At its heart, historic preservation is about recognizing and valuing what was created

in the past. It offers a lens for recognizing the value of neighborhoods and telling

the stories of the people who have shaped and continue to shape them. This

chapter articulates the case for a community-oriented preservation model that

supports long-time residents, creates pathways for newcomers, and strengthens neighborhoods

for all. The idea that there is economic, social, and environmental value worth preserving

in existing buildings, neighborhoods, and communities is an essential theme in stabilizing

middle neighborhoods. Stabilization is often discussed in theoretical terms, but it has very

practical effects on neighborhood real estate values, as the other chapters in this book attest.

Reinvesting in buildings can boost property value. When the process of reinvestment includes

and honors local communities and their ongoing stories—their heritage—preservation can be a

powerful tool for significant and sustainable change in neighborhood dynamics.

Preservation offers an approach to and set of strategies for thoughtfully managing change

in areas with high development or demolition pressures. The most obvious tools for managing

change are zoning and other local regulations, particularly in designated historic districts,

and financial tools such as historic tax credits and tax abatements.1

However, this chapter

focuses on strategies and tools that are not tied to historic designation and thus are more

broadly applicable in middle neighborhoods and elsewhere. These tools help to stabilize and

strengthen real estate markets in older neighborhoods and, in a related benefit, provide an

avenue for active community stewardship of places. As will be discussed below, preserving

older housing in middle neighborhoods serves sustainability, health, and social equity objectives

in addition to market stabilization benefits.

America’s legacy cities are uniquely positioned to innovate across a slate of policy areas,

including preservation, as the immediacy of physical, economic, and social challenges

demands new thinking on complex challenges. The first section of this chapter describes how a growing network of actors has redefined preservation in legacy cities. The second section

explores the multiple value propositions that preservation can bring to holistic neighborhood

stabilization and preservation. The chapter concludes with case studies of three Ohio

coalitions that are implementing effective preservation strategies in stabilizing middle neighborhoods,

as well as a discussion of ways forward.

Redefining Preservation

To be clear, we advocate for a type of preservation that is not Thomas Jefferson’s Monticello,

New York’s Grand Central Terminal, or the gracious Lower Peninsula in Charleston. It

is about neighborhoods with buildings where siding has been patched and windows replaced,

where vacant lots and buildings sit between occupied homes. It is about people, their stories,

and the collective heritage of neighbors and families. In short, it is about individual and

community investment rooted in a passion for a specific place. This approach represents

a pragmatic preservation ethos: one that recognizes that not every building can or should

be saved and embraces instead a holistic view that prioritizes actions—from mothballing to

demolition to rehabilitation—based on realistic assessments of neighborhood conditions and

likely short- to medium-term changes.

The earliest preservation advocates in the United States saw their work in the context of

community. Beginning in 1853 with a campaign to save George Washington’s home, the

fledgling movement looked to the past to shape a more virtuous future. Subsequent efforts

have often been motivated by a “civic patriotism” that uses the tangible past to define a

common identity. When New Yorkers rallied to try to save Penn Station in 1963, they were

in part reacting to larger autocratic decisions around demolition, freeways, and the shape of

their city. Although the building was lost, it catalyzed a broad-based preservation movement

that saw the urban landscape as a more democratic endeavor.

Too often, preservation has been perceived as an elite discipline dominated by monuments

and wealthy, typically white, neighborhoods. The situation is more complex than

that, of course, but it holds truth. The stories most often recorded and celebrated are those of

privileged groups, and the buildings that typically receive attention are grand buildings built

for and occupied by the same groups. Even as preservationists and community advocates

have expanded the conception of multilayered, multicultural histories, the historic designation

required for powerful historic tax credits and other incentives has historic integrity as a

core requirement. That limits eligibility to buildings or neighborhoods that remain largely

unchanged, a quality virtually impossible in long-disinvested low-income neighborhoods

and communities of color that have faced—and are still facing—pervasive structural discrimination

and underinvestment. Although not all middle neighborhoods share this particular

history, most have faced decades of struggle.

It can be argued that the current iteration of preservation has goals similar to the earliest

movements, but with equity and sustainability as driving forces and a much larger view of

what should be preserved. Preservationists point to sturdy houses and commercial districts

with “good bones” and unique architecture as the basis for neighborhood revitalization.

They see incentives for reinvesting in buildings as tools that help build wealth for longtime

homeowners. They promote mixed-use buildings and neighborhoods with a mix of

unit sizes as opportunities to start businesses, foster socioeconomic diversity, and preserve

informal affordable housing, as with the “Older, Smaller, Better” work of the Preservation

Green Lab at the National Trust for Historic Preservation.2

They emphasize that reoccupying

a vacant house keeps it from being demolished and its remains dumped in a landfill. Finally,

they value building community capacity through deep public engagement, while new technologies

create opportunities for more inclusive planning, such as the Austin Historical

Wiki Project and the Detroit Historic Resource Survey. While these ideas are rooted in the

preservation movement’s origins, their traction and application within the field has been

limited. Renewed attention to middle neighborhoods and legacy cities is a fresh opportunity

to promote these ideas, to examine how preservation frameworks and tools can be more

equitable and useful, and to be taken seriously by other stakeholders, including politicians,

planners, land bank officials, financial institutions, and community members.

Preservation’s “Triple Bottom Line” Value Proposition

The physical fabric of most middle neighborhoods offers many desirable characteristics

aligned to advance complementary goals of sustainability and health, social equity, and

economic prosperity. This triple bottom line payoff for middle neighborhood stabilization

is rooted in the fact that the existing physical inventory of middle neighborhoods is relatively

dense.3

Although the age of the building stock may often require substantial system

upgrades, the compact urban form of many middle neighborhoods offers increased walkability

and decreased vehicle miles traveled compared with newer developments. These characteristics,

similar to those aligned with smart growth principles, are associated with lower

rates of asthma, obesity, and heart disease, as well as lower incidence of car crash fatalities.4

Moreover, reduced dependence on private cars, increased rates of walking, and greater

use of public transportation result in a smaller carbon footprint.5

Finally, when comparing buildings of equivalent size and function, building reuse almost always offers environmental

savings over demolition and new construction.6

In other words, keeping a relatively dense

neighborhood as dense as possible has all the positive benefits associated with smart growth—

notwithstanding the challenges placed on the real estate market by low demand or other

negative effects of high numbers of vacant buildings.

