The Challenges of Designing for and Reaching Vulnerable Populations

Innovation in highly regulated and complex industries can be extremely costly. This is especially true in financial services, where the legal and regulatory environment creates significant barriers to entry and sustainability for new consumer finance businesses. It typically takes far longer for entrepreneurs to take ideas to prototype, increasing both the costs and the likelihood of failure. Ongoing compliance, risk management, and partner requirements drive increased operating expenses. Investors, therefore, place significant premiums on entrepreneurs with proven track records, industry experience, or strong professional connections that can shorten the time to market and/or reduce execution risk. Despite fintech being touted for its promise to increase financial health amongst diverse and underserved populations, these dynamics have resulted in a starkly homogenous sector. According to Village Capital, women make up just 17 percent of executives at fintech startups, and less than 1 percent of fintech founders are Black.1

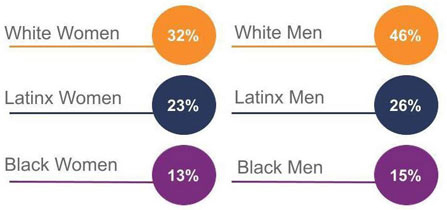

At the same time, estimates from the Financial Health Pulse2 indicate that over two-thirds of people living in America are financially unhealthy, of whom a disproportionate percentage are Black, Latinx, and/or women.3 As of August 2020, only 15 percent of Black people and 24 percent of Latinx people were financially healthy, compared with 39 percent of White people and 39 percent of Asian Americans. The gap in financial health between men and women is also notable, with 40 percent of men versus 28 percent of women financially healthy. As Table 1 shows, these disparities compound, making it even more challenging for people who identify across more than one of these dimensions.

Figure 1

Intersectionality: Percentage of Financially Healthy by Race/Ethnicity and Gender

For the promise of fintech to be realized, we need entrepreneurs with a deep understanding of the lives and livelihoods of vulnerable consumers and the persistent challenges getting in the way of their financial health. Additionally, we need to create a strong, enabling environment of financial services providers, investors, policymakers, and regulators who can help create pathways to scale for solutions that work.

In this article, we explore how our Financial Solutions Lab4 leveraged philanthropic capital and a multi-stakeholder approach to support the development and rollout of two interventions to identify and reach the most vulnerable student loan borrowers during the height of the pandemic.

Reaching Student Loan Borrowers in Need: A Case Study

In early 2020, the Financial Solutions Lab launched its first Collaborative Challenge5 with the aim of co-creating an innovation to support student loan borrowers in distress, especially those who also became unemployed during the pandemic. We were particularly interested in solutions that could continue to help borrowers once emergency measures, like expanded unemployment benefits and the student loan forbearance period, came to an end—knowing that these twin crises would have a significant hit on consumers’ financial health. The design and execution of the Collaborative Challenge serves as an example of how we can harness and direct innovation to where it is needed most.

Understanding the Needs of Vulnerable Student Loan Borrowers

The latest reporting on student loan debt in the United States shows Americans owe more than $1.5 trillion. Although this number is alarming, macro-level indicators are insufficient to provide a more nuanced understanding, such as which borrowers are struggling the most and why. Surely not all borrowers’ circumstances and ability to repay are the same.

A closer look at student loan repayment rates reveals the following:

- The highest rates of default are among borrowers with less than a $5,000 balance.6

- Black and Latinx borrowers have some of the highest default rates in the United States, with 49 percent of Black borrowers and 33 percent of Latinx borrowers defaulting on their payments within a 20-year period.7

- Low-income borrowers are less likely than other borrowers to be enrolled in an Income-Driven Repayment (IDR) plan. Instead, over two-thirds of loan dollars in IDR plans belong to borrowers who are enrolled in graduate and professional school—a group that typically has higher-than-average incomes.8

- Almost 40% of student loan payers are helping someone else pay off their student loan debt, with 27% holding no student loan debt themselves, which underscores the extent to which student loan repayment is a shared family burden beyond the direct borrower.9

Disaggregating student loan repayment data starts to reveal the various and often stark differences between borrowers’ circumstances. The borrowers in the greatest trouble are typically not the ones with high debt, but instead the ones with relatively low balances. Many in this category started a degree but didn’t finish, and thus aren’t enjoying the higher earnings afforded by a degree. Perhaps they were one of the three million students who drop out of college each year because of an unexpected financial emergency of $500 or less.10 This is especially true for Black and Latinx students, who are more likely to come from less well-off families that lack emergency savings and are unable to assist with college-related expenses.

