Recent economic research has made prescient the assertion in 1966 of Nobel Laureate Merton Miller that “[the idea] that financial markets contribute to economic growth is a proposition too obvious for serious discussion,”1 but there is still limited research exploring the role financial institutions, such as banks, should play in adaptation efforts in the face of climate change. The 5th Assessment Report of the Intergovernmental Panel on Climate Change (IPCC) includes an entire working group report focused on approaches for societal adaptation for climate change,2 but still only includes minimal guidance on the way in which banks could adapt lending and asset management policies.3 Rather than a lack of recognition of the role banks could play in the allocation of capital towards positive adaptive investments,4 which include any investments meant to reduce future costs due to climate change, we believe the report omits this discussion because “adaptation is place- and context-specific” so it is challenging to provide a flexible solution likely to offer appropriate guidance in areas that face such heterogeneity.

How then are we to proceed in the face of such challenges? One possibility is to continue efforts with local government, but with an increased focus on potential feedback mechanisms through the local banking sector. However, such an approach sidelines banks that, evidence suggests, are critical in providing efficient local allocation of capital for investment,5 which is exactly the problem being faced in determining adaptation outlays. Leveraging private financial institutions, such as banks, in the adaptation process, may provide substantial benefits to exposed communities. Or in the words of James Titus, former project manager for sea level rise at the U.S. Environmental Protection Agency (EPA), is there a “strategy [that] minimize[s] governmental interference with decisions best made by the private sector?”6 The 5th Assessment Report of the IPCC therefore suggests that there may perhaps be “emerging economic instruments [that] can foster adaptation by providing incentives for anticipating and reducing impacts” but doesn’t indicate yet exactly what instruments these may be.7 In this article, we provide evidence of recent research which suggests that local property values may provide one potential economic instrument to assist in incentivizing adaptive banking.8

Challenges of Lending for Adaptation

Lending by private institutions, such as banks, for adaptive investments face two major hurdles in the form of externalities. The first challenge, concurrent externalities, is commonplace for virtually any investment project and has been one of the most basic concepts in modern economic theory since the work of Henry Sidgwick and Arthur Pigou in the late 19th and early 20th centuries, respectively. Namely, externalities for an investment made feasible with capital from a bank are unlikely to be accounted for in the allocation process. For example, the interest rate charged to provide financing for the construction of a noisy and odorous sewage processing plant may not be any higher if it is right next to a restaurant. One way to approach such a problem is to rely on local governments to provide the capital for projects with large positive externalities and regulation to limits those with negative externalities. This of course limits any assistance from those institutions, such as banks, likely to have local allocative knowledge and incentives.

If the goal is to gain the assistance of private institutions, while maintaining appropriate incentives, the work of Nobel Laureate Ronald Coase provides some guidance. In simplified terms, the Coase Theorem shows that if transaction costs are sufficiently low, and there exists an economic instrument to trade an externality, bargaining will lead to a Pareto efficient9 allocation regardless of who receives the instrument initially.10 While there are a broad set of potentially reasonable critiques of the Coase Theorem in practice,11 what should be clear is that the existence of an instrument tied to the value of the externality has the potential to provide more appropriate allocations if properly used. If a bank had an asset tied to the value of restaurants in the area, they would be less likely to provide an inappropriately low-cost loan to the sewage plant discussed earlier. Unfortunately, in the case of adaptive banking, equity prices do not appear to respond to long-run climate risks and so won’t respond to adaptations intended to reduce those risks.12

Therefore, the second challenge, and likely the most difficult, when encouraging adaptive lending practices for climate change is the extremely long-term nature of the externalities caused by many of these investments. There is an expansive literature showing that “short-termism” on the part of decision makers, can lead to adverse long-run outcomes.13 By the same logic, political terms, loan lengths, and bank manager turnover make it unlikely that gains or losses from adaptative investments will be realized in time to alter these parties’ current behaviors. Or, as was noted in the 5th IPCC report, “poor planning or implementation, overemphasizing short-term outcomes or failing to sufficiently anticipate consequences can result in maladaptation, increasing the vulnerability or exposure of the target group in the future or the vulnerability of other people, places or sectors.”14 Once again, one approach is to find a financial instrument that tracks the value of the externality and uses that to align incentives. In the next section, we will argue that unlike equity prices, real estate not only has the potential to price long-run risks, such as climate change, but already appears to be doing so.

