The demographics of aging have long been studied as a key driver of investment behavior in capital markets, as changes in life stage alter investor preferences. Asia is home to countries with a diverse range of demographic profiles, with several rapidly aging countries like Japan, Korea, and China, and younger populations in India and Indonesia. Building upon other research into the relationship between demographics and capital markets, this post considers how aging may impact the region.

Asia’s Work Force is Peaking, but the Investor Base is Still Growing

Economists often examine the age demographics of a country for insight into future performance. For countries with a young population, economic growth may benefit from the so-called “demographic dividend.” A younger population creates a larger base of workers who, in addition to providing their labor, also generate demand for goods and services and pay taxes—all contributors to economic activity. When a large cohort of workers ages and begins to retire, the workforce shrinks, and economists mark the end of the demographic dividend.

The aging of a workforce creates challenges for economic growth. Indeed, the IMF estimates that the aging population will subtract up to one percentage point from annual GDP growth in Japan over the next three decades. Still, transition out of the demographic dividend period can boost financial markets at intermediate stages. Younger workers tend to lack excess savings useful for investing in capital markets, as their incomes are lower and their need to accumulate other long-term assets—from education to housing—defrays investment. Conversely, people begin to “de-save” upon retirement, consuming their life savings, in whatever form, including selling assets like stocks.

The sweet spot age for investment comes in between. Economic theory on lifecycle saving and investment behavior indicates that people save the most when reaching middle age, assuming they have adequate income. Modern portfolio theory also recommends that middle-aged individuals allocate a large chunk of their savings in equity investment. As a result, economies with a rising share of middle-aged workers may see a potential boost to capital markets. Workers at middle-age—typically defined as beginning at 35 or 40 years old—form the core equity market investor base in developed countries.

In the Investment Sweet Spot?

An examination of the ratio of middle- to young-aged populations (M/Y ratio) indicates that a number of Asian countries with the region’s largest stock markets (Table 1) might be in a favorable demographic position over the next decade.

Table 1

Asia’s Largest Stock Markets

| Country | Market Cap (US$ trillion) |

|---|---|

| China | 7.64 |

| Japan | 6.33 |

| Hong Kong | 5.70 |

| ASEAN-5 | 2.37 |

| India | 2.29 |

| South Korea | 1.75 |

| Taiwan | 1.27 |

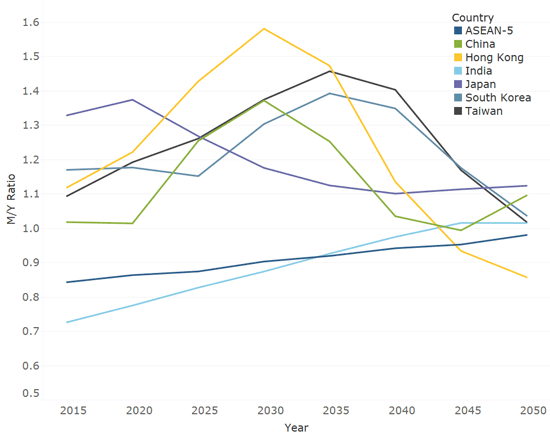

Based on United Nations population data and projections of future growth, China, Japan, Hong Kong, India, South Korea, Taiwan, and the ASEAN-51 countries are all in the midst of an upward swing in the size of their middle-aged population that forms the core investor base. In each country, the M/Y ratio—calculated using cohorts of 35-49 and 20-34 years old—is trending upwards (Figure 1).2

Asia Grows Up (Middle- to Young-aged Populations)

Estimates based on medium-variant forecast of fertility.

For Japan, this trend will be short lived as the current cohort of middle-aged Japanese is relatively large, a relic of a baby boom during Japan’s high growth in the 1970s. Elsewhere in northeast Asia, China and South Korea will see their M/Y ratio continue to climb over the next decade. Hong Kong, home to Asia’s 3rd largest stock market capitalization, is expected to see a peak above 1.6. In contrast, the ratio for the United States peaked at only 1.1 in the year 2000. Proponents of the explanatory power of demographics in capital markets forecasting have long argued that the late 1990s US stock market rally, popularly understood as a technology-driven boom, was boosted by the growth of the country’s middle-aged workforce. If northeast Asia follows this trend, the region can expect a strong demographic tailwind for capital markets over the next decade. The region’s high saving rates will likely add additional momentum.

