularly among countries in the European periphery—have been a drag on economic performance in the region. While European labor markets have improved only modestly, Asian labor markets have largely recovered from the global financial crisis in terms of unemployment. These different experiences have created an uneven global recovery.

- In addition to the implications of Europe’s slow recovery on U.S. exports, weak demand in Europe also appears to be weighing on Asian exports to that region. For example, Chinese exports declined 3.1% year-to-year in June. However, some commentators speculated that the decline was attributable in part to stricter enforcement of trade accounting standards. The crackdown may have reversed some overstatement of past export levels.

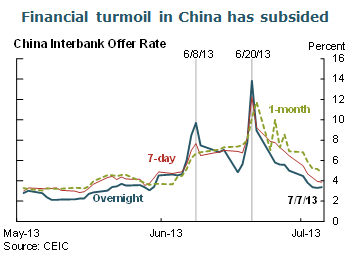

- Financial conditions in China tightened in June. Seasonal conditions that raised demand for cash among financial institutions at the end of the quarter were initially not accommodated by the Peoples’ Bank of China (PBOC). In the past, the PBOC has injected liquidity into the financial system to meet this demand, either through reverse repos or through a reduction in reserve requirements. There was some speculation that the PBOC’s reluctance to pursue past policies may have been associated with a desire to curb riskier lending activities that were particularly exposed to end-of-quarter liquidity difficulties. Interbank rates in China rose dramatically, but fell again after a PBOC statement that it would provide liquidity and stabilize interbank rate volatility.

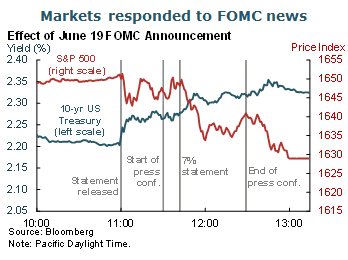

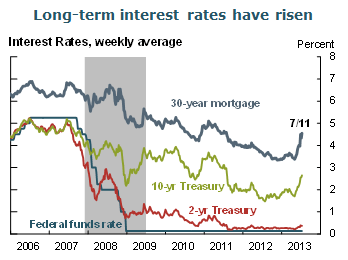

- Equity market values fell and bond yields increased after the June 19 Federal Open Market Committee (FOMC) meeting and subsequent press conference by Chairman Bernanke. Tick-by-tick data demonstrate that, while the markets moved somewhat in response to the FOMC statement and the release of the FOMC member forecasts, equities responded much more dramatically to the Chairman’s discussion of the of the possibility of ending the Federal Reserve asset purchase program in mid-2014, when the unemployment rate “would likely be in the vicinity of 7%.”

- After the June FOMC meeting, long-term interest rates continued to move upwards. By contrast, equity market indexes have recovered and reached record closing highs. This combination of bond market selling and a rally in equity markets appears consistent with growing market confidence in the strength of the underlying real economy.

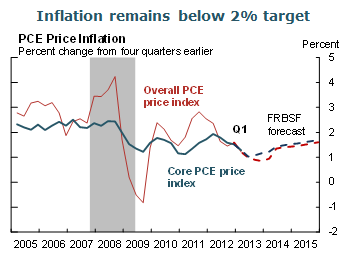

- Inflation remains low. The PCE price index rose 0.1% in May, in line with expectations. Core PCE increased 0.1% in May, also in line with expectations. The 12-month change in the core index was 1.1%, the same as in April, but down from 2% in March 2012. We project that inflation will rise gradually towards the FOMC’s 2% target.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.