Households are currently expecting inflation to run high in the short run but to remain muted over the more distant future. Given this divergence, what role do short-run and long-run household inflation expectations play in determining what workers expect for future wages? Data show that wage inflation is sensitive to movements in household short-run inflation expectations but not to those over longer horizons. This points to an upside risk for inflation, as workers negotiate higher wages that businesses could pass on to consumers by raising prices.

The U.S. labor market has rebounded strongly from the deep pandemic-related recession and is now very tight. Employment is back at pre-pandemic levels, job openings are surpassing the number of unemployed workers, and people are quitting jobs at high rates. Reflecting the difficulties businesses face in finding workers, wages have climbed substantially. Wages were growing about 3% annually before the pandemic, when the labor market was also tight; now, average hourly earnings are growing at roughly twice that rate, and even more in some sectors hit hardest during the pandemic, such as leisure and hospitality. Other measures, such as employment wage costs that control for worker shifts between occupations and industries, are up almost as much.

However, the substantial nominal wage gains have not been enough to compensate for the rise in inflation over the past year. The 12-month change in consumer price inflation has risen from 1.4% at the start of 2021 to more than 9% in June 2022. As a result, real wages, which adjust for the rising cost of living, have declined.

This increase in inflation was mostly unanticipated and expected by many to be temporary. Thus, it was likely not a major factor in wage negotiations until recently. However, if inflation remains very high, workers may expect it to persist and demand higher wages to match the rising cost of living (Lansing 2022). While the inflation rates that households expect over the longer run remain fairly stable, year-ahead inflation expectations have risen substantially since early 2021. In April 2022, year-ahead expected inflation was up to 5.4% before receding slightly to 5.2% in July. Therefore, future wage inflation depends in part on its sensitivity to short- and long-run inflation expectations.

In this Economic Letter, we show that year-ahead inflation expectations have a large impact on wage inflation, while long-term inflation expectations have essentially no influence. Given the large increase in short-term inflation expectations in the past year, our results point to an important upside risk to inflation, as workers demand higher wages that businesses could pass on to consumers by raising prices. By reducing demand, ongoing monetary policy tightening will help reduce the probability that this risk materializes. As such, the stability of long-run inflation expectations is a sign that households have confidence that the Federal Reserve will achieve low inflation over time.

The recent evolution of inflation expectations

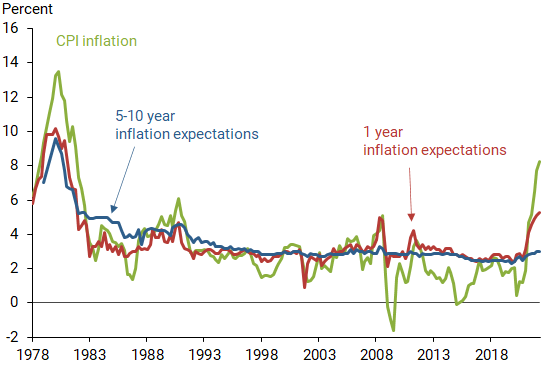

Every month the University of Michigan conducts a survey of consumers. As part of this survey, a representative group of households are asked about their expectations for future inflation, either in the short run over the next year, or over the longer run, the next five to ten years. Figure 1 shows that household one-year-ahead inflation expectations have risen dramatically over the past year, in line with higher actual inflation. Historically, household short-run inflation expectations are highly sensitive to recent changes in inflation: the two series have a correlation of 0.91 between 1980 and June 2022. In assessing what inflation is likely to be in the year ahead, households are particularly influenced by recent changes in gas, food, and other commodity prices (Glick et al. 2021). Thus, it is not unusual to see spikes in household inflation expectations following fluctuations in those prices, as in 2008 and 2011.

Figure 1

Price inflation and inflation expectations

Note: Consumer price index (CPI) inflation measured as four-quarter percent change.

Source: BEA and University of Michigan; some missing 5-10 year expectations for the 1980s use interpolations from adjacent quarters or FRB Philadelphia’s Livingston Survey.

In contrast to the substantial rise in household short-run inflation expectations, Figure 1 shows that households continue to expect only moderate inflation over the longer run, expecting prices to rise roughly 3% on average. This may reflect a perception that the recent inflation increase is driven by temporary factors, for instance, the effects of fiscal support or supply-chain disruptions, which will wane over time (Barnichon et al. 2021, Jordà et al. 2022). Alternatively, they may expect the Federal Reserve to raise interest rates sufficiently to reduce inflation over time, even if underlying shocks prove persistent.

