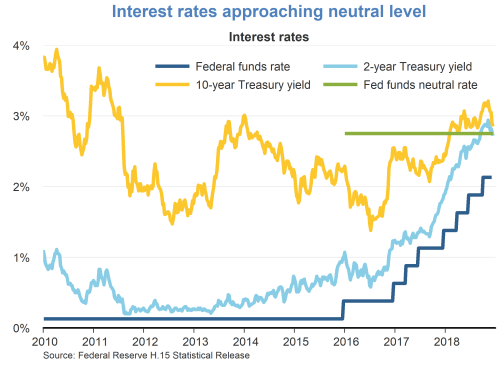

Zheng Liu, senior research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of December 13, 2018.

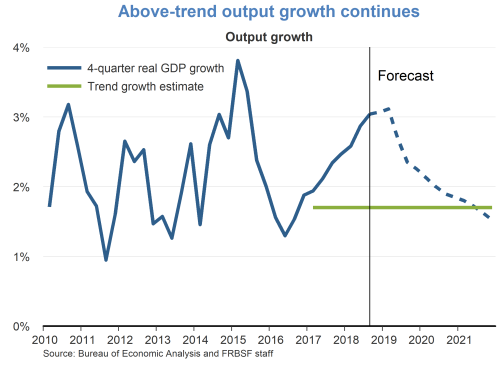

- The economy has continued to grow at a solid pace. After a strong second quarter, real GDP grew at an annual rate of 3.5% in the third quarter according to the second estimate of the Bureau of Economic Analysis. Despite recent financial market volatility and a cooling housing market, the fundamentals of the economy remain strong. We forecast that GDP will grow at an annual rate of 2.4% in the fourth quarter and average 3.1% for 2018. Over the medium term, as monetary policy continues to normalize and fiscal stimulus wanes, we expect growth to gradually fall back to our estimated long-term rate of 1.7%.

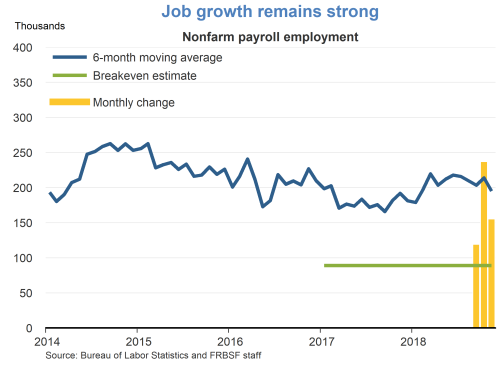

- The labor market has tightened further in recent months. The economy added 155,000 jobs in November, following the October gain of 237,000 jobs. Despite job gains being slower than expected in November, the economy added on average about 206,000 jobs per month this year. The pace of job growth significantly exceeded the breakeven rate, which we estimate at about 90,000 jobs per month.

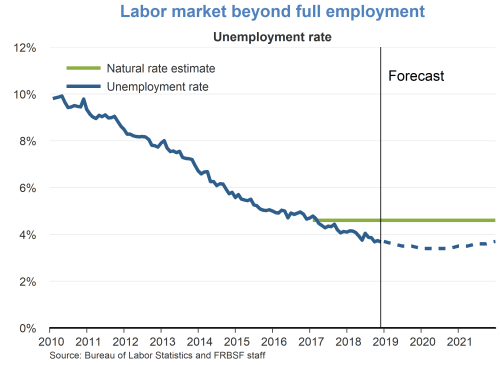

- The unemployment rate in November remained unchanged at 3.7%, the lowest reading since 1970. We expect it to decline to 3.4% by the end of next year as the labor market continues to tighten. Over the longer term, we expect the unemployment rate to return gradually to its natural rate of 4.5%.

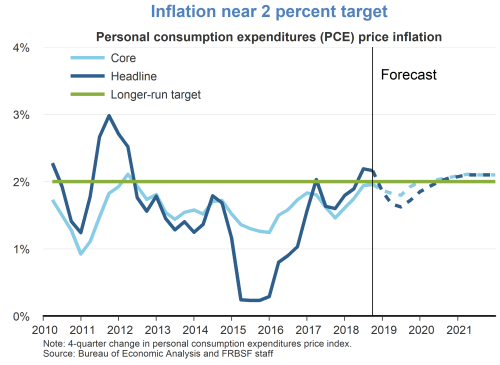

- Inflation has come close to the Federal Open Market Committee’s target of 2%. In October, the personal consumption expenditures (PCE) price index rose 2.0% over the past 12 months, and the core PCE price index, which excludes the volatile food and energy prices, rose 1.8%. The lower October reading of core inflation partly reflects the recent declines in the costs of health-care services, which are less sensitive to changes in overall economic conditions than other prices such as housing, restaurants, and recreation services; these effects are expected to be transitory. Declines in energy prices also put short-term restraints on headline inflation. As the labor market continues to strengthen and the effects of transitory factors diminish over time, we expect both headline and core inflation rates to slightly overshoot the 2% target by 2020.

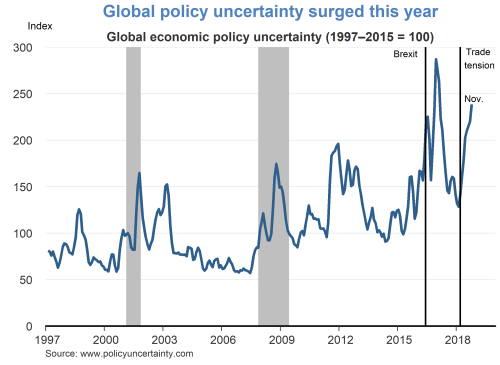

- A potential headwind for the U.S. economy is weaker global growth, partly attributable to the recent surges in global economic policy uncertainty. The elevated global uncertainty stems mainly from trade tensions between the United States and its major trading partners as well as political risks in Europe, particularly those associated with Brexit, the expected departure of the United Kingdom from the European Union. Recent trade agreements between the United States, Mexico, and Canada (the USMCA) and the temporary truce in the trade war between the United States and China have eased trade policy uncertainty to some extent.

- Global uncertainty can potentially spill over to the United States through trade relations. Elevated uncertainty induces a wait-and-see attitude and reduces business investment and hiring. Recent studies estimate that Brexit reduced U.K. business investment by 5%, or equivalently its GDP by 0.5%. Global uncertainty can also affect the U.S. economy through financial linkages. An increase in uncertainty raises demand for safer assets, such as U.S. Treasuries, leading to a stronger dollar and weaker export demand. However, capital inflows can also restrain increases in U.S. interest rates, providing an offset. With exports making up only 12.5% of its GDP, the spillover from global uncertainty to the United States is likely to be small.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.