Property Values and Climate Change

Empirical evidence from recent research suggests that current house prices are already altered by temporally distant climate change-related risks because of the concerns of real estate investors. Why might this be true in real estate, when it appears to be absent in other asset classes like equities? Real estate is much more likely to have value even far into the future, long after many current firms may have gone bankrupt from excessive risk-taking. Also, anecdotally, property is something households appear to consider as bequest motives for passing on to future generations, in which case, concerns even very far into the future may have the potential to alter the value of property in the present day. In fact, research indicates that people are willing to pay ten percent more for a 700-year lease than they are for an identical property with a 100-year lease.15 This suggests that potential real estate owners appear to care substantially about ownership and value of the property even 100 years into the future.

What does this mean for the relationship between climate change and property values? In addition to anecdotal reports by news media,16 researchers in 2017 conducted 48 semi-structured interviews in Miami-Dade County (MDC)—a location with overwhelming exposure to climate change from sea level rise—with local officials, researchers, real estate developers, investors, financiers, residents, and activists and found a consensus that “high-elevation property would increase in value over the long-term with SLR [sea level rise] and that preferences relating to flood risk (climate-change related or not) were increasingly being recognized among consumers and real estate actors.”17 This consensus was supported by the researchers empirically by examining 107,984 single family home transactions in MDC from 1971-2017. After including linear controls for age, square footage, and transaction date, the authors found evidence in support of the hypothesis that higher elevation properties had appreciated more quickly than lower elevation properties over the last 47 years in MDC. The authors are careful to note that “since elevation was the only locational factor, it is possible that the results simple demonstrate a correlation between location and price appreciation.”18 What this means is that since higher elevation properties tend to differ systematically along other dimensions from lower elevation, the observed price appreciation may have been driven by aggregate trends over time in the value of other characteristics, or even something as simple as actual flooding damage. While these results can’t be taken as causal, the finding of faster appreciation for higher elevation properties in MDC is suggestive evidence that SLR may already be affecting house prices and consistent with first-hand accounts from the interviews these researchers conducted.

Concerns about interpretation have been alleviated in complementary concurrent research by providing the first evidence of a direct casual effect of SLR on property values by showing that coastal properties exposed to projected SLR sell at an approximately seven percent discount relative to otherwise similar properties in a nationwide sample.19 There is a broad set of empirical challenges in obtaining causal interpretation of the price effect of SLR exposure on coastal real estate, the most prominent of which is that exposure probability decreases with distance to the coast and properties closer to the coast differ systematically from those that are farther away. The main method used in this paper to address such identification concerns is to compare more than 465,000 residential property transactions from 2007-2016 within a quarter mile of the coast that are identical on observable dimensions, except SLR exposure. In the workhorse specification, the authors compare exposed and unexposed homes with the same property characteristics (e.g., bedrooms, property type), sold in the same month, within the same ZIP Code, in the same 200-foot band of distance to coast, and in the same two-meter elevation bucket, as well as controlling separately for any price differences due to property square footage. Within each fixed effect bucket, some of the variation in SLR exposure is due to very granular changes in elevation (even within a two-meter elevation bin the expected time until inundation can vary by over a century), but directly observable factors like elevation and coastal distance of a property combine to explain at most 45 percent of the residual SLR exposure.

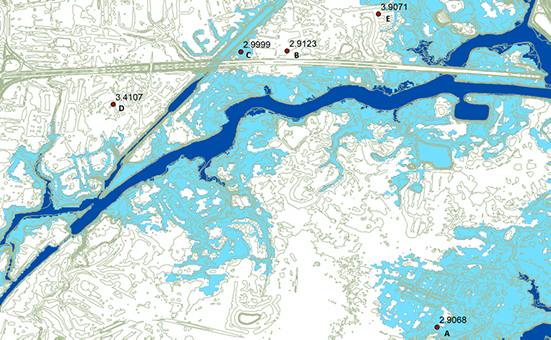

An example of the kind of variation exploited is depicted in Figure 1 which plots the elevation and location of all transactions in July of 2014 in ZIP Code 23323 (in Chesapeake, VA) that involve a property that is (1) between 0.16 and 0.25 miles from the coast, (2) elevated between two and four meters above sea level, (3) four bedrooms, (4) a non-condominium, (5) owner occupied, and (6) bought by a non-local buyer.

Figure 1

Example of Within Bin Variation in SLR Exposure

The figure shows that Properties D and E are approximately 0.5 to one meter higher in elevation than properties A, B, and C and are unexposed to a six-foot SLR. Thus, there is variation in SLR exposure within each fixed effect bucket that is due to very granular changes in elevation. Figure 1 also shows that exposure is not monotonically associated with elevation. Comparing properties, A, B, and C in the figure shows that property C is higher than A and the same distance from the coast, but A has higher elevations between it and the coast (as well as a highway) that appear to reduce SLR exposure.