Additionally, low-income borrowers are less likely to participate in IDR plans, suggesting that these borrowers are unaware of, or have had difficulty navigating, such programs. This is partly due to the needlessly complex federal student loan repayment system that administers various programs with different terms and eligibility rules. The result is that people who are underwater on their investment in college may end up defaulting on their loans and paying an unnecessary price.

To better understand the needs of low-income and vulnerable borrowers and to map potential collaboration opportunities, the Collaborative held several workshops with a diverse group of stakeholders who had direct experience working with distressed borrowers, including community-based organizations and nonprofit practitioners, as well as individuals with backgrounds in banking, policy, and digital product design and management.

Through these workshops, there was clear consensus around a need for identifying and reaching vulnerable borrowers with relevant information on the relief measures available to them, including IDR plans. Enrollment in these plans would be especially critical once the student loan forbearance period is set to end.

Equipping Innovators with Flexible Capital, Deep Consumer Finance Expertise, and Network Connections

To move from ideation to action, the Collaborative awarded a grant to two workshop participants: Student Borrower Protection Center11 (SBPC) and Student Debt Crisis12 (SDC). Over several months, these organizations, in partnership with others, embarked on research sprints, iterative product design, and rapid prototyping and testing.

Selected Concepts and Project Teams:

Concept #1: Identifying Distressed Borrowers

Lead Partner: Student Borrower Protection Center

Support Partner: San Francisco’s Office of Financial Empowerment

Concept #2: Development of Tools and Support Resources to Help Borrowers Navigate Relief Options

Lead Partner: Student Debt Crisis

Support Partners: NextGen, Young Invincibles, Savi

Concept #1: Identifying Distressed Borrowers

The first concept was the development of an interactive dashboard13 to identify and target borrowers who would benefit from IDR plans, particularly Black and Latinx borrowers.14

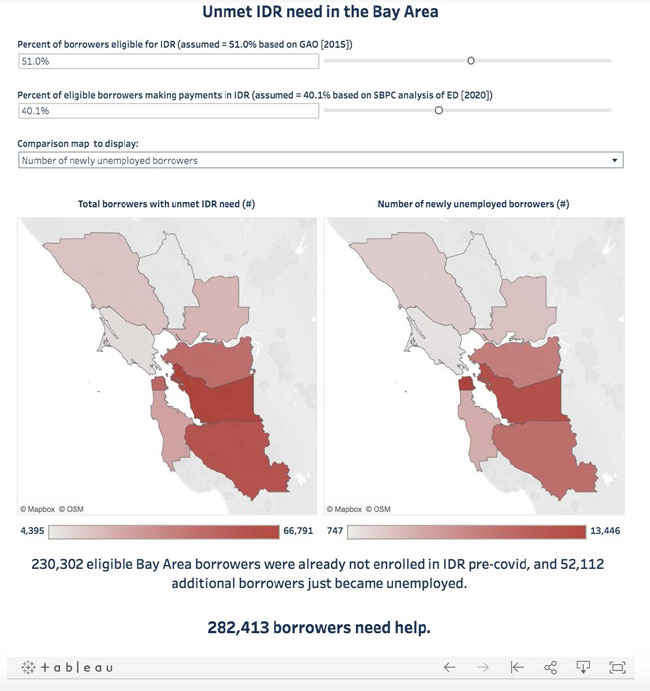

Figure 2

Interactive Dashboard of Unmet Income-Driven Repayment Plan Need in the San Francisco Bay Area

This concept was led by SBPC, in partnership with the city of San Francisco’s Office of Financial Empowerment (SF OFE). By bringing together data on borrower distress, unemployment, demographics, and economic status, SBPC and SF OFE identified over 280,000 borrowers in the Bay Area who are eligible for, but not currently enrolled in, IDR plans. Many of these borrowers are concentrated in some of the Bay Area’s poorest communities and those with higher percentages of Black and Latinx residents.

Armed with this data, SF OFE published an RFI (request for information) in late 2020 seeking a technology vendor that could provide direct-to-borrower assistance in accessing and enrolling in IDR plans. SF OFE is currently evaluating responses to this RFI and is preparing to implement an intervention before the end of the federal student loan forbearance period.

Concept #2: Helping Borrowers Understand and Effectively Navigate Relief Options

The second concept was a public education campaign designed to help borrowers understand the CARES Act and its implications for their student debt obligations and to help borrowers navigate the relief options available to them, including enrollment in IDR plans.

