Bart Hobijn, senior research advisor at the Federal Reserve Bank of San Francisco, provides his views on current economic developments and the outlook.

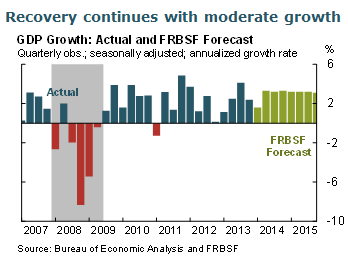

- Some data for January and February, such as auto sales and housing starts, came in softer than expected. It is likely that this weakness primarily reflects weather-related disruptions. These disruptions should have a temporary effect on the pace of the recovery, with a bounce back in growth likely when they dissipate. As a result, we recently lowered our forecast for GDP growth in the first quarter of 2014 and raised it slightly for the remainder of 2014. Our view of the underlying strength of the economy has not changed. We continue to see a moderately paced recovery that has generally gathered momentum since the start of 2013.

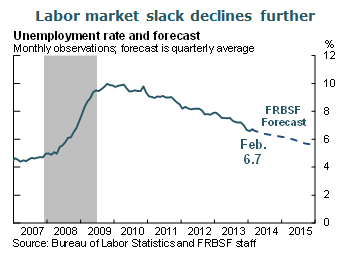

- The February labor market report showed a return to a solid pace of job growth. Though the unemployment rate ticked up in February, this appears to be only a brief interruption in the largely steady decline of the unemployment rate that we have seen since mid-2009.

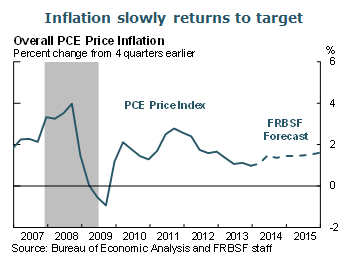

- We expect inflation to remain quite low over the next few years, returning only slowly to the FOMC’s 2% target. This view is guided by factors that affect the long-run inflation outlook as well as those that have more short-term effects.

- The long-run outlook for inflation is mainly driven by inflation expectations. As measured in household surveys, reported by business forecasters, and implied by pricing in financial markets, inflation expectations remain well-anchored. Consequently, our long-run inflation forecast is for a return to the 2% target consistent with general price stability.

- In the short run, however, other factors can cause persistent deviations of inflation from its target. One of the main factors contributing to the currently low inflation rate is that firms are not facing high cost pressures. Compensation costs, which make up the bulk of firms’ operating expenses, have been growing at approximately a 2% rate over the past two years.

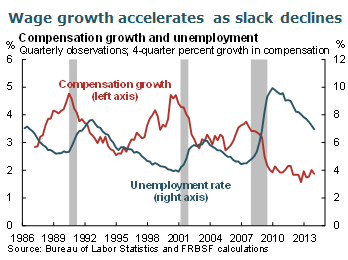

- It is common for wage growth to remain slow even after the unemployment rate declines. A similar pattern was evident in the wake of the 1990 and 2001 recessions. Once the unemployment rate declined enough to significantly reduce labor market slack, wage growth accelerated. Thus, as the unemployment rate declines, compensation growth will put increased upward pressure on firms’ costs.

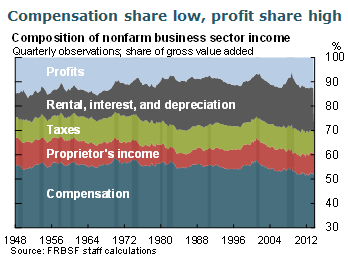

- The extent to which such upward cost pressures translate into price inflation will depend on how much firms absorb them into their profit margins or pass them on to higher prices for their products. Currently, compensation as a share of firms’ income is at a postwar low, while profit margins are high, implying plenty of room for businesses to absorb wage increases into profits. This suggests that rising compensation may not create substantial inflation pressures over the next few years.

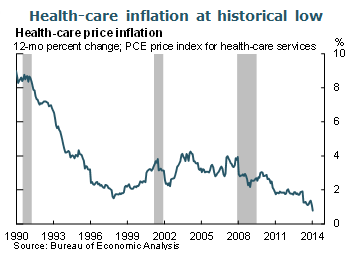

- Two other factors are currently contributing to the low inflation rate. The first is health-care price inflation. Health-care expenditures make up 17% of the goods basket that is used to calculate the Federal Open Market Committee’s preferred inflation measure, the personal consumption expenditures (PCE) price index. The expenditures are calculated in two parts. One is the direct out-of-pocket household costs for medical care. The other is the payments health insurance companies make on behalf of their customers. This is the same rate at which health-care providers are reimbursed for the services they provide. Reimbursement rates have been growing very slowly over the past year, causing the rate of health-care price inflation to fall to a 50-year low. Over the past year the rate of health-care price inflation fell more than 1 percentage point, thus contributing 0.2 percentage point to the slowdown in overall inflation.

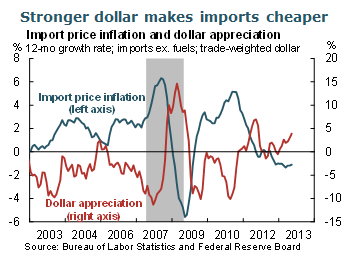

- The second factor contributing to low inflation is the decline in the price of imported goods and services over the past year. This decline is largely a response to the strengthening of the U.S. dollar. Such a decline in import prices tends to subdue inflation of goods with high import content, like clothing and consumer electronics.

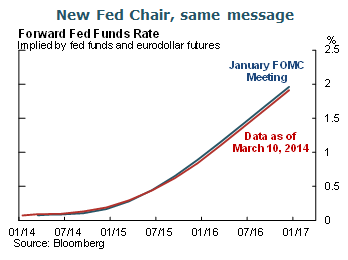

- Recent data and the change in the Chair of the FOMC have not significantly altered financial market

perceptions of future monetary policy. As of March 10, the path of the forward fed funds rate had

barely moved since the January 29 FOMC meeting.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.