With respect to economic mobility, density, a variety of sizes and price points, homeownership,

and property values found in older neighborhoods offer toeholds that are generally

absent from newer developments. In his 2009 book, Place, Race, and Story, Ned Kaufman

cites Donovan Rypkema’s research, writing, “A thriving local economy will include ‘small

businesses, non-profit organizations, start-up firms, bootstrap entrepreneurs’ who cannot pay

the high rents commanded by new construction. Old buildings provide ecological niches for

essential activities. Without them, settled communities cannot thrive.”7

Although stabilizing the real estate markets of middle neighborhoods is of primary import

to city governments and community residents, other complementary factors are advanced

through successful neighborhood preservation. Preservation’s intangible values of community

character, social equity, quality of life, memory, and beauty are generally the most lasting

and important arguments for saving buildings and community heritage.8

These intangible

benefits often underpin demand by owner occupiers and investors in homes. They can also

serve as common ground to build new relationships required for the broadly based partnerships

necessary to achieve outcomes. Moreover, existing civic capacity around historic preservation

provides valuable partners, influence, and constituencies in place-based stabilization

efforts. Indeed, as the following case studies demonstrate, preservation groups can be an early

force in convening and furthering neighborhood stabilization initiatives.

In neighborhoods facing substantial change, one social equity concern is very often

voiced: will current residents benefit from the changes that are coming? In addition to the

environmental outcomes and opportunities for investment, neighborhood-based preservation

strategies and tools lean heavily on incremental improvements, as opposed to wholesale

redevelopment, and are much more likely to be helpful for current residents than new

development. Small repairs can help make an older home safe, habitable, and high quality

for years to come. These are also repairs and tools that can be undertaken and obtained by

homeowners, in contrast with the professionalized technical and financing requirements

of new construction. Painting, repairing windows, and some energy efficiency measures

can be completed by homeowners with minimal training. Many homeowners in middle

neighborhoods can afford to make these upkeep repairs. For those who cannot, public or subsidized resources are often available for weatherization and improvements to increase

energy and water efficiency. Unlike complex, large-scale financing tools for new development

(e.g., New Markets Tax Credits), the paperwork for these small home improvement

grants can be handled between homeowners and program administrators such as city staff,

utility companies, or privately run programs like the Heritage Home Program discussed later

in this chapter.

On the community action side, preservation offers a way to organize local residents and

other stakeholders around collective concerns and goals using the tangible built environment.

Stories are one of the most fundamental ways to connect with other people and the

heritage of a place. This may take the form of collecting oral histories about local places and

people, organizing to save a building with local ties or distinctive (or typical) architecture,

or discussing how to guide rehabilitation, new development, or demolition in a way that

preserves the built character of a block or neighborhood.

Community members can take tangible actions through preservation, too. Demolition is

appropriate for many vacant and abandoned buildings, but it must be done by professionals

at a per-building cost ranging from $10,000 for a detached house to $50,000 or more for a row

house with occupied neighbors. Boarding up buildings, on the other hand, can be completed

by neighbors at a weekend work party with hand-held drills and low-cost or donated materials.

As shown by community-led board-ups in Youngstown, Ohio, this “mothballing” helps

people to be active participants in combating blight—to feel that they are taking back their

neighborhood and contributing to a positive upward trend. It also allows breathing room to

see if the market will rebound, while ensuring that vacant buildings are secured from illegal

squatting or other criminal activities.

This last opportunity is a particularly important one in middle neighborhoods, where

decline in demand sometimes leads to lower housing values and higher rates of abandonment

and demolition. Out-of-town investors are often major landholders in these areas and

they are difficult to hold accountable for property maintenance. Taking a careful look at

the building stock and allowing local residents to weigh in on appropriate strategies help to

reclaim a neighborhood in spirit and, more practically, galvanize public pressure to invest

in rehabilitations, board up vacant houses, complete strategic demolitions, and hold inattentive

building owners accountable through targeted code enforcement and tax liens where

applicable. The community-based planning work of the Youngstown Neighborhood Development

Corporation, a case study in this chapter, offers a model for inclusive processes that

invites people to shape their place. Although preserving buildings is not always an outcome

of this process, residents’ motivation for participating often comes from a connection to the

neighborhood’s built environment, and a feeling that the place is distinctive enough to merit

a personal investment of time and energy.

Building Effective Place-Based Partnerships

As discussed, preservation dovetails with many other disciplines shaping place, building

community capacity, and improving local social networks. Collaboration between these

disciplines and the community is critical. This is especially true in middle neighborhoods,

where resources are limited, community needs may be significant and multifaceted, and

residents have historically been disempowered from decision-making about their own neighborhoods.

Particularly in legacy cities, middle neighborhoods face myriad challenges. Vacant

buildings and lots punctuate occupied homes, a downward trend in middle-income jobs

creates a highly uneven patchwork of income levels, and public education quality can be hit

or miss. These challenges are fundamentally interconnected and place-based, with a multiplicity

of players making decisions. Everyone has something at stake, and everyone should

have a place at the table in developing strategies and tools.

A broader definition of preservation creates many collaborative opportunities and

expands the list of stakeholders and partners. Preservation shares goals with many, including:

- Advocates for quality affordable housing and commercial space,

- Programs that seek to increase and maintain homeownership,

- Community wealth-building advocates,

- Community members seeking to improve their neighborhoods in tangible ways,

- Community organizers with the goal of increasing community engagement and

developing capacity for direct involvement and political action, - Local historians looking to preserve community heritage and stories,

- City and neighborhood champions hoping to retain and attract new residents via

unique built character,9 - Sustainability advocates.

The three case studies that follow highlight Ohio organizations working to address most

of these priorities in some way. The case studies represent a range of on-the-ground initiatives

with exceptional track records—not the only work happening in this arena, but some of

the strongest. The programs explored in these case studies are conducted by nonprofit organizations,

county land banks, and private partners using public, private, and self-generated

funding. One program hews to traditional preservation standards; the others simply aim to

keep buildings standing and return them to productive parts of the neighborhood that are

valued both in the economic and community senses.

Youngstown Neighborhood Development Corporation

The Youngstown 2010 plan made national headlines when it was adopted in 2005.

