Zheng Liu, senior research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of December 10, 2015.

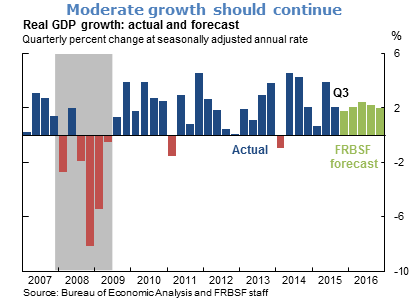

- Real GDP grew at an annual rate of 2.1% in the third quarter, according to the most recent estimate of the Bureau of Economic Analysis. Over the first three quarters of this year, real GDP has expanded at an average rate of 2¼%. This moderate growth pace reflects solid gains in private domestic final purchases, particularly household spending supported by increases in household income, declines in energy prices, and increases in housing and equity prices. However, overall growth has been partially restrained by weakness in net exports, reflecting the effects of recent dollar appreciation and deterioration in foreign economic conditions.

- We expect moderate growth to continue into next year, with real GDP rising at an average rate between 2% and 2¼%. Domestic spending should continue to support overall growth, while the adverse impact of dollar appreciation should wane over time.

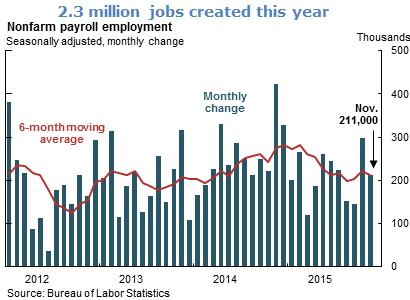

- Labor market conditions strengthened further. The U.S. economy added 211,000 new jobs in November after gaining 298,000 jobs in October, bringing the 6-month moving average of job gains well over 200,000 per month. Since early 2010, 13.2 million jobs have been created.

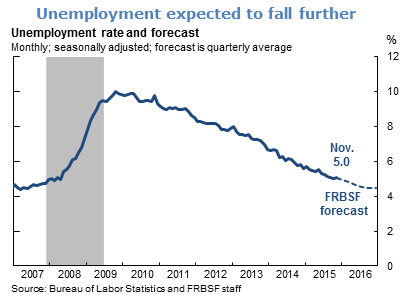

- The unemployment rate was unchanged in November, remaining at 5.0%. Although the labor force participation rate and the employment-to-population ratio remained low, broader indicators of labor-market slack such as the share of total unemployed plus those workers employed part-time for economic reasons and those marginally attached to the labor force have improved. We expect the unemployment rate to decline further through 2016 before returning to its long-run natural rate of about 5%.

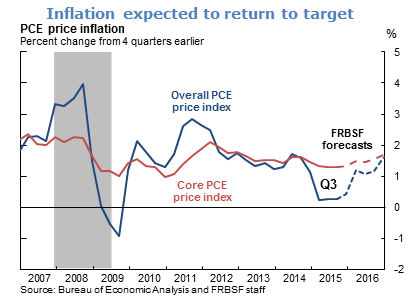

- Consumer price inflation as measured by the change in the price index of personal consumption expenditures (PCE) was 0.22% in the 12 months ending in October, reflecting steep declines in energy prices. Excluding the volatile food and energy components, core inflation ran at 1¼% in the 12 months ending in October. Both overall and core inflation rates are well below the Federal Reserve’s 2% target. Going forward, we expect the transitory effects of the dollar appreciation and energy prices to diminish and wage growth to strengthen. As a result, inflation should rise gradually toward the 2% target.

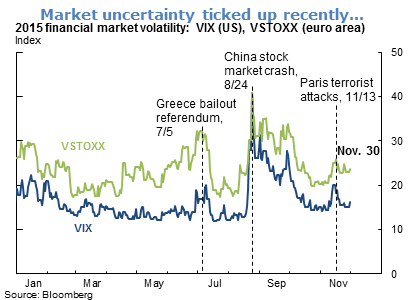

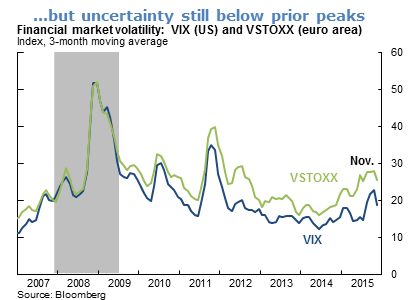

- Global uncertainty has increased in the last half of the year. Measures of financial uncertainty based on stock market volatility in both the United States (VIX) and the euro area (VSTOXX) rose in response to recent events including the Greece bailout referendum in July, China’s stock market crash in August, and the Paris terrorist attacks in November. However, the levels of uncertainty in both the United States and the euro area remained below their prior peaks during the global financial crisis in 2007-09 and the onset of the European debt crisis in 2011.

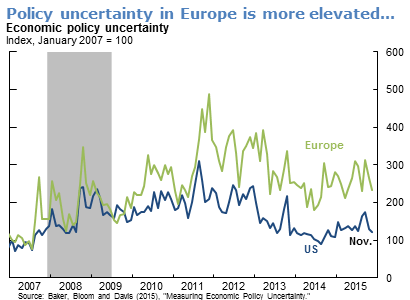

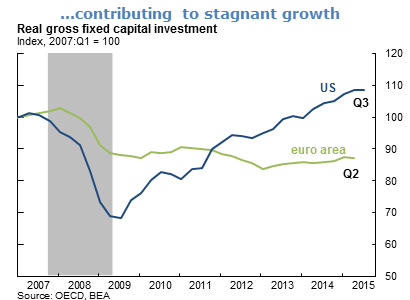

- Since the end of the global financial crisis, both market-based measures of financial uncertainty and economic policy uncertainty in Europe have been more elevated than in the United States. The relatively greater uncertainty has contributed to the euro area’s economic stagnation in recent years, particularly in investment spending.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.