The jobless unemployment rate is a reliable predictor of recessions, almost always showing a turning point shortly before recessions but not at other times. Its success in predicting recessions is on par with the better-known slope of the yield curve but at a shorter horizon. Hence, it performs better for predicting recessions in the near term. Currently, this data and related series analyzed using the same method are not signaling that a recession is imminent, although that may change in coming months.

The U.S. economy undergoes repeated business cycles, expanding gradually during booms and contracting sharply during recessions. Since business cycles affect both financial markets and the real economy, forecasting if and when the economy will head into a recession is of interest to financial market participants and policymakers alike. A variety of different models try to predict these cycles using indicators from financial markets, consumer sentiment measures, and the real side of the economy (see, for example, Kiley 2022).

This Economic Letter discusses how the jobless unemployment rate can be turned into a predictor for recessions. The resulting predictions are surprisingly accurate, on par with those derived from the more commonly used Treasury yield curve. The Letter further argues that the same methodology used for the jobless unemployment rate can also be applied to other macroeconomic time series to forecast recessions.

The unemployment rate and the business cycle

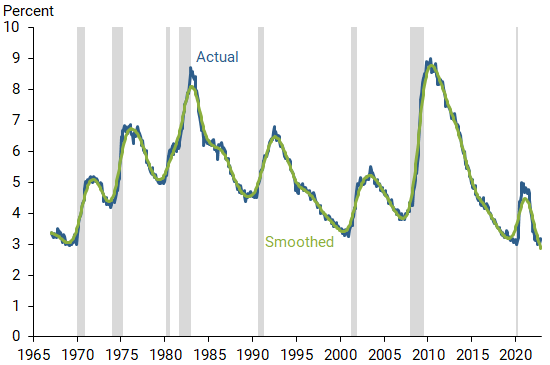

The smoothed jobless unemployment rate exhibits a predictable pattern throughout the business cycle, typically rising sharply in recessions and gradually declining during expansions. Figure 1 shows the jobless unemployment rate, defined as the fraction of people who are unemployed—adjusted for workers who lost jobs and are on temporary layoffs—in the labor force over time (blue line). The underlying historical time series from the Bureau of Labor Statistics are publicly available on the St. Louis Fed’s FRED database starting in January 1967. The figure also shows an estimate of the historical cyclical trend in the series obtained with the benefit of hindsight. This estimated historical trend is a smoothed version of the time series that averages over both past and future monthly values (green line). The jobless unemployment rate primarily differs from the conventional unemployment rate in that it exhibits a much smaller spike during the COVID-19 recession when many workers were furloughed.

Figure 1

Actual and smoothed jobless unemployment rate

Source: Bureau of Labor Statistics, FRED, and author’s calculations.

Note: Gray shading indicates NBER recession dates.

The figure shows a stable pattern emerging over time. The smoothed jobless unemployment rate bottomed out and turned before every recession except in 1982. Furthermore, the estimated historical trend never turned at any other part of the business cycle.

These consistent patterns around recessions resemble evidence from the Treasury yield curve. Every recession since the mid-1950s was preceded by an inversion of the yield curve (Bauer and Mertens 2018a), when long-term yields fell below short-term yields. And there was only one yield curve inversion in the mid-1960s that was not followed by a recession within two years. The slope of the yield curve is thus a very reliable predictor for recessions (Bauer and Mertens 2018b). With the yield curve currently inverted, several market participants and commentators have warned of recession risks.

The smoothed jobless unemployment rate declined during about two-thirds of the months in the sample starting in 1967 and increased during one-third. This compares to the National Bureau of Economic Research classifying 87% of the months as expansions and 13% as contractions, that is, recession months. At the same time, months when the jobless unemployment rate increased and decreased have been heavily clustered. Typically, the jobless rate falls during expansions, turns before a recession, and then rises during the downturn.

Consequently, if the low points can be identified based on the latest data, recessions become more predictable. These low points are turning points in the smoothed jobless unemployment rate that occur when (1) the series has bottomed out, but (2) its rate of change is rising. Applying the first of these two conditions would identify both highs and lows in the series. With the second condition included, only the low points are identified. Mathematically, the first condition corresponds to the first derivative being zero in the time series while the second condition corresponds to the second derivative being positive.