Youngstown was the first legacy city to acknowledge that its decades-long population loss was permanent and would continue unless drastic changes were made.10 It would not regain

the 51 percent of its population that departed between 1960 and 2000. But the plan was optimistic,

citing an opportunity to “change the status quo.” “Many difficult choices will have to

be made as Youngstown recreates itself as a sustainable mid-sized city,” read the first point in

the plan’s framework. Presidential candidate John Edwards called the plan “visionary” during

a 2007 campaign stop in Youngstown, and media in other legacy cities like Detroit looked to

Youngstown’s pragmatic, forward-looking approach as a potential model.11

Youngstown residents accepted the forecast and recommendations for a smaller city. In

fact, they had shaped them as part of a broad-based community engagement process. More

than 5,000 people participated in the plan’s development via community and neighborhood

meetings. Significantly, more than 150 people had a hands-on role in creating the plan via

working groups that articulated how to realize an overall vision for the city. The American

Planning Association recognized Youngstown 2010 with its Public Outreach Award in 2007,

and in 2010 the New York Times featured “civic energy” as a bright spot in Youngstown’s

ongoing struggle with vacancies.12

Starting Small: Idora

The Youngstown Neighborhood Development Corporation (YNDC) was established in

2009 with a focus on Idora, a residential, predominantly single-family neighborhood on the

city’s southside. In many ways, Idora was typical of Youngstown as a whole. Established as

an early streetcar suburb in the early twentieth century, the neighborhood prospered until

the collapse of the steel industry in the late 1970s.13 In the next three decades, the neighborhood

lost 36 percent of its population: less than the citywide population decline of roughly

50 percent, but still substantial.

As one of Youngstown’s more viable neighborhoods, Idora was an early target for stabilization.14

Youngstown 2010 prioritized the stabilization of viable neighborhoods as one of

its four guiding themes: “a starting point from which to reclaim some of the adjacent neighborhoods

that have not so successfully withstood the test of time.” In 2009, a report from

the National Vacant Properties Campaign (now the Center for Community Progress) underscored

the importance of focusing comprehensive strategies in viable neighborhoods like Idora.15 It also noted an issue not uncommon in legacy city neighborhoods: even though 27

percent of buildings in the neighborhood were vacant at the time, according to Ian Beniston,

the executive director of YNDC, the report pointed out that “the same problem… is likely

to be true in other neighborhoods in the city which are still potentially viable.”

A 2008 neighborhood plan for Idora cited an 86 percent occupancy rate and 67 percent

homeownership rate—both roughly proportional to the city as a whole.16 However, the

neighborhood had higher rates of poverty, lower education, and a median home value of

just $33,767, nearly 20 percent lower than the citywide median of $40,900. More than onequarter

of buildings and 15 percent of parcels in the neighborhood were vacant; Youngstown

had a combined vacancy rate of 40 percent.17

The Idora Comprehensive Neighborhood Plan named six goals: increasing safety,

increasing pride, revitalizing the neighborhood’s commercial corridor, preserving existing

housing, reclaiming vacant land and structures, and cleaning and greening the neighborhood.

Youngstown Neighborhood Development Corporation tackled most of these goals,

with the overall aim of catalyzing reinvestment in the neighborhood. From the beginning,

the organization took a multipronged approach to neighborhood stabilization and revitalization,

with tactics including demolition, greening, and reuse of vacant lots; partnerships with

code enforcement; home repairs, rehabilitation, and sales; public art; and the development

of community gardens and an urban farm in the neighborhood.

By 2012, four years after work began, YNDC had demolished 93 houses, rehabilitated

43 vacant and owner-occupied houses and completed minor repairs to 30 more, boarded up

40 houses, and cleaned and repurposed more than 150 vacant lots composing more than 17

acres into uses such as community gardens, native planting sites, and side yard expansions.18

It had launched a Community Loan Fund to provide mortgages in target neighborhoods,

financial training for homebuyers, and repair funds. It had also completed homeownership

training for 36 people and developed job training for city residents.

Community-Powered

YNDC’s work in Idora and other middle neighborhoods has built on and expanded the

focus in Youngstown 2010 of engaging community members. “REVITALIZE” is emblazoned

on YNDC annual reports and materials. The houses that YNDC rehabilitates are frequently

advertised as “revitalized” instead of “renovated.” The word is “a call to action,” says Tom

Hetrick, YNDC’s neighborhood planner. “It gets different groups involved in helping to

improve the community.”

YNDC’s website highlights the need for “a renewed sense of ownership and community

among residents. We must leverage the most important asset in our neighborhoods: the time,

energy and resources of existing residents.” Even more directly, many YNDC plans, t-shirts,

vehicles, and even a storage facility bear the slogan “STAND UP—FIGHT BLIGHT.” The

responsibility is clear.

Although YNDC staff and City of Youngstown planners develop each Neighborhood

Action Plan, public meetings give neighborhood stakeholders the opportunity to identify

local priorities and assets at the beginning of the planning process, and offer feedback on

specific strategies during the process. When each plan is completed, Neighborhood Action

Teams composed of local leaders and residents are charged with implementation. Beniston

says that each team plays a central role as “the infrastructure to communicate and implement

the plans.” It meets quarterly to update a list of priority properties and provides a local

communication network for YNDC and the City to better connect with residents. In turn,

YNDC staff track the work of Neighborhood Action Teams and report back on impact at

the end of each year.

Neighborhood residents also have the opportunity to roll up their sleeves at community

workdays held in each of YNDC’s ten target neighborhoods. More than 1,200 volunteers

showed up to 26 workdays in 2015 to clean vacant lots, clear debris from vacant houses

and lots, board up 553 houses, and help with basic rehabilitation tasks. Volunteers cleaned

and secured more than 200 vacant buildings. A robust AmeriCorps volunteer program also

provides on-the-job construction training for city residents—13 local residents worked across

25 neighborhoods in 2015 as part of the program. If neighborhood groups want to do boardups

on their own, they can look to the YNDC’s “Board-Up Manual” for guidance.

Whether as one-time volunteers, returning volunteers, or AmeriCorps members, handson

work helps people see what is happening in their neighborhood. In the short run, says

Beniston, “they want to become a part of it so they can get more done.” And in the long run,

“It helps instill pride in their neighborhoods.”

On the Ground Revitalization

YNDC’s work advances parcel by parcel. When it completes a Neighborhood Action

Plan, YNDC makes recommendations for all buildings in the area that are vacant or have

code violations. The recommendations are based largely on field surveys, but also incorporate

data on ownership, including absentee owners, how recently the property has been transferred,

and delinquent taxes. To provide tangible items for immediate actions, 25 “priority

properties” are identified on the basis of factors such as code violations, severity of deterioration,

public safety, and proximity to assets and otherwise stable areas. Community members

adjust this list as needed, and it is updated as properties are demolished, rehabilitated, or

code violations are brought into compliance.