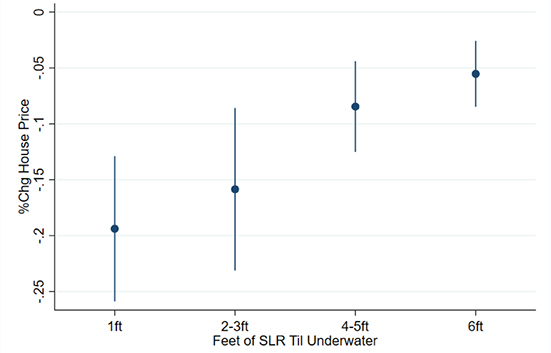

Using the type of variation illustrated in Figure 1 the authors estimate that SLR-exposed properties trade at a 6.6 percent discount relative to comparable unexposed properties. They then further break this into exposure buckets, with properties that will be inundated after one foot of global average SLR trading at a 14.7 percent discount, properties inundated with two-to-three feet of SLR trading at a 13.8 percent discount, and properties inundated with four-to-five and six feet of SLR trading at 7.8 percent and 4.4 percent discounts, respectively, as illustrated in Figure 2.

Figure 2

SLR Exposure and House Price Effects

Note: These price effects are in line with scientific models of SLR projections20 if we assume full loss at the outset of inundation and use prior estimates of long-run discounts rates.21

The presence of a more than four percent SLR exposure discount in samples not expected to be inundated for almost a century suggests that coastal real estate buyers price long-run SLR exposure risk. Placebo tests using rental properties further bolster this interpretation as there is no relation between SLR exposure and rental prices using the main specification, mitigating the possibility that the SLR exposure discount is due to unobservable differences between exposed and unexposed properties. Indeed, to the extent that a difference in current property quality or flood risk contributes to the SLR exposure discount, rental rates should also be lower for exposed properties. The significance and magnitude of the SLR exposure discount being robust to (i) the inclusion of controls for a wide range of observable property characteristics; (ii) the exclusion of areas with recent flood incidents; (iii) the exclusion of properties listed as having attractive features such as waterfront views; and, (iv) the exclusion of properties likely to have been recently remodeled (i.e., properties listed as having been remodeled, properties that change characteristics over time, or older properties) supplies further evidence that current property quality is not the primary driver of the SLR exposure discount. Instead, the primary conclusion to make from recent empirical evidence is that there is already a causal nationwide effect of climate change risks, and, in particular, SLR risks, on house prices. This suggests that real estate could be exactly the kind of “economic instrument,” described by the IPCC and Coase’s Theorem, that could be used as a tool to help align incentives of the private sector.

Property Values and Climate Change

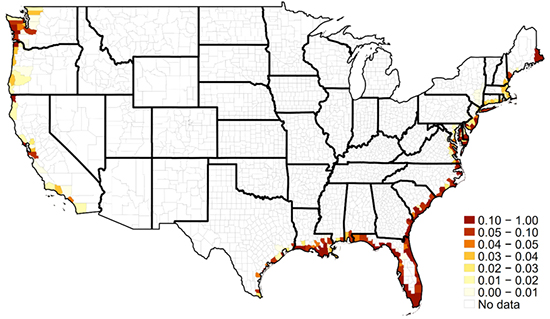

One of the clearest costs associated with future climate change is made evident by rising sea levels. This may give rise to a vision of idyllic wealthy coastal enclaves with more than enough resources to engage in adaptive investments as needed to protect their communities. But such a representation would not be accurate. As has been noted by the Union of Concerned Scientists (UCS), and is made clear in the plots of county-level exposures in Figure 3, the risks of climate change for even something that seems like it should be concentrated among the wealthy, are anything but.22

Figure 3

SLR Exposure and House Price Effects

As noted by the UCS, “nearly 175 communities nationwide can expect significant chronic flooding by 2045, with 10% or more of their housing stock at risk. Of these, nearly 40%—or 67 communities—currently have poverty levels above the national average.”23 This analysis was carried out using granular property level data provided for academic research by Zillow, called ZTRAX. Zillow itself found similar results when exploring the exposure of communities noting in 2017 that “[o]ne-third (32%) of underwater homes would be valued in the bottom third nationally, meaning $123 billion in losses… in urban areas homes in the bottom value tier are more likely to be affected.”24 What this suggests is that low- or moderate-income (LMI) individuals are likely to be adversely affected by SLR, and likely by other risks of climate change as well.

