Sylvain Leduc, executive vice president and director of research at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of April 11, 2019.

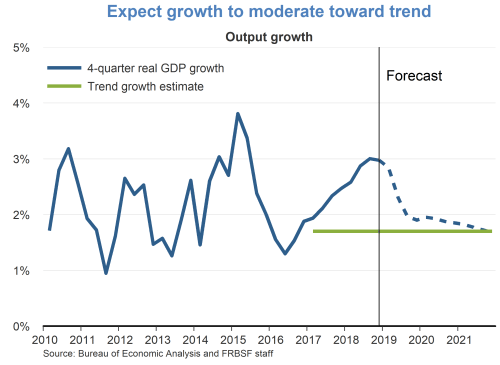

- The economy continues to grow, albeit at a slower pace than last year. Given the positive momentum, the economy is set to establish a new record this summer for the longest expansion in the post–World War II era. The expansion that started in June 2009 will then be more than 120 months, surpassing the previous record established between 1991 and 2001.

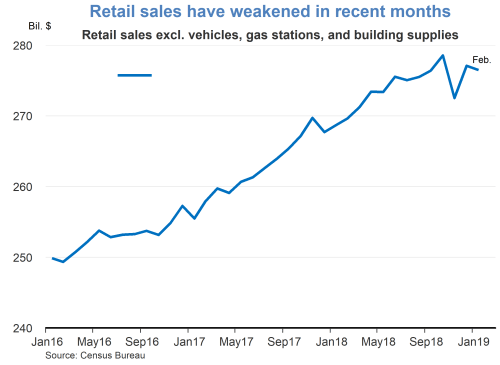

- Still, the data since the start of the year have been somewhat uneven, sending mixed signals about growth. Retail sales, an important indicator of consumer spending, appear to have slowed somewhat since November. Although January sales rebounded from December’s steep decline, sales in February remained soft. These data suggest that consumer spending is likely to be weak in the first quarter.

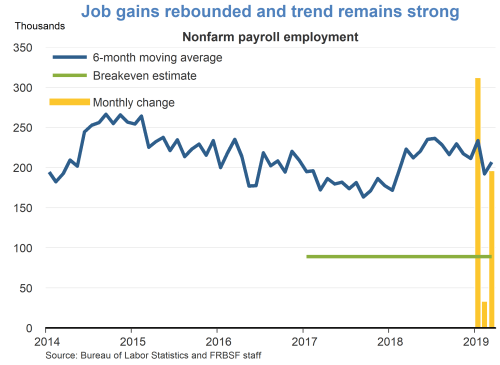

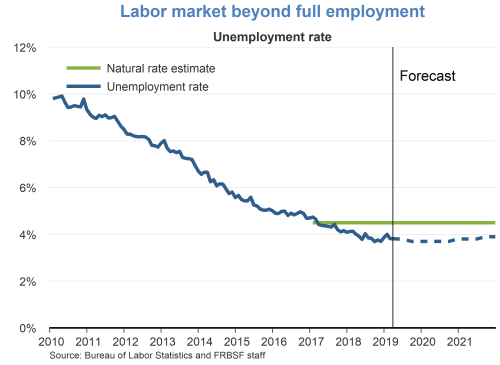

- In contrast, job gains rebounded strongly in March, with employers adding 196,000 new jobs compared with only 33,000 jobs the month before. The six-month moving average shows that employment gains remained above 200,000 jobs in March. The unemployment rate stayed at 3.8%, much lower than our estimate of its long-run natural rate of 4.5%. However, average hourly earnings growth eased off a bit in March, to 3.2%. That said, steady wage increases and continued job gains should help support consumer spending going forward.

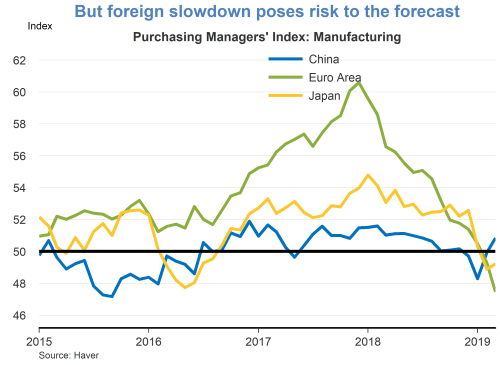

- Overall, we continue to expect growth to moderate to a more sustainable pace over the next two years. Past increases in interest rates and the fading boost from fiscal policy should partly contribute to this moderation. In addition, continued uncertainty surrounding trade policy is contributing to weaker growth abroad, as indicated by continued declines in Purchasing Managers’ Indexes for manufacturing in other countries, which in turn has weakened U.S. growth through lower growth in exports.