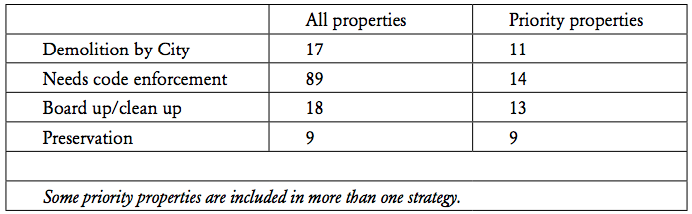

In a recently completed Neighborhood Action Plan for the Wick Park neighborhood, the

majority of properties were recommended for code enforcement (Table 1). Of the 25 priority properties identified for immediate action by the Neighborhood Action Team, just under onehalf

were recommended for near-term demolition by the City, with the remaining properties

recommended for code enforcement and boarding up. (As used in the table, “preservation”

denotes long-term board-ups of buildings that have architectural value, but whose size, rehab

cost, and/or surrounding market conditions may preclude immediate rehab and resale.)

Table 1

Wick Park Neighborhood Housing and Property Strategies

Because much of YNDC’s rehabilitation work is unsubsidized, most decisions about

vacant buildings come down to whether YNDC can rehab and resell them at a profit or

at least without significant loss. The Mahoning County Land Bank partners with YNDC

to transfer tax-foreclosed buildings at no cost, but a typical rehabilitation costs $20-$30

per square foot—between $30,000 and $80,000 for recent projects, according to Beniston.

AmeriCorps volunteers and YNDC construction crews complete the work, with community

members providing assistance on unskilled tasks such as cleaning out debris and painting.

If the local market will absorb a rehabilitated house at or near the rehab cost, YNDC says

it is worth the work. In addition to providing jobs and job training, renovated houses help

repopulate a neighborhood with owner-occupants, increase the value of the property and

adjacent houses, and build the city’s property tax base. A vacant lot is worth $250; a rehabbed

house is worth $60,000, and saving it preserves neighborhood character. “The homes that

we’re rehabilitating have more character than all the similar product in the suburbs, and

they’re totally updated,” says Beniston.

Residents often champion rehabilitation of vacant houses rather than demolition. “Most

people want the houses reoccupied,” says Beniston. “They don’t want their whole neighborhood

torn down.” Community members push back against some recommended demolitions

during the Neighborhood Action Plan process or in subsequent Action Team meetings,

where proposed parcel-level strategies are examined in detail. Some go further. One local

group is hiring an intern to market rehabbed houses in its neighborhood. In select cases

when vacant buildings have significant architectural or other value and community members

advocate for rehabilitation, but near-term sales are unlikely, YNDC assigns a “preservation”

strategy to the buildings and boards them up.

YNDC’s rehab work is not limited to vacant buildings. The organization’s Community

Loan Fund offers long-term financial counseling coupled with mortgages to homebuyers

who have been denied an affordable loan by traditional lending institutions. This “high

accountability, character-based approach” allows community members to purchase YNDC-rehabilitated

houses and complete minor repairs, even with imperfect credit in a conservative

lending market.19 The program is offered in partnership with the city, state, a local foundation,

a local bank, HUD-certified counseling agencies, and others. For owner-occupied

houses, the Paint Youngstown program provides free external repairs to avoid potential code

violations and improve the overall image of the neighborhood.

Impacts

As any legacy city resident knows, stabilizing a neighborhood market takes time and

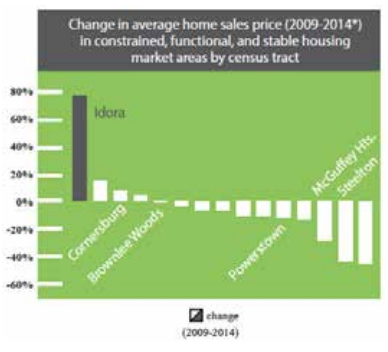

requires much more than just fixing one house. Since work began in Idora in 2009, vacancy

rates have dropped roughly 8 percent and average sales prices have risen nearly 80 percent.

In those seven years, YNDC has rehabilitated and resold 31 vacant homes, repaired 84

additional homes for low-income homeowners, boarded up 46 vacant houses, and provided

loans to 19 homeowners through its Community Loan Fund.20 Nearly 130 buildings have

been demolished, and close to 200 vacant lots have been repurposed as gardens, parks,

recreation, events, and an urban farm. All this has bolstered market confidence: more than

160 property owners have made significant investments in their homes since 2009. And the

organization’s work continues in the neighborhood.

from Youngstown Neighborhood Development Corporation.

YNDC expanded its focus beyond Idora to other middle neighborhoods in Youngstown,

guided by a 2014 Neighborhood Conditions Report that classified neighborhoods by market

strength, from extremely weak to stable. YNDC is now working in nine other constrained

and functional neighborhoods using Neighborhood Action Plans and Neighborhood Action

Teams. In 2015, the organization completed two owner-occupied rehabilitations, 27 limited

repair projects for homeowners, brought 41 properties into code compliance, rehabbed 45

properties, cleaned up or boarded up 228 houses, and worked with the City and the land

bank to prioritize demolitions of 220 houses.

The change, according to Beniston, goes well beyond the numbers: “We can look at the

data all we want, and we know that’s critical, but another piece is that these are neighborhoods

that people live in… We value what people think of their neighborhoods and their

priorities for buildings.”

Ohio’s Heritage Home Program – Pioneered By Cleveland Restoration Society

The Heritage Home ProgramSM supports preservation projects across 42 communities in

northeast Ohio, but it does so by almost any other name than “historic preservation.” Lowinterest

loans are available to “older houses,” while “old house experts” provide technical

advice. Any residential building with three or fewer units qualifies if it was constructed more

than 50 years ago—no historic designation required.

Yet preservation it is. All exterior work must comply with the gold standard for preservation

projects, the Secretary of the Interior’s Standards for Rehabilitation, and loan

funds cannot be used for historically incompatible alterations such as vinyl siding or vinyl

windows. Participating property owners—largely homeowners—are required to consult with

program staff while planning their project. The same staff members inspect the finished

project to ensure that it complies with the program’s “master specifications,” a detailed set

of technical standards.