In fact, the risks for these communities could be even larger than they appear at first glance.25 They show that SLR exposure is a first-order consideration for certain segments of the coastal real estate market, but not others. They consistently find evidence that the SLR exposure discount is driven by sophisticated investors, who are not sensitive to local beliefs regarding the effect of climate change and who incorporate new information regarding climate change into their home buying decisions. They find little evidence of SLR exposure discounts among less sophisticated buyers, except in the counties most concerned about climate change, even though housing likely constitutes the majority of their savings.26 Thus, even if sophisticated investors are perfectly pricing the effects of expected SLR exposure, this absence of a current house price discount in less sophisticated market segments raises the possibility of a large wealth shock to coastal communities unless strategies are undertaken to mitigate the effects of SLR.

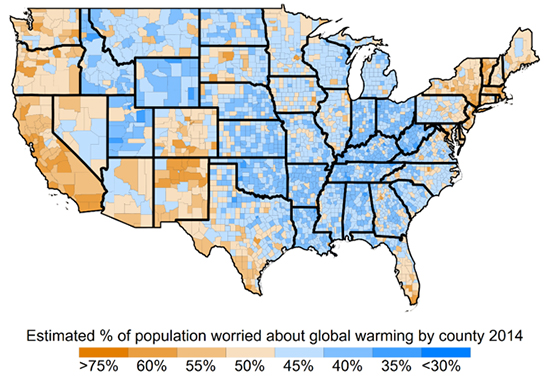

Figure 4

Percent of Adults Who Are Worried About Global Warming

Areas of Louisiana are a perfect illustration of the potential dangers for certain LMI communities. Figure 4 shows the results of the 2014 Yale Climate Opinion Survey which indicates the response to the question “How worried are you about global warming?”27 What is clear when comparing Figures 3 and 4 is that while the southern coast of Louisiana has some of the lowest concern about climate change, they are also some of the most at-risk communities in the entire country. Indeed, the UCS notes that “the largest share of these [communities] is in Louisiana, where there are 25 communities with above-average poverty rates and with 10% or more of the homes at risk by 2045.”28 This is a common finding throughout the country since there is a statistically significant negative relationship between county-level concern about climate change in the Yale survey and SLR exposure.

In the absence of the ability of LMI communities to engage in sufficient adaptive investments on their own behalf the Community Reinvestment Act (CRA) could be a useful regulatory framework to implement adaptive banking policies. Not only are these exactly the communities likely to need additional assistance in raising funds for adaptive investments, they are also the least cognizant of the risks they face.29 The CRA could allow banks to act as not only financial intermediaries, but also act as information intermediaries in a way that should be immediately salient for communities requiring financing.

Conclusion

In light of growing empirical evidence that distant risks of climate change are already affecting current property values, we believe banks can play a pivotal role in arbitrating climate risks. By aligning the performance of loans with long-term property values, Coasean bargaining suggests that banks could be incentivized to subsidize adaptive projects when doing so provides a net benefit to the community. Since communities without substantial financial resources are both the ones most likely to need bank assistance and the most likely to be unaware of the risks they face, the CRA could provide a potential vehicle for incorporating real estate as a means of incentivizing adaptive banking. In addition, banks have the capacity to serve as information intermediaries by providing borrowers with comprehensive information about the long-term risk of individual properties. Nevertheless, we would caution policy makers that, as with all tools, such instruments could lead to adverse consequences, such as increased exposure for banks or unintended migration.

1. Recent empirical evidence supports this as well, including: Guiso, L., Sapienza, P., and Zingales L. “Does Local Financial Development Matter?” The Quarterly Journal of Economics, 119(3) (2004), pp. 929–969; Bekaert, G., Harvey, C., and Lundblad, C. “Does financial liberalization spur growth?” Journal of Financial Economics 77(1) (2005), pp. 3-55; and Hsu, P., Tian X., and Xu, Y. “Financial development and innovation: Cross-country evidence,” Journal of Financial Economics, 112(1) (2014), pp. 116-135, as just a small number of recent examples.

2. Miller, M. “Financial markets and economic growth,” Journal of Applied Corporate Finance, 11 (1998), p. 14.

3. Intergovernmental Panel on Climate Change (IPCC). “2014: Climate Change, Synthesis Report,” Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change (Core Writing Team, R.K. Pachauri and L.A. Meyer [eds.]) (2014), p. 151.

4. Or the strains economic distress could place on the banking sector, and subsequent amplification of such distress via a reduction in available credit from these institutions.

