Reuven Glick, group vice president at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of December 8, 2016.

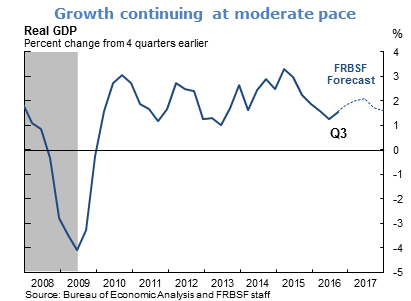

- Real GDP growth was revised up to an annualized rate of 3.2% in the third quarter from an initial estimate of 2.9%, confirming that the economy has picked up from its modest pace in the first half of the year when growth averaged only 1.1%. Growth is being driven primarily by healthy consumer spending, as business investment has been weak, particularly in the energy sector.

- We expect GDP growth to soften somewhat in the fourth quarter, as some of the third quarter strength was due to higher exports and an inventory rebound, and is likely to be transitory. Going into 2017 and beyond, the growth rate should slow somewhat to its long run trend of a little over 1-1/2%.

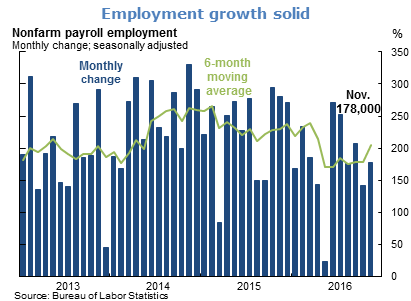

- Current job growth is consistent with a healthy labor market. Nonfarm payroll employment in November rose by 178,000 jobs. Over the past six months, payroll gains have averaged 205,000 per month. These numbers are well above our estimate of the “break-even” level of 80,000 new jobs per month needed to absorb new entrants to the job market.

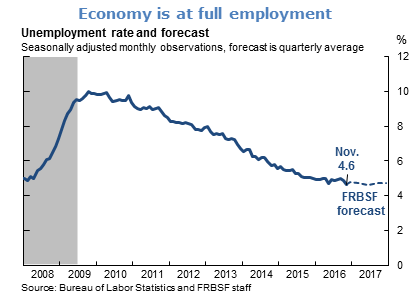

- The unemployment rate declined sharply in November, from 4.9% to 4.6%, the lowest level during the recovery period and below our estimate of the natural rate of unemployment of 5.0%. A broader measure of labor market slack which includes those who want to work but have stopped looking as well as those in part-time jobs who want full-time positions also moved down in November, from 9.5% to 9.3%. Most of these declines were due to lower labor force participation because more of the unemployed totally left the labor force. With the economy growing somewhat above trend and employment growth remaining healthy, we expect the unemployment rate to decline a bit more before returning to its natural level.

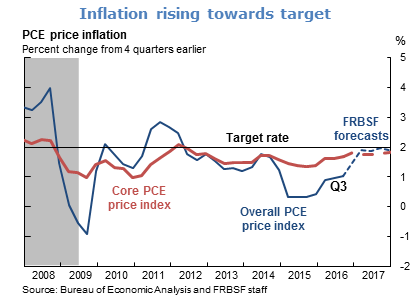

- Inflation has been increasing, but continues to run below the Federal Open Market Committee (FOMC)’s 2% target. In the 12 months through October, overall inflation, as measured by the change in the personal consumption expenditures (PCE) price index, was 1.4%, up from 1.2% in September. This is the highest reading since late 2014 and reflects the stabilization and rebound in energy prices. Core inflation, which strips out volatile movements in energy and food prices, rose 1.7% over the past 12 months through October, the same rate as reported in September. Average hourly earnings for private-sector workers continue to rise modestly, growing 2.5% in November compared with reported earnings of a year earlier. We expect that as the labor market tightens and the effects of past energy price declines dissipate, core and overall PCE inflation will rise gradually towards 2%.

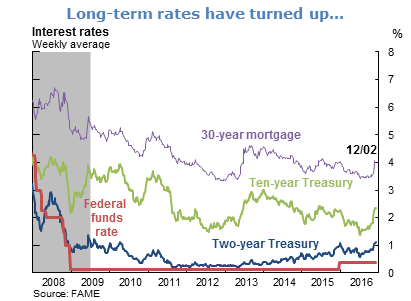

- Earlier this year, long-term U.S. Treasury yields fell to near historic lows, reflecting a combination of long-term and short-term factors. Over the long term, slower trend productivity and output growth in the United States and other advanced economies have reduced demand for investment. Aging populations and shrinking labor forces have also put downward pressure on output and have depressed investment demand. In addition, the so-called “global saving glut” in many emerging market economies has added to the supply of funds in financial markets. More saving and less investment have pushed down equilibrium interest rates. In the short term, heightened global uncertainty has increased demand for safe-haven assets, such as U.S. Treasuries. In addition, expansionary monetary policy in the United Sates and other advanced countries has pushed down rates.

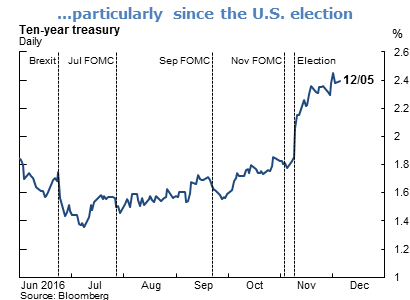

- In the past five months, long-term rates have risen as expectations of a federal funds rate hike have become stronger and the outcome of the U.S. election in early November has encouraged prospects of a more expansionary fiscal policy. The 10 year Treasury rate has risen roughly 100 basis points since July, with more than half of this change occurring in the last month.

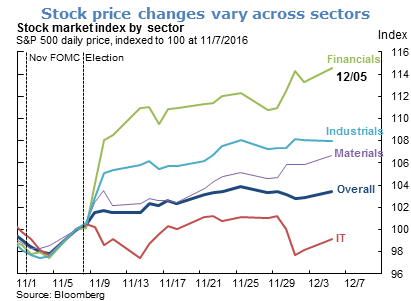

- Expectations of more fiscal stimulus have also affected the stock market, with the Standard & Poor’s (S&P) 500 index up over 4% since the elections. The changes in the stock market have varied across sectors. Firms in the industrial and materials sectors experienced relatively higher increases in stock prices presumably based on expected benefits from greater government infrastructure spending. Financial sector stocks also rose significantly due to expectations that higher interest rates and possibly less government regulation will boost earnings.

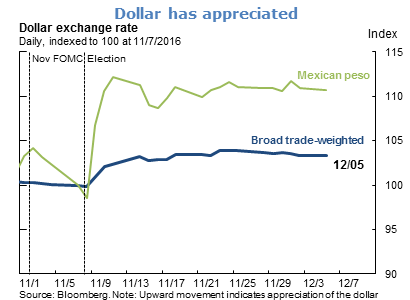

- Higher U.S. interest rates have also led to a stronger dollar. The dollar has appreciated against a broad basket of currencies by about 3% in the last month since the U.S. elections. The dollar appreciated even more against the Mexican peso because of concerns about possible changes in trade and immigration policies affecting Mexico’s bilateral relations with the United States.

- The financial market’s expected probability of a federal funds rate hike calculated from futures contracts fluctuates in response to economic data and events. Since the elections, expectations of a rate hike have increased markedly.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.