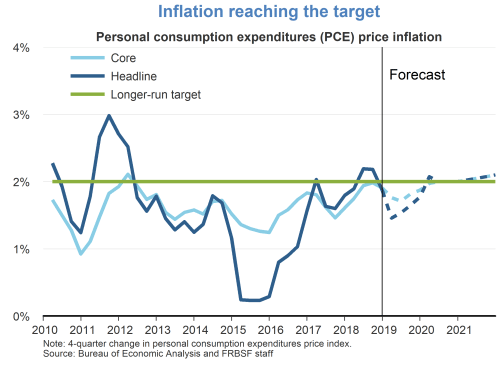

- Inflation remains muted. In January, the headline personal consumption expenditures (PCE) price index rose 1.4% from a year earlier, while core PCE inflation, which removes the volatile food and energy components, declined a tad to 1.8%. Partly due to the absence of inflationary pressures and continuing concerns about global economic and financial developments, the Federal Open Market Committee (FOMC) reiterated in March that it “will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate” to support its mandated goals of price stability and maximum employment.

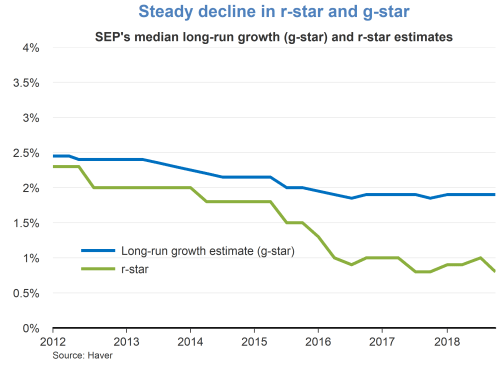

- Given continued economic growth, strong employment gains, and inflation close to target, the Federal Reserve announced in November 2018 that now is a good time to review its monetary policy strategy, tools, and communications. This review is also timely given that r-star, the long-run level of the policy rate consistent with full employment and inflation at target, has declined substantially over time. In particular, the Summary of Economic Projections shows a steady fall in r-star since 2012, in line with a fall in trend GDP growth. As a result, the federal funds rate, the FOMC’s primary monetary policy tool, is likely to hit the effective lower bound more often in the future, limiting its ability to stimulate the economy when conditions are weak.

- Although the Federal Reserve has other tools, such as forward guidance and quantitative easing, to conduct policy in such situations, Fed policymakers believe it is prudent to review different strategies that could be effective in helping the Fed achieve its mandated goals. While the review will be wide-ranging, it will not reconsider the 2% inflation target.

- Two proposed strategies to mitigate the constraint on monetary policy from the effective lower bound are price-level targeting and average-inflation targeting. In contrast to the current inflation-targeting framework, price-level and average-inflation targeting both embed so-called makeup properties.

- For instance, with an inflation-targeting approach, monetary policy leans against shocks that lower inflation to bring it back to target over the medium term. For example, if a negative price shock pushes inflation below the 2% target, monetary policy will be expansionary to return inflation to the target rate. However, this policy entails “drift” in the price level, as targeting the inflation rate does not fully make up for the effect of the negative inflation deviation from target on the price level. Thus, the price level will always be below the level that would have prevailed without the shock.

- In contrast, when monetary policy targets the price level—assuming, for instance, a target that would allow prices to grow at a 2% rate—Fed policymakers fully respond to price shocks in order to bring the price level back to target over time. This policy necessarily implies that shocks that push the price level below target, leading inflation to fall below 2%, must be made up in the future with above 2% inflation in order to meet the price-level target, resulting in an average inflation rate of 2%.

- The makeup property embedded in price-level targeting is attractive when recessions push monetary policy to the effective lower bound. In this case, any associated decline in the price level needs to be compensated in the future by allowing above 2% inflation for some time. Therefore, price-level targeting automatically entails more policy accommodations during effective lower bound episodes than an inflation-targeting framework.

- However, price-level targeting may be difficult to communicate, given that the public is used to focusing on inflation. In this case, average-inflation targeting may be a useful alternative. Simply targeting an inflation rate that is 2% on average would provide the same makeup property embedded in price-level targeting, but would be easier to communicate to the public.

- While these alternative policies may offer benefits, the bar for changing the current framework is high. In this context, the Federal Reserve is inviting a broad public discussion of its strategy, tools, and communications by conducting a Fed Listens tour around the country. We are delighted that this tour will include a stop in San Francisco in September to discuss the sustainability of running a hot economy.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.