In 2014, Jimmy Chen,1 a software engineer, set out to apply for food stamps. He visited the Human Resources Administration office in Brooklyn, NY. He joined the line of people waiting to meet a caseworker and fill out the same application. Jimmy noticed that people were doing what most of us do when we have an hour to wait—they were on their smartphones, killing time. Here was a tool that most everyone had and could do what they were waiting in line to complete with the caseworker. The problem wasn’t a hardware one (most low-income Americans have a smartphone)2 but a software one. Why weren’t technology companies building the tools to solve this problem?

Low-income Americans face a dozen indignities and inconveniences a day—substandard housing, poor transportation options, and low-wage jobs, not to mention the fees, fines, and penalties that tax those trying to stretch their funds until the next paycheck. Unfortunately, the social safety net is often no different. With strict work requirements, severe penalties for any misstep, and multistep application and recertification processes, accessing the social safety net is far from easy. This reality is further compounded by the structural racism threaded through the social safety net, which results in Black Americans being concentrated in states with less generous welfare programs,3 and more Black and Latinx Americans have not received the three Economic Impact Payments (“stimulus payments”) in a timely manner, or at all.4

Although the civic tech movement—made up of technology-oriented nonprofits, govtech companies, and the many state and local innovation teams that have sprung up around the country—is tackling the cumbersome application process, as well as making it easier for Americans in need to stay on benefits programs, little attention has been given to the experience of making the most of government benefits once a person has been accepted to a program.5

Customer experience matters enormously for households that face severe financial and time constraints. But while wealthier households have an array of services and products to manage their financial lives, there are few options for households with limited income managing complex financial lives that include government benefits issued through specialized cards and payment systems. However, there are tangible, practical, and achievable ways to ease this inequity.

Modernizing the experience of using government benefits does not have to require a lengthy and expensive system overhaul. The technology powering the many apps that aggregate financial data, with customer authorization, to help reach financial goals or simply provide a more specialized experience than a bank or credit card company can be applied to support low-income households. These households arguably manage more complex financial lives—crossing cash, government benefits, and limited budgets—but the practice is not widespread.

Some of the best customer service solutions come through specialization and choice. But most government benefits service systems must be one-size-fits-all—to serve everyone. By inviting innovation and new players in the government benefits system, these optional supplemental services can build on the strong foundation of government supports and layer on higher levels of customer experience through a specialization that isn’t possible for a government agency or contractor. By bringing additional resources, time, funding, and expertise, these technology companies can immediately modernize the client experience of using government benefits without having to overhaul the system.

This paper will explore the potential of a tech-enabled social safety net to improve the experiences of government program beneficiaries, as well as common concerns with this approach through the example of SNAP (the Supplemental Nutrition Assistance Program, or “food stamps”) and the Fresh EBT app.6

Bringing SNAP Customer Experience into the 21st Century

Diana7 is a mother to seven grown children and grandmother to 19. She works part-time as a housekeeper and the rest of the time provides “daycare” for her family. She and her retired husband have been receiving SNAP, in different amounts (depending on how much she’s working), for the past five or six years. One day she saw her daughter checking her SNAP benefits balance through an app called Fresh EBT. Diana was used to calling the 1-800 number on the back of her EBT card and going through an automated phone system to hear her SNAP balance. With the app, where she could check her balance at any time, it was a relief to not have to call and “sit there and listen to all the blah blah blah and punch in all the numbers and just sit there.” Diana now uses the app at least five or six times a week. Sometimes her husband asks how much they have left, and since an accident has left her with short-term memory loss, she just opens the app to tell him. She always checks her balance before going to the store, and as she’s leaving, to make sure the transaction went through and that she’s budgeting for the month. In addition to the convenience, Diana likes that Fresh EBT doesn’t make her “feel stupid” the way other things online do. (She has tried, unsuccessfully, to use her bank’s mobile app.)

SNAP is the country’s most important anti-hunger program, used by over 40 million households.8 It is made possible by the federal government, state governments, grocery retailers, and the private companies that provide the EBT (electronic benefits transfer) system. The federal government creates the overarching program rules, states implement them, and private companies create and distribute EBT cards to individuals, who then spend those benefits at grocery retailers. The current system is successful because it brings together different parties to carry out different functions, out of a recognition that each specializes in its part of the program (e.g., grocery stores are better retailers than the government).9

In 2015, Propel,10 a social enterprise that builds software products for low-income Americans, created the Fresh EBT app11 to modernize the SNAP experience. Fresh EBT allows EBT cardholders to view their SNAP balance at any time, in addition to helping them manage their benefits through tracking transactions, saving via coupons, and earning money through job postings. Fresh EBT is available for free in all 50 states and has grown to reach over 5 million people every month, which is about one in five SNAP recipients. Fresh EBT generates revenue via the coupons and job postings within the app.

It really helps to be able to quickly check my balance while I’m in the store. The phone call method is harder to do in a noisy store, and if I turn up the call volume, others can overhear my call.

– Trina, Wyoming

Fresh EBT facilitates balance checking through consumer-authorized access. Much like third-party finance apps, it obtains a user’s consent to log into another system (in this case, EBT portals) and pull information, which is then displayed in the app. When users open the Fresh EBT app on their phone, the app initiates a request directly to the processor’s portal on their behalf. Authentication is conducted through the same method used by the portal, which is often a username and password passed fully encrypted to the portal and back. No personal user data used to log into the system is saved by Fresh EBT or stored on its servers.