Initially, the program was limited to houses in historic districts. But by 2012, foreclosures

during the Great Recession continued to decimate residential neighborhoods in and around

Cleveland. The Cleveland Restoration Society (CRS), the 44-year-old preservation organization

that initiated the Heritage Home Program in 1992 and continues to operate it, saw a

need for action. “It became not just fixing up historic homes, but about keeping people in

their homes and their neighborhoods,” said Margaret Lann, the Heritage Home Program

associate at CRS. There was also, she added, a bigger question, how to extend the program to

people in older homes so they can improve their homes and remain in them? Consequently,

CRS made some significant changes. It:

- Opened up the program to any house more than 50 years old;

- Expanded loan-eligible projects to include all forms of general rehabilitation, so long

as the project is consistent with the architectural style of the house; - Aggressively marketed the program to additional communities; and

- Reduced program fees and interest rates to attract more participants.

These changes were in line with CRS’s progressive preservation ethos, which sees preservation

as a powerful tool to advance the goals of community revitalization, a stronger

regional economy, and higher quality of life.21

The Heritage Home Program remains available to any older house, but it incentivizes

preservation-friendly decisions via inexpensive loan funds (with fixed-rate financing as low

as 1.4 percent), education, and technical assistance. It also effectively addresses three of the

top objections to buying older houses: the cost of maintenance, the specialized knowledge

required of homeowners, and the functional obsolescence of kitchens and bathrooms in

older houses. (Heritage Home Program loans can be used to fund those interior improvements

with no historic standards or review.)

The program’s low-interest loans are enabled by a “buy-down” of interest rates from

two local banks. Public funds from the Cuyahoga County and the Ohio Housing Finance

Agency (OHFA) provide capital to subsidize the difference between at-market interest rates

and the lower subsidized rate.22 Loan amounts are determined by an after-rehab appraisal

that estimates the post-rehabilitation home value to establish equity. The loan terms are for

7 to 10 years, with no prepayment penalty. The CRS banking partner can hold the first or

second lien on the property.

Borrowers must meet participating banks’ standard lending requirements, Lann notes.

This includes income sufficient to pay back the loans, though loans subsidized by OHFA

dollars are restricted to low- and moderate-income households earning up to approximately

$76,000 per year. Program staff estimate that, over the life of the program, it has made more

than 300 loans worth $11 million to low- and moderate-income homeowners in northeast

Ohio. (Loans subsidized by Cuyahoga County are unrestricted.)

The Heritage Home Program has become a national model in its nearly 25 years of operation.

According to its website, it has made more than 1,200 low-interest loans for more than

$46 million and provided technical assistance to more than 9,000 homeowners on projects

valued at a total of $200 million. Loans range from $3,000 to $200,000, with an average

loan of $25,000. A Cleveland State University study showed that the loans benefited the

surrounding neighborhoods as well; assessed values and sales prices of homes surrounding

the participating properties increased.23

The Heritage Home Program is open to any age-eligible house in participating communities,

but some communities market the program in targeted ways. The city of Cleveland

Heights is currently planning to focus its marketing efforts to areas hard-hit by the recession,

where homeowners have been hesitant to reinvest in their homes, and the city of Bay Village has done targeted outreach to low- and moderate-income census tracts. The Lucas County

Land Bank is also taking a focused approach in several neighborhoods in and around Toledo,

as will be discussed later.

Technical Assistance

Technical assistance, or “home improvement advice,” is the heart and soul of the Heritage

Home Program. Program staff offer consultations at no charge to owners of older residential

properties in participating communities; homeowners outside those areas and owners of

other building types are charged a small fee. Services include site visits; recommendations

on maintenance, repair, rehab, additions, energy efficiency, and modernization of kitchens

and bathrooms; and construction advice. In addition, staff help evaluate contractor bids and

estimates and provide advice on materials and supplies.

“Not everybody is going to want a program loan, but they want to get the job done

in one way or another,” says Lann. Technical assistance “helps to get those projects done,

hopefully with a preservation approach” that maintains the quality of local architecture and

neighborhood character. Last year, program staff provided free advice to more than 1,500

homeowners.24 In the past 10 years, 8,000 homeowners have used the program’s technical

assistance, including 5,200 site visits.

Although most technical assistance is requested, some is required for loan recipients.

Staff members go on a site visit with prospective borrowers and review the proposed scope of

the project prior to the application’s submission. Before work begins, staff members develop

exterior project specifications in collaboration with the property owner; these are referred to

again during a final inspection.

Program involvement extends to the funding itself. The homeowner is the borrower,

but the lending institution deposits loan funds into an escrow account held by CRS, which

disburses them directly to the contractor as work is completed. According to Lann, CRS sees

the escrow process as added value for multiple parties: it removes the hassle of managing

payouts and contractors for the homeowner, assures the contractor they will get paid, and

provides trusted quality control that reassures banks that the completed project will add

value, which helps them take small risks with lending.

CRS also organizes public workshops on home maintenance and rehabilitation, and an

online preservation toolbox rounds out the program’s technical assistance. Practical topics

are the focus of both programs: painting and color advice, maintenance basics, weatherization,

roof repair, etc.

Impacts

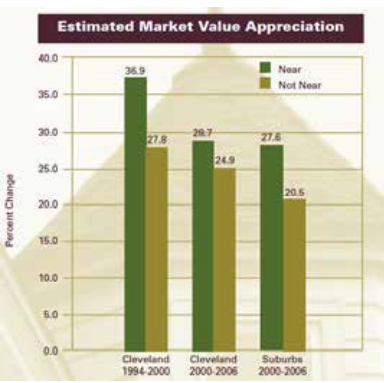

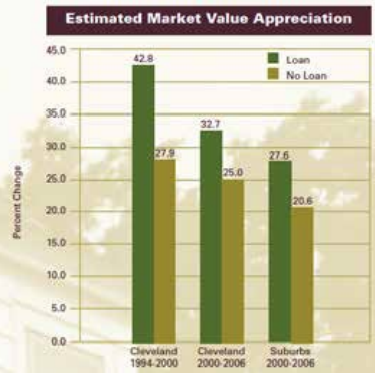

Put simply, houses in the program achieve results. Between 2000 and 2006, the assessed

values of Cleveland properties in the Heritage Home Program rose roughly 8 percent above the values of comparable properties.25 Between 1994 and 2000, the assessed values appreciated

43 percent on average, compared with 28 percent for similar properties. The results

were similar in communities outside Cleveland that adopted the program after 2001. There,

nearly 100 properties saw a median appreciation of 28 percent compared with 21 percent for

comparable properties.

from Biran Mikelbank, Cleveland State University “Does Preservation Pay? Assessing Cleveland Restoration

Society’s Home Improvement Program.