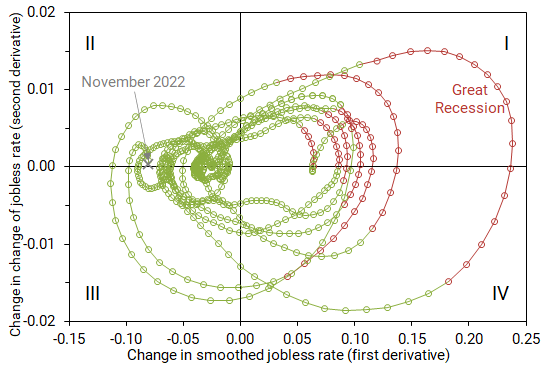

To visualize this procedure, Figure 2 plots the change in the smoothed jobless unemployment rate (first derivative) on the horizontal axis and the change in the change (second derivative) on the vertical axis. Recession months are depicted as red dots and expansion months as green dots.

Figure 2

Clockwise movements of jobless unemployment rate

Source: Bureau of Labor Statistics, FRED, and author’s calculations.

Note: First derivative measures the change in the smoothed jobless rate; second derivative measures the change in the change of the smoothed jobless rate.

Charted this way, the time series shows the mostly clockwise movements around the origin where the zero lines cross. To describe the movement, I turn the chart into a “recession clock” using estimates of the historical cyclical trend. Turning points in the time series occur when the change is zero and increasing, that is, when the curve crosses 12 o’clock, moving from the second quadrant into the first quadrant, labeled in Roman numerals in the figure. Notably, recessions start a few months later, as indicated by a few expansion months (green dots) after the turning point moves into the first quadrant.

This recession prediction closely relates to the “Sahm rule” (Sahm 2019). According to this rule, a recession occurs when the three-month moving average of the overall unemployment rate has risen at least half a percentage point above its minimum over the previous 12 months. The main difference is that the recession clock developed here is an advance predictor of recessions, whereas the Sahm rule typically indicates a recession after it has already started.

Predictions using the recession clock

The analysis above estimates the underlying historical trend by averaging past and future data around each point in time. Turning these estimates into real-time recession predictors requires a purely backward-looking methodology.

For this analysis, I’ll first turn to an indicator that predicts a recession when the time series crosses from the left-side quadrants of Figure 2, which indicate a negative slope, into the first quadrant between 12:00 and 3:00. For example, the real-time recession clock moved from 8:03 to 12:19 in June 2007. This change in the recession clock occurred about half a year before January 2008, which marked the official start of the Great Recession.

To shed light on the accuracy of the forecast for predicting recessions, I use a simple procedure to compute the rate of false positives—the incidence of incorrectly predicted recessions relative to all expansion months—and false negatives—the fraction of actual recession months that were not predicted. This provides insights into both the prediction accuracy and the optimal forecast horizon (Berge and Jordà 2011).

After trading off false positives and false negatives, I find that the jobless unemployment rate is most successful in predicting future recessions at a horizon of eight months. The jobless unemployment rate is thus a shorter-term predictor compared with the slope of the yield curve, measured as the difference between yields on 10-year and 1-year Treasury securities, which has an optimal prediction horizon of 13 months (Bauer and Mertens 2018a). At their respective horizons, the forecast accuracy is very similar, although the yield curve has a slight edge.

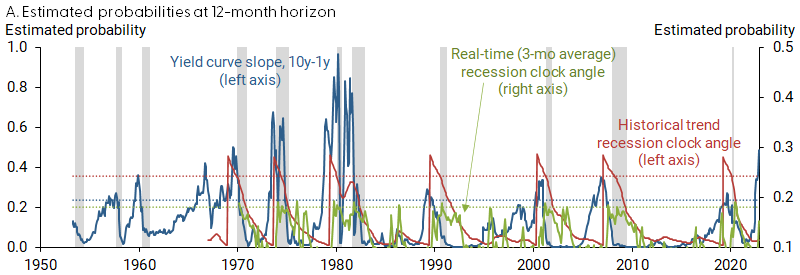

I use a second statistical analysis based on a probit model that turns a recession indicator into a probability. The predictor is a three-month moving average of the angle of the dial on the real-time recession clock. Panel A of Figure 3 shows the estimated probabilities of being in a recession 12 months ahead for estimates of the recession clock in real time and based on historical trends and compares them to estimates derived from the yield curve.

Figure 3

Estimated recession probabilities using yield curve and recession clock

Source: Bureau of Labor Statistics, FRED, and author’s calculations.

Note: Dotted lines indicate prediction thresholds for lines of same color. Gray shading indicates NBER recession dates.

Translating these estimates into recession predictions requires specifying a threshold level above which the estimates can be interpreted as signaling a recession at the end of the forecast horizon. Appropriate threshold levels are defined by a zero slope of the yield curve and a recession clock angle of 1:30, leading to thresholds of 0.23 for the yield curve and 0.36 and 0.18 for the historical cyclical trends and real-time recession clocks, respectively.