The considerable rise in short-run inflation expectations may lead workers to demand higher wages to compensate for the anticipated rise in the cost of living. However, businesses may be reluctant to give large pay increases if price pressures are expected to be temporary, particularly if they are unable to pass higher costs on to consumers. Thus, it is unclear how much wage growth responds to changes in short- or long-run inflation expectations.

Wage growth determinants

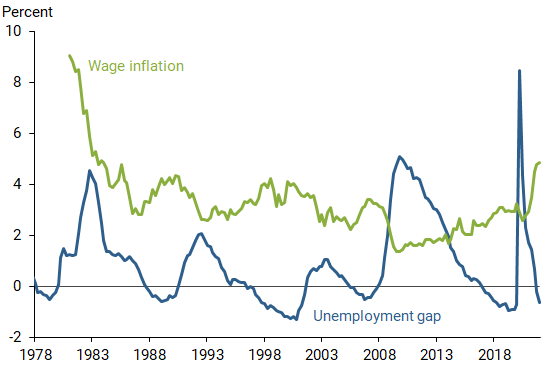

To examine the effects of short- and long-run inflation expectations on wage inflation, we estimate a wage Phillips curve, an empirical relationship between overall wage inflation and its determinants. One important factor driving fluctuations in wage inflation is the business cycle and the strength of the labor market, as captured by the unemployment gap. The unemployment gap measures the difference between the unemployment rate and a measure of maximum employment from the Congressional Budget Office. A negative unemployment gap thus reflects a tight labor market. Figure 2 shows that, historically, wage inflation has moved inversely with the unemployment gap. When the labor market is strong and the unemployment gap is negative, nominal wages tend to rise. In contrast, when the labor market is weak and the unemployment gap is positive, nominal wages tend to fall.

Figure 2

Unemployment gap and wage inflation

Note: Wage inflation measured as four-quarter percent change in employment cost index.

In addition to the unemployment gap, our wage Phillips curve includes household short-run and long-run inflation expectations from the University of Michigan, and lagged core price inflation, which abstracts from volatile food and energy price inflation, to capture the possibility that workers and firms are directly influenced by previous price inflation when agreeing on wages. We use core inflation because it is more persistent than headline inflation and thus more likely to influence wages. Other work suggests that household inflation expectations may also capture the effects of lagged oil and other noncore inflation components (Coibion et al. 2018 and Glick et al. 2021). We also include the trend growth in labor productivity from the Bureau of Economic Analysis (BEA). Over time, higher labor productivity growth should boost wage growth, with the strength of the relationship depending on such factors as workers’ and firms’ bargaining power. To rule out the possibility that inflation leads to ever-rising, “explosive” increases in wage growth over time, we assume the total effects of lagged and expected inflation equal wage inflation over the long run (see, for instance, Hooper, Mishkin, and Sufi 2020).

To estimate this wage Phillips curve, we use quarterly data from the second quarter of 1980 to the first quarter of 2022. We measure wages using the wages and salaries component of the employment cost index compiled by the BEA, with data beginning in the first quarter of 1980. This measure accounts for changes in the composition of the workforce, which could impact wage growth separately from the wage Phillips curve. Inflation rates in wages and core prices are measured as (log) changes over each quarter at an annual rate.

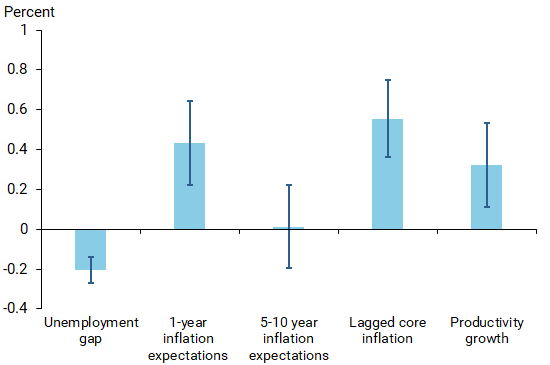

Figure 3 reports the estimated coefficients for the wage Phillips curve components, where the height of the bars indicates the estimated percent change of wage inflation in response to a 1 percentage point change in each component. The figure also reports the 95% confidence bands around each estimate. The figure shows that wage inflation is significantly related to labor market tightness, as Figure 2 implies. A tighter labor market, represented by a negative unemployment gap, is associated with higher wage inflation. The results also confirm that greater productivity growth is accompanied by higher wages.