Program participation is also correlated with lower rates of foreclosure, a broad indicator

of neighborhood stability. A study of Heritage Home Program loan properties from 2006 to

2013 found that foreclosure rates for the sample track countywide trends, reflecting difficult

market conditions.26 However, the rate of foreclosure among program participants was 2.9

times (in 2008) to 11.1 times (in 2010) lower than the countywide foreclosure rate. Foreclosure

rates for program participants were also lower than those in their surrounding communities,

both within Cleveland and in inner- and outer-ring suburbs.27

Mikelbank’s “Does Preservation Pay?” study established that the impacts for property

values extend beyond the houses in the program—a particularly important point for middle

neighborhoods where stabilizing and strengthening housing markets may be a priority. The

spillover benefits were measured for houses within one-tenth of a mile of properties that had

received CRS loans. In Cleveland, the sale price of the nearby houses had risen by 10 percent,

compared with a 6 percent increase for other houses. In the surrounding communities, sale prices appreciated by 14 to 50 percent more than sale prices of other houses. Assessed values

also rose more for nearby houses. In Cleveland between 1994 and 2000, assessed values for

nearby houses had appreciated 9 percent more than other houses (37 percent vs. 28 percent);

between 2000 and 2006, the difference was 4 percent higher (29 percent vs. 25 percent).

Outside Cleveland, houses in the tenth of a mile radius were assessed at values roughly 7

percent higher than those outside it (28 percent vs. 21 percent).

The same study also suggested that the loan programs had nonmonetary benefits for the

neighborhood. Few houses in the CRS loan programs sold between 1994 and 2006. Mikelbank

thought that perhaps homeowners who had thoughtfully invested in their homes were

less likely to sell them. If this were the case, the loan program could help encourage lower

turnover and more stability. Lann at CRS noted that the program encourages a shift in attitude,

from regarding a house as an investment—one that will eventually be sold—to seeing it

as an asset that shapes the quality of daily life. “When people do a project that makes their

day-to-day living better and know they’ve invested in their house, they tend to stay in it

longer,” she said.

Lucas County Land Bank

In 2014, CRS licensed the Heritage Home Program to the Lucas County Land Bank,

which was established in 2010 to work in Toledo and surrounding communities in northwest

Ohio. Through this move, and by making the program available for licensing to other land

banks, CRS sought to make rehabilitation a stronger, easier tool for land banks to use.28

According to Lann, licensing also allowed the program to grow beyond CRS’s geographic

area—a key move, given the importance of onsite technical assistance.

The Lucas County Land Bank (“Land Bank”) was no stranger to rehabilitation, with a track

record that included acquisition and resale of 329 houses in its first five years.29 It does not

rehabilitate homes itself, but resells the houses with the condition of renovation to leverage

private dollars. For houses that do not require extensive renovation, offers from prospective

owner-occupants are prioritized. The Land Bank has also worked with local immigrants to

repurpose vacant buildings as part of the Welcome Toledo–Lucas County initiative. The

Land Bank’s “Five Year Progress Report” framed the work in terms of preserving “the fabric

of our neighborhoods”: “Each vacant property that is renovated helps stabilize surrounding

properties by increasing values, eliminating blight, and generating new energy in our neighborhoods

and commercial corridors.”30 This includes partnerships with immigrants.

According to David Mann, the Land Bank’s executive director, the agency sees the Heritage

Home Program as a proactive way to stabilize properties before they deteriorate, encourage upkeep of surrounding properties, and preclude more substantial Land Bank involvement—

in the long run, achieving its mission to strengthen neighborhoods and preserve property

values. According to the “Five Year Progress Report,” a recent survey of every parcel in Toledo

yielded encouraging results about the condition of the housing stock—88 percent of houses

were in good or very good condition. At the same time, it noted, “too many homeowners

cannot keep up with major exterior maintenance”: nearly 16,000 properties, or 17 percent of

all buildings in the city, had missing siding and peeling paint.

Yet the challenging regional real estate market has significant repercussions for property

owners who seek to repair their homes. The foreclosure crisis sent local property values into

a downward spiral, with a 25 to 30 percent reduction in most Toledo neighborhoods, and

home values have remained flat or climbed only slightly in subsequent years, according to

Mann. Combined with banks’ conservative approaches to calculating potential loans, this

means that many homeowners have too little equity in their houses to qualify for a loan,

even with the after-rehab assessments offered by the Heritage Home Program. They are not

able to sell either. This is true even in Toledo’s most stable neighborhoods, says Kathleen

Kovacs, the Heritage Home Program director for the Land Bank.

As a result, technical assistance has by far been the largest component of the Heritage

Home Program in Lucas County. In the 18 months since the program began there, approximately

120 homeowners have taken advantage of the free technical assistance offered by the

program, compared to just two loans made. As in Cleveland and Cuyahoga County, program

staff conduct site visits, help homeowners evaluate and prioritize needed work, determine

what they can do themselves, and review contractor quotes when needed.

“It’s about knowledge-sharing and education,” says Kovacs. “If you leave a homeowner

a little more educated about what they need to do to maintain their home, that leaves the

community better off.” Mann agrees: “If someone has gained real knowledge—or gained real

knowledge and been able to make those improvements—that’s a benefit to the community.”

Both see the Land Bank as a neighborhood resource with a long-term view, and the Heritage

Home Program as a relatively inexpensive investment in—and toolkit for—early preventive

intervention.

The program is open to all age-eligible houses in Lucas County, as in Cleveland, but the

Land Bank has targeted its initial outreach to four neighborhoods in Toledo and one neighborhood

in a suburban community. Kovacs noted that they chose stable and middle neighborhoods

with the goal of preventing the need for other, more intensive land bank services.

They began with two historic districts, one in a stable neighborhood and one in a middle

neighborhood, working intensively with local partners. The program then expanded to two

middle neighborhoods with historic housing stock in Toledo and a suburban neighborhood.

In the four Toledo neighborhoods, technical assistance was in high demand. When it came

to making improvements, most property owners in two of the higher-income neighborhoods

preferred to use their own funds, while some homeowners in the other neighborhoods had

insufficient equity to qualify for loans.