The estimated probabilities for all three indicators increase around the start of recessions, shown by the gray shaded bars. Compared with the slope of the yield curve, the real-time recession probability based on the jobless unemployment rate is substantially less reliable at the 12-month horizon. The slope of the yield curve performs much better with this longer lead time.

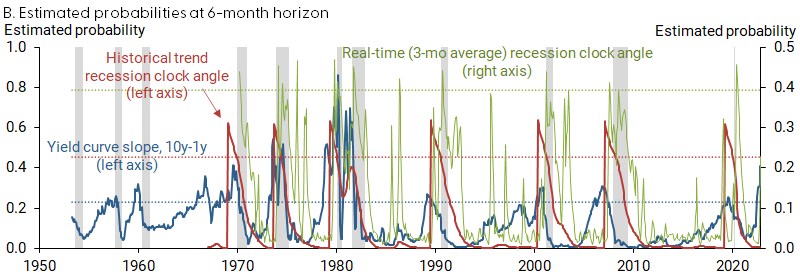

At the six-month horizon, however, both the historical trends and real-time estimates based on the jobless unemployment rate outperform the slope of the yield curve, as shown in panel B of Figure 3.

Based on current data, recession probabilities are elevated according to the slope of the yield curve where they are 25 percentage points above the threshold for recession prediction at a 12-month horizon. For the jobless unemployment rate, they currently stand 16 percentage points below the threshold at a 6-month horizon and are thus still relatively low. While the most recent reading of the recession clock has crossed 12 o’clock into the first quadrant, the three-month moving average still shows that it hasn’t done so on a sustained basis. This assessment could change quickly if the unemployment rate ticks up in coming months.

The Federal Open Market Committee’s Summary of Economic Projections (SEP) from December predicts that the unemployment rate will likely rise in 2023. Such an increase would trigger a recession prediction based on the unemployment rate. Under this view, low unemployment can lead to a heightened probability of recession when the unemployment rate is expected to rise. In this sense, the prediction based on the recession clock can differ from the Sahm rule, which would not indicate a recession if the unemployment rate were to rise gradually.

Other macroeconomic time series

Similar to the jobless unemployment rate, some other macroeconomic time series that exhibit a strong cyclical pattern may also have predictive power for recessions. Those series include the overall unemployment rate, the vacancy-to-unemployment ratio, initial unemployment insurance (UI) claims, and housing starts. The same methodology I use to find turning points in the jobless unemployment rate can also deliver recession predictors based on these other macroeconomic time series.

While the overall unemployment rate produces very similar recession predictions to those from the jobless unemployment rate, the other time series lead to significantly less-reliable predictions. However, the three alternative time series to unemployment-based measures can lead to earlier predictions. While the best prediction horizon is eight months for the jobless unemployment rate, it is 12 months for the vacancy-to-unemployment ratio and housing starts and 16 months for UI claims.

These combined results suggest that an accumulation of evidence is the best predictor of recessions. When initial UI claims have been rising, the slope of the yield curve is inverted, and housing starts and the vacancy-to-unemployment ratio are falling on a sustained basis, a situation emerges that has historically been associated with a runup to a recession.

Currently, none of these predictors indicate an upcoming recession over the next two quarters. However, the underlying trend in these macroeconomic time series has started to turn and the predictions might change in the coming months.

Conclusion

This Economic Letter discusses recession predictions based on macroeconomic time series, particularly the jobless unemployment rate. This predictor is almost as accurate as the slope of the yield curve but is more accurate at shorter horizons. The jobless rate does not currently signal an impending recession, nor do other macroeconomic time series analyzed using the same methodology. In general, however, examining these series suggests that the business cycle is at a maturing stage when expansions typically come to an end.

Thomas M. Mertens is a vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Bauer, Michael D., and Thomas M. Mertens.2018a. “Economic Forecasts with the Yield Curve.” FRBSF Economic Letter 2018-07 (March 5).

Bauer, Michael D., and Thomas M. Mertens. 2018b. “Information in the Yield Curve about Future Recessions.” FRBSF Economic Letter 2018-20 (August 27).

Berge, Travis J., and Òscar Jordà. 2011. “Evaluating the Classification of Economic Activity into Recessions and Expansions.” American Economic Journal: Macroeconomics 3(2), pp. 246–277.

Kiley, Michael T. 2022. “Financial and Macroeconomic Indicators of Recession Risk.” FEDS Notes, Federal Reserve Board of Governors, June 21.

Sahm, Claudia. 2019. “Direct Stimulus Payments to Individuals.” In Recession Ready: Fiscal Policies to Stabilize the American Economy, report produced by The Hamilton Project, eds. Heather Boushey, Ryan Nunn, and Jay Shambaugh, pp. 67–92.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org