This concept was led by SDC, the nation’s largest student loan advocacy organization. SDC developed relevant content for borrowers15 and organizations that can help reach borrowers,16 then tested content delivery methods and messaging through trusted nonprofit partners NextGen and Young Invincibles. SDC also worked with social impact technology startup Savi to deploy a free, online IDR enrollment tool to eligible borrowers. These outreach efforts resulted in:

- Reaching ~70,000 borrowers via email campaign

- More than 7,000 registrations for student loan repayment workshops, 28 percent of whom identified as Black student loan borrowers

- 460 registrations for the Savi tool, with nearly $20 million total debt managed and more than $1,000 average monthly savings for borrowers once the forbearance period comes to an end

Creating Pathways to Scale

Although the Collaborative was successful in supporting the development of SBPC’s interactive dashboard and SDC’s public education campaign, scaling these interventions will require the active engagement and participation of the broader ecosystem.

SBPC continues to leverage its data and insights to advise state governments and other stakeholders. It is in ongoing discussions with Governor Newsom’s Student Debt Task Force, run by the California Student Aid Commission (CSAC), and along with NextGen and others will help shape a set of recommendations to assist student borrowers, to be published in Fall 2021. SBPC is also working with other cities interested in building local dashboards and exploring how this data-driven approach can apply to other vulnerable populations struggling with student debt. It is actively engaged in conversations with leaders in Boston and Chicago.

SDC continues to evolve its campaign efforts based on borrower feedback and input from its workshop series. Likewise, the Borrower Resource Center and Savi’s eligibility tool continue to see increased traffic and engagement. SDC is currently focused on recruiting additional partners to bring these tools to Black and Latinx borrowers at scale.

The Role of Technology and Policy

It is important for fintechs and nonprofits to understand the policy reforms that could impact their work, and many of them are already playing a role in shaping the policy discussion. Likewise, it is important for policymakers and policy influencers to understand how tech-enabled innovations can complement their efforts to reach diverse communities, as well as the regulatory challenges impeding innovators’ ability to scale. A survey conducted by SDC, for example, found that more than 24 percent of Black borrowers17 did not know that their federal loan payments were paused as part of the CARES Act (compared with less than 19 percent of White borrowers). Although innovations from private and nonprofit groups can help reach some of these borrowers, they alone cannot bring change at the scale required.

The Collaborative organized a convening with our pilot partners, think tanks, and policy experts to discuss the role of technology and policy in helping distressed borrowers and to share insights and learnings from our pilot program. It was widely agreed that policy levers, such as debt cancellation, autoenrollment, and recertification of IDR plans, could eliminate or lessen many of the obstacles hindering access to debt relief among vulnerable borrowers.

Even at relatively small amounts, debt cancellation could help massive numbers of borrowers—over 40 percent of student loan borrowers have less than $10,000 in debt. Although there is much debate as to whether this cancellation should be means-tested or across-the-board, this type of measure would provide much-needed relief to those who need it most.

For borrowers with remaining debt who continue to need relief, enabling autoenrollment in and recertification of IDR plans could dramatically improve access and utilization of such relief programs. Regarding autoenrollment, the IRS could share income tax information with the Department of Education to identify and target IDR-eligible borrowers more easily. In the case of recertification, unemployed borrowers must verify loss of income by completing a paper-based application. Instead, the IRS and Social Security Administration could consider a data-sharing policy to automatically determine loss of income, which would eliminate one hurdle in the recertification process.18

These types of IDR enhancements would allow innovations from private and nonprofit groups, like those offered by SBPC and SDC, the ability to focus on helping borrowers manage their debt rather than the tactical steps to participate in these IDR plans. We hope these kinds of cross-sector conversations, backed by evidence-based data, will result in a more effective and efficient set of policies and innovations to reach greater numbers of borrowers in need.

Conclusion

To improve financial health for all, business leaders and policymakers must be intentional in their efforts to go beyond macro-level indicators and statistical averages to develop a more nuanced and informed understanding of where disparities lie across individuals and communities. In the case of student loans in the United States, borrowers in the greatest trouble are typically not those with the highest debt, but those who dropped out before they earned a degree. The highest rates of default are among borrowers with less than a $5,000 balance—a disproportionate percentage of whom are people of color.

Although data can help us identify where the most acute need is, our thinking must also be informed by listening to the people whose lives we seek to improve. Our pilot partners, SBPC and SDC, ran workshops with distressed borrowers and partnered with nonprofit organizations to test the relevancy of their approach and messaging campaigns. We are continuing to work with our pilot partners to help them scale their innovations, with a particular focus on Black and Latinx borrowers and communities. Additionally, we are leveraging the insights and learnings gained from these pilots to help inform and engage policymakers who share our goal of better targeting relief measures to borrowers in need.