The Land Bank is currently exploring other tools to enable homeowners to complete

necessary work. It just started the RISE (Rebuild, Invest, Stabilize, and Engage) program, a

targeted effort being piloted in Toledo’s character-rich Library Village neighborhood to layer

multiple Land Bank programs and maximize impact. The Land Bank is also considering

whether an existing program to fund energy efficiency improvements in commercial buildings

can be adapted for use with residential properties.31

In the meantime, the Heritage Home Program is aligned with other Land Bank programs:

home sales for renovation, acquisition and resale of commercial buildings for renovation,

and more. The Land Bank actively demolishes vacant houses—with an anticipated 1,800

demolitions by the end of 2016—but it also aims to help maintain neighborhood character

and provide homeowners with strong tools for success, according to its “Five-Year Progress

Report.” “By making direct investments, partnering on renovation projects, and offering the

Heritage Home Program,” says Mann on the Heritage Home Program website, “we hope we

are setting an example for other land banks across the country that balance is key—and it’s

not an either/or.”32

For example, $1.4 million from a Wells Fargo settlement provided partial funding for a

Land Bank roof replacement grant program in 2014–2015.33 The program was targeted to

low- and moderate-income homeowners in three concentrations of majority-minority census

tracts and included similar elements as the Heritage Home Program: homeowner education

through credit counseling and wealth-building classes; technical assistance, with a home

inspection by land bank staff and comprehensive repair list; and funds to replace roofs.34 The program replaced 145 roofs, but the education and assistance had other lasting impacts.

“The homeowners understood that we were going to invest in them in the long term, not the

short term,” Kovacs noted.

Conclusions

Evidence is growing for the positive impact that short-term investment programs—preservation

and otherwise—have when they take a holistic, long-range view of neighborhood stabilization

in middle-market neighborhoods. These targeted, incremental improvements both

benefit current residents and pave the way for much-needed newcomers. A more expansive

view of historic preservation in middle neighborhoods provides neighborhood stabilization

benefits along the equity, health, and environmental axes in addition to encouraging more

robust real estate markets. Preservation tools such as those discussed in this chapter, and others

yet to be tried, deserve careful attention by those seeking to stabilize middle neighborhoods.

This is particularly true because, when owner-occupied, the houses that make up middle

neighborhoods are tremendously important concentrations of wealth for a large proportion

of families.35 Finding ways to stabilize and build market value (and restore market functionality

for fair transactions) of these homes is an essential part of this volume. Underlying these

strategies is an understanding that the historic character, the walkability, the sustainability, and

the feel of these neighborhoods are both valued and an underused source of market demand.

Although it is true that each city, neighborhood, and block is unique, we can draw three

conclusions about the importance of deep partnerships, long-term community engagement,

and targeting limited resources.

The value of strong partnerships cannot be understated. When preservation has been an

effective tool in bringing a community and many external stakeholders together to achieve

tangible results in a neighborhood, it has been rooted in partnerships between many actors,

many of whom may have never previously worked closely together. It is precisely because

different groups bring different experience, connections, and expertise to the table that their

collaborative efforts are far greater than the sum of their parts.

Meaningful community engagement and long-term commitment to a specific community

were also hallmarks of these programs’ success. The Youngstown Neighborhood Development

Corporation has not only conducted community engagement activities in Idora—

it also supports the activities of Neighborhood Action Teams and tracks progress toward

community goals. The result is more proactive and engaged representatives from the local

community. The Heritage Home Program in Lucas County is joined by other land bank

initiatives to build homeowners’ financial acumen and practical know-how. These programs

fall outside traditional land bank activities, but they meet larger goals of neighborhood stabilization

and help community members see the land bank as a long-term partner and resource.

For cities with a high proportion of middle neighborhoods, resources available for investment

strategies are stretched extremely thin. The programs in Slavic Village and Idora have

taken the approach that neighborhood investment strategies should be tailored to neighborhood

conditions to achieve the highest likelihood of results. In Cleveland and Lucas County,

the Cleveland Restoration Society and partners have made more financial resources available

via after-rehab appraisals and lower interest rates. The simultaneous strategy of considering

technical knowledge an important resource adds another dimension of value.

Because they could quickly turn up or down, middle neighborhoods in legacy cities

offer unique opportunities for program innovation, as well as and for substantial returns on

limited investments. We see an economic, equity, and environmental case for substantial

increases in the strategic deployment in middle neighborhoods of programs that increase

neighborhood curb appeal characteristics, such as (relatively) small-scale facade improvement

grant and loan programs. This volatile context also makes it challenging to evaluate

programs that intervene and underscores the need for careful research.

It is worth noting that those seeking to stabilize middle neighborhoods through preservation

strategies often point to an absence of compelling quantitative research to share with

stakeholders, funders and regulators around the benefits of neighborhood-scale preservation

programs. Future research that would be helpful in this arena would analyze a broad range of

neighborhood stabilization tactics (e.g., occupant support, rehab, stabilization, mothballing,

demolition, and vacant property uses) with regard to impacts on foreclosures, property

values, and other demographic effects.

In the short term, we will be eying a few emerging programs, including the Healthy

Rowhouse Project in Philadelphia; Rehabbed and Ready, a public-private partnership to renovate

and auction homes in Detroit; and the Detroit Neighborhood Initiative—all oriented

around furthering affordable homeownership in older neighborhoods. The Lucas County

Land Bank’s RISE program in Toledo (to be launched in 2016) and the Slavic Village Recovery

Project in Cleveland also merit observation and full evaluation over the next few years.

Programs such as those in Youngstown’s Idora neighborhood and the Heritage Home

Program around Cleveland and in Lucas County reflect a new paradigm of holistic and

broadly based historic preservation. With a practical orientation to contemporary community

needs, historic preservation can help ensure that the older building stock of a neighborhood

can effectively meet the triple bottom line goals of economics, equity, and the

environment for future residents and those who, for a very long time, have called these

neighborhoods home.

1. Historic tax credits are available federally for designated historic buildings that are also income-producing;

the credit comprises 20 percent of qualified rehabilitation expenditures and requires rehabilitation work to

comply with the Secretary of the Interior’s Standards for Rehabilitation. More than 30 states and many more

cities offer historic tax credits that can be layered with the federal tax credits. A lesser-known 10 percent

federal historic tax credit is available for nonresidential buildings constructed before 1936 that retain a

substantial amount of their original structure and walls. There is no formal review process for work completed

using this credit. Many states also have tax credits for restoration of historic structures.