Figure 3

Effects on wage inflation of 1% change in variables

Note: Dark blue bands indicate 95% confidence intervals.

Most importantly, Figure 3 also shows that short-run household inflation expectations are a key determinant of wage inflation, along with the unemployment gap, lagged core price inflation, and trend productivity growth. In contrast, long-run household inflation expectations have no statistically significant effects on wage inflation, as reflected by the fact that the confidence bands encompass the possibility that these estimated effects are zero. The influence of short-term inflation expectations on wage inflation is similar to their role for price inflation, as documented in Coibion, Gorodnichenko, and Kamdar (2018).

Our general results are unaffected if we use alternative measures of variables in our analysis, such as measuring wages with average hourly earnings or measuring slack with the vacancy-to-employment ratio, or if we add other possible explanatory variables such as oil or noncore price inflation. Removing the assumption that wage inflation is tied to past and expected inflation over the long run also does not affect our main conclusion, that wages are sensitive to short-run but not to long-run inflation expectations.

Inflation risk

According to these results, the recent rise in household year-ahead inflation expectations could lead to substantially higher wage inflation in the short run. Focusing on this channel alone, our estimated wage Phillips curve suggests current household one-year-ahead expectations could add nearly 2.3 percentage points to wage inflation. To the extent that companies raise prices and pass on the higher labor cost to consumers, our results point to an important upside risk to inflation. To mitigate this cost increase, companies could decide to automate or offshore some jobs, although higher tariffs and supply-chain challenges make offshoring more costly than in the past.

On the other hand, the decline in unionization over the past 50 years and the disappearance of automatic cost-of-living adjustments in long-term wage contracts make it less likely that short-run inflation expectations will persistently boost wage inflation. Similarly, many firms have relied on one-time bonuses to attract and retain workers instead of permanently raising wages. More broadly, monetary policymakers have the tools to reduce this inflation risk by raising interest rates to lean on overall demand. The fact that changes in long-run inflation expectations have been muted over the past year suggests that households have confidence that the Federal Reserve will restrict monetary policy sufficiently to bring about low inflation over the medium run and avoid a price-wage inflationary spiral.

Conclusion

Inflation is running at a 40-year high, and year-ahead household inflation expectations have risen substantially, although households continue to expect relatively muted inflation over the longer run. Given this divergence in expectations, this Letter assessed the role of short-run and long-run household inflation expectations as a determinant of wage inflation. We showed that movements in short-run household inflation expectations have a significant impact on wage inflation. In contrast, wage inflation does not react to changes in long-run household inflation expectations. Therefore, the increase in short-run expectations since last spring point to an important upside risk to inflation, as workers negotiate higher wages that businesses could pass on to consumers in the form of higher prices. By reducing overall demand, the ongoing monetary policy tightening will help reduce the probability that this risk materializes.

Reuven Glick is a group vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Sylvain Leduc is executive vice president of the Economic Research Department of the Federal Reserve Bank of San Francisco.

Mollie Pepper is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Barnichon, Regis, Luiz E. Oliveira, and Adam H. Shapiro. 2021. “Is the American Rescue Plan Taking Us Back to the ’60s?” FRBSF Economic Letter 2021-27 (October 18).

Coibion, Olivier, Yuriy Gorodnichenko, and Rupal Kamdar. 2018. “The Formation of Expectations, Inflation, and the Phillips Curve.” Journal of Economic Literature 56(4), pp. 1,447–1,491.

Glick, Reuven, Noah Kouchekinia, Sylvain Leduc, and Zheng Liu. 2021 “Do Households Expect Inflation When Commodities Surge?” FRBSF Economic Letter 2021-19 (July 12).

Hooper, Peter, Frederic Mishkin, and Amir Sufi. 2020. “Prospects for Inflation in a High Pressure Economy: Is the Phillips Curve Dead or Is It Just Hibernating?” Research in Economics 74(1), pp. 26–62.

Jordà, Òscar, Celeste Liu, Fernanda Nechio, and Fabián Rivera-Reyes. 2022. “Why Is U.S. Inflation Higher than in Other Countries?” FRBSF Economic Letter 2022-07 (March 28).

Lansing, Kevin J. 2022. “Untangling Persistent versus Transitory Shocks to Inflation.” FRBSF Economic Letter 2022-13 (May 23).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org