We know that the challenges facing borrowers will become even more acute as the student loan forbearance period under the CARES Act comes to an end. Through collaboration and cross-ecosystem engagement, we can help create a path toward a better financial future where all people, especially the most vulnerable, have the information, tools, and support they need to be resilient and thrive.

We invite you to reach out to finlab@finhealthnetwork.org if you would like to discuss this topic further, explore collaboration, or bring the resources developed by our pilot partners—SBPC and SDC—to the communities you serve.

The Community Development Innovation Review focuses on bridging the gap between theory and practice, from as many viewpoints as possible. The goal of this journal is to promote cross-sector dialogue around a range of emerging issues and related investments that advance economic resilience and mobility for low- and moderate-income communities and communities of color. The views expressed are those of the authors and do not necessarily represent the views of the Federal Reserve Bank of San Francisco or the Federal Reserve System.

End Notes

1. Village Capital, “Fintech for All: Building a More Equitable Financial Services Sector” (Washington, DC: Village Capital, August 2020).

2. https://finhealthnetwork.org/programs-and-events/financial-health-pulse/

3. Financial Health Network, “Financial Health Pulse” (Chicago, IL: Financial Health Network, November 2020).

4. The Financial Solutions Lab (https://finlab.finhealthnetwork.org/) is a $60 million, 10-year initiative managed by the Financial Health Network in collaboration with founding partner JPMorgan Chase and with support from Prudential Financial. The Financial Solutions Lab’s mission is to cultivate, support, and scale innovative ideas that advance the financial health of low- to moderate-income (LMI) individuals and historically underserved communities. The Financial Solutions Lab focuses on innovative solutions that support populations facing acute and persistent financial health challenges, including communities of color, women, older adults, and people with disabilities.

5. https://finlab.finhealthnetwork.org/financial-health-collaborative/

6. College Board, “Share of Defaulters and Three-Year Default Rates by Loan Balance,” (New York: College Board, 2016), https://trends.collegeboard.org/student-aid/figures-tables/share-defaulters-and-three-year-default-rates-loan-balance.

7. Laura Sullivan et al., “Stalling Dreams: How Student Debt Is Disrupting Life Chances and Widening the Racial Wealth Gap” (Waltham, MA: Institute on Asset and Social Policy (IASP), Brandeis University, September 2019), https://heller.brandeis.edu/iasp/pdfs/racial-wealth-equity/racial-wealth-gap/stallingdreams-how-student-debt-is-disrupting-lifechances.pdf.

8. Jason Delisle, “Fixing the Student Loan Safety Net” (Washington, DC: American Enterprise Institute (AEI), 2021), https://www.aei.org/op-eds/fixing-the-student-loan-safety-net/.

9. Diana Farrell et al., “Student Loan Debt: Who is Paying it Down?” (JPMorgan Chase & Co. Institute, October 2020), https://www.jpmorganchase.com/content/dam/jpmc/jpmorgan-chase-and-co/institute/pdf/household-debt-student-loan-debt.pdf.

10. Sara Goldrick-Rab, “Edquity Emergency Aid Primer” (Brooklyn, NY: Edquity, 2019), https://uploads-ssl.webflow.com/5e56bab4a602182939defee3/5eb3865b8cf2c610cd112590_EA Primer.pdf.

11. https://protectborrowers.org/

12. https://studentdebtcrisis.org/

13. https://protectborrowers.org/bay-area-borrowers/

14. Financial Solutions Lab, “Driving Cross-Sector Solutions: Responding to the Unemployment and Student Loan Crises.” Blog (Chicago, IL: Financial Solutions Lab, December 15, 2020), https://finlab.finhealthnetwork.org/driving-cross-sector-solutions-responding-to-the-unemployment-and-student-loan-crises/.

15. https://sites.google.com/studentdebtcrisis.org/borrower-resource-center

16. https://docs.google.com/document/d/1DF8R2A-CtMypN8g98J9yEsSCmHlI9U8bvHyypLEc0VE/edit#heading=h.q9tiqzraayok

17. https://studentdebtcrisis.org/student-debt-covid-survey/

18. Financial Solutions Lab Blog, “Two Ways Policy and Technology Can Support Struggling Student Loan Borrowers.” Blog (Chicago, IL: Financial Solutions Lab, March 2, 2021).