2. Preservation Green Lab, National Trust for Historic Preservation, Older, Smaller, Better: Measuring How

the Character of Buildings and Blocks Influences Urban Vitality, May 2014, www.preservationnation.org/information-center/sustainable-communities/green-lab/oldersmallerbetter/report/NTHP_PGL_OlderSmallerBetter_ReportOnly.pdf.

3. For Youngstown neighborhood density, see Youngstown Neighborhood Development Corporation, City

of Youngstown, Neighborhood Conditions Report, 2013 p. 13; Cuyahoga County municipal population

densities are available at http://planning.co.cuyahoga.oh.us/census/2010land.html.

4. Reid Ewing and Shima Hamidi, “Measuring Urban Sprawl and Validating Sprawl Measures” (Salt Lake City:

Metropolitan Research Center at the University of Utah for the National Cancer Institute, the Brookings

Institution, and Smart Growth America, 2014), p. 43.

5. Ibid.

6. Preservation Green Lab, “The Greenest Building: Quantifying the Environmental Value of Building Reuse”

(Washington, DC: National Trust for Historic Preservation, 2011). The study found that it takes “10 to 80

years for a new building that is 30 percent more efficient than an average-performing existing building to

overcome, through efficient operations, the negative climate change impacts related to the construction

process” (p. vii).

7. Ned Kaufman, Place, Race, and Story (New York: Routledge, 2009), p. 400.

8. Ibid., p. 396.

9. See Marcia Nedland’s chapter in this volume.

10. City of Youngstown and Youngstown State University, “Youngstown 2010” (Youngstown, OH: City of

Youngstown, 2003).

11. David Skolnik, “Edwards Called City’s 2010 Plan ‘Visionary,’” The Vindicator, July 18, 2007, www.vindy.com/news/2007/jul/18/edwards-called-city8217s-2010-plan/; Terry Parris, Jr., “Youngstown 2010: What Shrinkage

Looks Like, What Detroit Could Learn,” Model D, May 4, 2010, http://modeldmedia.com/features/ytownplan5022010.aspx.

12. Sabrina Tavernise, “Trying to Overcome the Stubborn Blight of Vacancies,” New York Times, December 19,

2010, www.nytimes.com/2010/12/20/us/20youngstown.html.

13. “Idora Comprehensive Neighborhood Plan” (Youngstown, OH: City of Youngstown Planning

Department and Ohio State University, March 2008), www.cityofyoungstownoh.org/about_youngstown/youngstown_2010/neighborhoods/south/idora/idora.aspx.

14. Youngstown uses the terms “constrained” and “functional” markets to refer to middle neighborhoods.

15. Dan Kildee et al., “Regenerating Youngstown and Mahoning County through Vacant Property Reclamation:

Reforming Systems and Right-sizing Markets” (Washington, DC: National Vacant Properties Campaign,

February 2009).

16. Data from Census 2000; “Idora Neighborhood Comprehensive Neighborhood Plan.”

17. Tavernise, “Trying to Overcome the Stubborn Blight of Vacancies.” Youngstown had 4,500 vacant buildings

and more than 23,000 vacant parcels.

18. Ian J. Beniston, “Idora: Creating a Smaller Stronger Neighborhood.” Presentation at the Thriving

Communities Ohio Land Bank Conference, November 28, 2012, www.wrlandconservancy.org/documents/F2-Idora-CreatingaSmallerStrongerNeighborhood.pdf.

19. Ian Beniston, email to the authors, 3/16/2016.

20. Youngstown Neighborhood Development Corporation, “Evidence-based Neighborhood Revitalization: The

Idora Neighborhood in Youngstown, Ohio” (Youngstown Neighborhood Development Corporation, 2015).

21. “Mission, Vision & Strategy,” Cleveland Restoration Society, clevelandrestoration.org/about/vision.php.

22. Heritage Home Program, “Loan Subsidy Application,” heritagehomeprogram.org/assets/pdf_files/Heritage%20Home%20Program%20Application.pdf.

23. Brian Mikelbank, “Does Preservation Pay? Assessing Cleveland Restoration Society’s Home Improvement

Program” (Cleveland State University, n.d.).

24. Heritage Home Program, “Loan Subsidy Application.”

25. Mikelbank, “Does Preservation Pay?”

26. Brian A. Mikelbank, “In Search of Stability: Adding Residential Preservation to the Planner’s Toolkit,”

unpublished manuscript, 2015, p. 15-16.

27. Ibid., p. 17, 20.

28. “Licensing the HPP: A Tool for County Landbanks” (Cleveland: Cleveland Restoration Society, n.d.), www.heritagehomeprogram.org/joinus/licensing.php.

29. Homes acquired for rehabilitation made up 30 percent of residential building acquisitions; the other 70

percent of houses were acquired for demolition. Lucas County Land Bank, “Five Year Progress Report: 2010-

2015” (Toledo: Lucas County Land Bank, 2015), p. 6, http://co.lucas.oh.us/DocumentCenter/View/55765.

30. Ibid.

31. The Property Assessed Clean Energy program (PACE) is administered through the Toledo Port Authority.

It allows property owners to borrow money to make energy efficiency improvements such as windows,

insulation, and boilers. Debt is assessed directly to property taxes and paid in installments and is transferable

to a new owner.

32. CRS, “Licensing the HPP.”

33. Lucas County Land Bank, “Five Year Progress Report.”

34. Ibid.; Lucas County Land Bank, “Neighborhood Roof Replacement Program” application packet.

35. See Mallach in this volume, “Homeownership and the Stability of the Middle Market Neighborhood.”

Cara Bertron is the Chair of the Preservation Rightsizing Network, which works in legacy cities to

preserve local heritage and revitalize the built environment. She has completed preservation-based planning

and revitalization projects in numerous cities, including Seattle, Philadelphia, San Francisco, Cincinnati,

and Charleston. Her work includes innovative historic resource scans, citywide preservation plans, and

neighborhood community development projects with a focus on equity and data-driven decision making.

She was the principal author of the Action Agenda for Historic Preservation in Legacy Cities.

Nicholas Hamilton is Director of Urban Policy at The American Assembly, Columbia University’s

bipartisan policy institute. There, Mr. Hamilton leads the Legacy Cities Partnership, a national coalition

working to revitalize America’s legacy cities. His work focuses on economic development, governance,

and civic engagement. Mr. Hamilton’s previous architectural and urban design work for the firm

Davis Brody Bond included the master planning and design of US diplomatic facilities abroad as well

as laboratory and teaching facilities for Columbia and Princeton Universities.