5. See the following for both theoretical and empirical evidence of the role of banks, especially small local banks, in capital allocation: Stein, J. “Information Production and Capital Allocation: Decentralized vs. Hierarchical Firms,” Journal of Finance, 57 (2002), pp. 1891-1921; and Berger, A. et al. “Does function follow organizational form? Evidence from the lending practices of large and small banks,” Journal of Financial Economics, 76, 2, (237) (2005).

6. Titus, J. “Strategies for Adapting to the Greenhouse Effect,” Journal of the American Planning Association (1990), pp. 311-323.

7. IPCC. “2014: Climate Change” (2014), p. 107.

8. By “adaptive banking” we mean any role banks play in reducing future costs associated with climate change. While these include “adaptive investments,” they could also include other banking policies, such as lending or risk management, that alleviate future distress due to climate change.

9. In simple terms, a Pareto efficient allocation is one in which there is no way in which to reallocate without making at least one individual worse off.

10. Coase, R. “The Nature of the Firm,” Economica, 4(16) (1937), p. 386; Coase, R. “The Problem of Social Cost,” Journal of Law and Economics, 3(1) (1960), pp. 1-44.

11. As argued by Coase himself in reality transaction costs of bargaining are almost always non-zero and often fairly high.

12. Hong, H., Li, F.W., and Xu, J. “Climate risks and market efficiency,” Working Paper (2015).

13. Von Thadden, E. “Long-term contracts, short-term investment, and monitoring,” Review of Economic Studies, 62 (1995), pp. 557–575; Stein, J. “Efficient capital markets, inefficient firms: A model of myopic corporate behavior,” Quarterly Journal of Economics, 104 (1989), pp. 655–669; Bolton, P., Scheinkman, J., and Xiong, W. “Executive compensation and short-term behavior in speculative markets,” Review of Economic Studies, 73 (2006), pp. 557–610; Cristina, C., Ellul, A., and Giannetti, M. “Investors’ horizons and the amplification of market shocks,” Review of Financial Studies, 26 (2013), pp. 1607–1648; and Edmans, A., Fang, V., and Lewellen, K. “Equity vesting and managerial myopia,” Review of Financial Studies, 7 (2017), pp. 2229-71.

14. IPCC. “2014: Climate Change” (2014), p. 20.

15. Giglio, S., Maggiori, M., and Stroebel, J. “Very long-run discount rates,” The Quarterly Journal of Economics, 130 (2014), pp. 1-53.

16. See, for example: Urban, I. “Perils of Climate Change Could Swamp Coastal Real Estate,” The New York Times (Nov. 24, 2016).

17. Keenan, J.M., Hill, T., and Gumber, A. “Climate Gentrification: From Theory to Empiricism in Miami-Dade County, Florida,” Environmental Research Letters, 13(5) 054001 (2018). doi: 10.1088/1748-9326/aabb32

18. Ibid.

19. Bernstein, A., Gustafson, M., and Lewis, R. “Disaster on the Horizon: The Price Effect of Sea Level Rise,” Journal of Financial Economics (May 3, 2018), available at http://leeds-faculty.colorado.edu/AsafBernstein/ DisasterOnTheHorizon_PriceOfSLR_BGL.pdf.

20. Parris, A.S. et al. “Global sea level rise scenarios for the united states national climate assessment,” NOAA Technical Report (2012).

21. Giglio, S., Maggiori, M., and Stroebel, J. “Very long-run discount rates,” The Quarterly Journal of Economics, 130 (2014), pp. 1-53.

22. Union of Concerned Scientists. “Underwater: Rising Seas, Chronic Floods, and the Implications for US Coastal Real Estate” (2018), available at https://www.ucsusa.org/sites/default/files/attach/2018/06/underwater-analysis-full-report.pdf.

23. Ibid, p. 9.

24. Bretz, L. “Climate Change and Homes: Who Would Lose the Most to a Rising Tide?” Zillow Research (2017).

25. Bernstein, A., Gustafson, M., and Lewis, R. “Disaster on the Horizon” (2018).

26. Campbell, J.Y. “Household finance,” The Journal of Finance, 61 (2006), pp. 1553–1604.

27. Howe, P. et al. “Geographic variation in opinions on climate change at state and local scales in the USA,” Nature Climate Change, 5 (2015), pp. 596-603.

28. Union of Concerned Scientists. “Underwater” (2018), p. 9.

29. Bernstein, A., Gustafson, M., and Lewis, R. “Disaster on the Horizon” (2018).