Elsewhere in Asia, young populations mean the demographics may not yet be ideal for capital market accumulation. India and the ASEAN-5 are both projected to have more young than middle-aged workers for the next three decades. This is not necessarily a negative, as the demographic dividend can boost economic growth, but it may mean less domestic demand for securities.

Greying May Hurt Developed Asian Markets

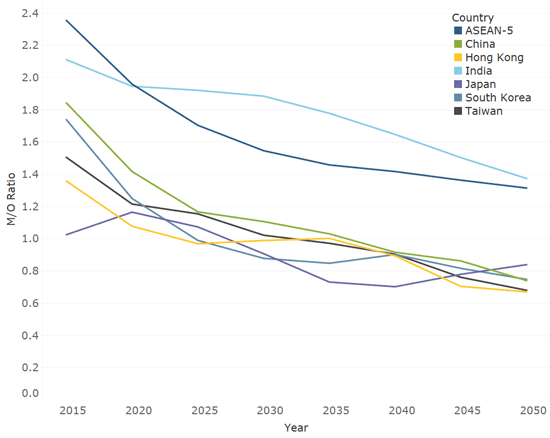

Another popular demographic indicator used to forecast capital market performance is the ratio of middle- and old-aged populations (i.e. the core working age population and the retired). Some researchers argue the middle-aged to old (M/O) ratio is more likely to predict changes in behavior given that it captures the two life stages where buying and selling behaviors are most clearly defined (as opposed to young adulthood, when many people simply do not invest). Over the second half of the 20th century, the M/O ratio—defined by SF Fed Research staff as the ratio between cohorts of 40-49 and 60-69 years old—moved in near lockstep with the S&P 500. While this relationship appears to have broken down in the wake of unconventional monetary policy that followed the global financial crisis, it still may be instructive to consider how Asian countries fare according to this indicator.

Perhaps unsurprisingly given the general aging of the world population—driven by rapid improvements in areas like nutrition, public health, and medical care—all Asian countries are forecasted to see a drop in their M/O ratios as more and more people live longer and longer (Figure 2). In fact, save for Japan, which will see a slight increase over the next decade, all countries in the sample will see a continuous decline in the M/O ratio moving forward.

Asia Greys

While this aging pattern implies a counteracting demographic force to the region’s growing middle-aged work force, it may be more relevant to countries with developed capital markets like Japan, South Korea, Hong Kong, and Taiwan, where securities have played a larger role in modern retirement planning. Japan’s Government Pension Investment Fund, for example, holds $1.4 trillion in securities, making it the largest pension fund in the world. By comparison China’s National Social Security Fund, founded in 2000, held roughly RMB 723 billion ($111 billion) in public equity investments as of its latest end-2016 reporting.3 For emerging Asian economies like China, India, and Indonesia, a growing base of middle-aged workers investing in the stock market may be a stronger force than retiring workers who have limited equity investment.

Monitoring the Impact of Asia’s Middle-aged

There are clear limitations to the broad use of age demographics to predict capital market behavior in a range of economies as diverse as Asia’s. Differing stages of economic and financial sector development, a diverse mix of demographic profiles, and distinctions in retirement savings systems offer a number of potential confounding factors. Further, some researchers debate whether current market prices already incorporate the potential impact of future demographic changes, as would be predicted by the efficient markets hypothesis. Even so, it is worth monitoring the impact of the broad increase in Asia’s population of middle-aged workers, which could be an important factor for the region’s capital markets in the coming decade.

1. Indonesia, the Philippines, Malaysia, Singapore, and Thailand.

2. Some studies choose to calculate the MY ratio using cohorts of 20-39 and 40-59 years old.

3. Original source in Chinese.

The views expressed here do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.