Fernanda Nechio, research advisor at the Federal Reserve Bank of San Francisco, stated her views on the current economy and the outlook as of February 8, 2018.

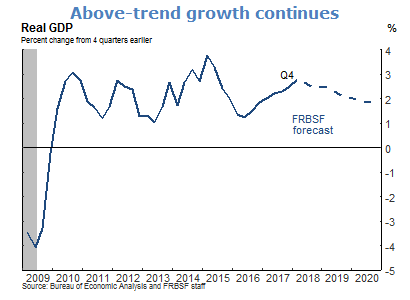

- Based on the advance estimate of the Bureau of Economic Analysis, real GDP expanded at an annual rate of 2.6 percent for the fourth quarter of 2017 and 2.5 percent for the year overall. The bulk of the strength in real GDP growth can be attributed to robust consumer spending, which in turn reflects household wage gains, increased equity prices, and supportive financial conditions. As monetary policy continues to normalize over the next two to three years, we expect growth gradually to fall back to our trend growth estimate of about 1.8%.

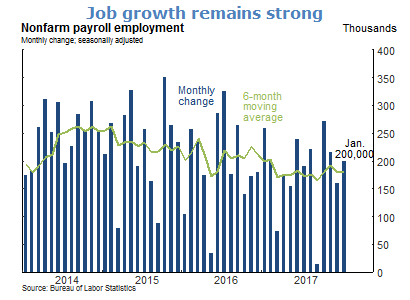

- Recent employment gains remain solid. Nonfarm payroll employment in January rose by 200,000 jobs. During 2017, payroll gains have averaged around 181,000 jobs per month.

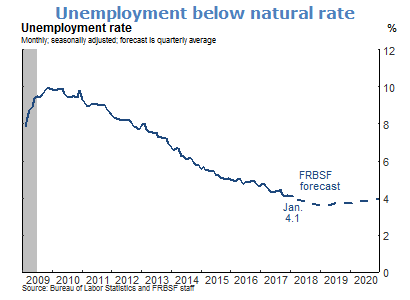

- The unemployment rate remained at 4.1% in January, unchanged since October. We expect this rate to fall below 4% in 2018 before gradually returning to our estimate for its natural level at 4.75%.

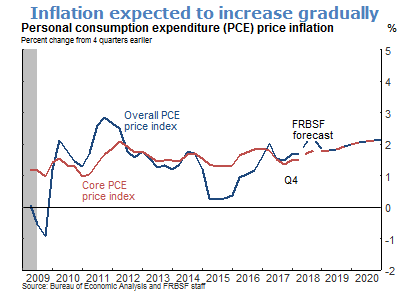

- Inflation continues to remain below the Federal Reserve’s 2% target. Overall inflation in the twelve months through December, as measured by the price index for personal consumption expenditures was 1.7%. Core inflation, which excludes volatile food and energy prices, rose 1.5% in the twelve months through December. Given the strong labor market conditions, we expect overall and core consumer price inflation to rise gradually and reach our 2% target over the next couple of years.

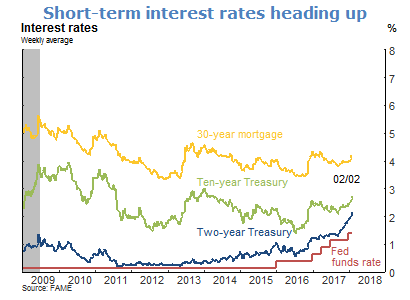

- Interest rates are continuing to increase with the gradual removal of monetary policy accommodation. At its January meeting, the FOMC maintained the target range for the federal funds target at 1.25% to 1.5%.

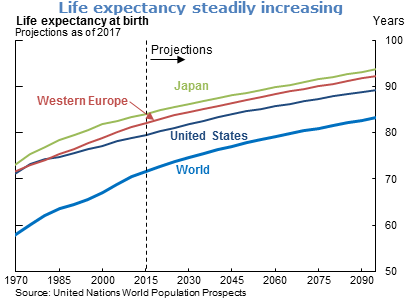

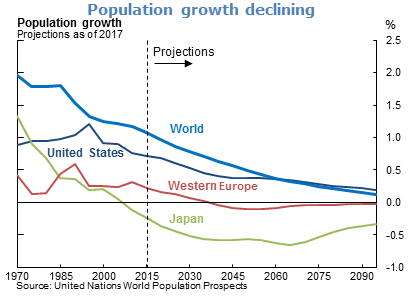

- The developed world is undergoing a dramatic demographic transition. In most advanced economies, actual and expected longevity have increased steadily, while the median retirement age has changed little, leading to longer retirement periods. Meanwhile, population growth rates are declining and in some cases, even becoming negative.

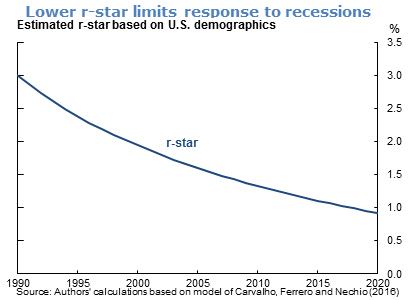

- Changing demographics can affect the natural real rate of interest, r-star; the inflation-adjusted interest rate that is consistent with steady inflation at the Fed’s target and the economy growing at its potential. Demographic trends affect the equilibrium rate by changing incentives to save and consume. Lengthier retirement periods may raise some households’ desire to save rather than consume, lowering r-star. At the same time, declining population growth increases the share of older households in the economy, who generally have higher marginal propensities to consume, raising consumption and r-star. As population growth declines, it could also reduce real GDP growth and productivity, thereby putting downward pressure on r-star.

- In the United States, these demographic changes have already put significant downward pressure on interest rates between 1990 and 2017. As demographic movements tend to be long-lasting, the effects on interest rates may be ongoing. A lower equilibrium rate has the potential to limit the scope for the Federal Reserve to cut interest rates in response to future recessionary shocks.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.