How Households Use Fresh EBT

As Diana’s story illustrates, being able to view your SNAP benefits balance whenever you want, with transaction history, is a huge improvement from the existing method of calling a 1-800 number. Despite the inconvenience of the phone call method, Propel found during early research that this is likely the most called number in the country.

Because Fresh EBT makes it easier, households check their EBT balance more frequently, often before and after every shopping trip, as Diana does. And as a result, benefits last longer. Research conducted since Fresh EBT launched found that the app helps users extend the length of time their benefits last.12 Even just making benefits last one or two more days is impactful when 80 percent of users spend their benefits within nine days.13

Using this app helps people feel not so embarrassed… the app gives confidentiality, something the government strives for.

– Anna, Illinois

An Emergency Response Tool

Fresh EBT has also proved to be easily adapted to a variety of contingencies because it is a trusted source of information for millions of households, and households visit Fresh EBT several times each month. As a smartphone-based service, it can respond quickly and meet people where they are—on their phones—to share information and new programs, often in partnership with nonprofits and other stakeholders.

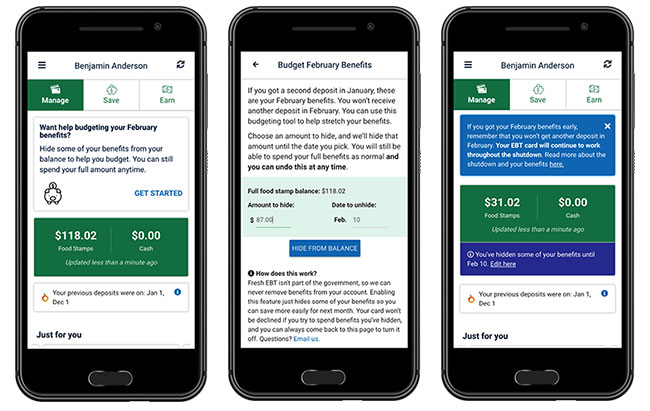

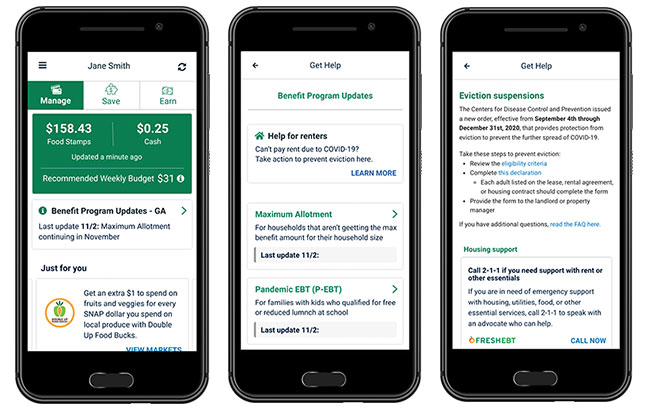

In 2019, when the government shutdown resulted in EBT cardholders receiving two months of benefits at once, Fresh EBT quickly created a “vault” that allowed users to hide a certain amount of their benefits balance, helping them make their funds last.14 When the COVID-19 pandemic led to new or expanded benefits programs, Fresh EBT created a feature to communicate these changes to users directly in the app. The “Benefits Update Center” has become Fresh EBT’s most used feature and expanded beyond just communicating information to connecting users to the actions necessary to access new benefits and protections. For example, over 41,000 Fresh EBT users submitted the declaration necessary to take advantage of the federal eviction moratorium via a partnership with the Kentucky Equal Justice Center, and 3.5 million connected with the non-filer tax form to access the Economic Impact Payments (“stimulus checks”).

Figure 1

The “vault” tool created by Propel to help Fresh EBT users during the 2019 government shutdown.

Figure 2

The Benefits Update Center created by Propel during the COVID-19 pandemic to help Fresh EBT users understand and access new protections and benefits.

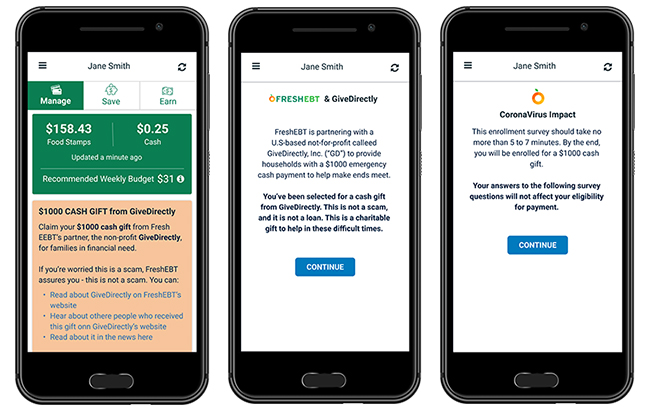

Perhaps the most powerful example is when Fresh EBT partnered with GiveDirectly, a nonprofit organization specializing in cash transfer programs, in March 2020 to distribute $1,000 in no-strings-attached cash assistance to households across the country. Fresh EBT knew that its user base, already living in a state of constant financial precarity, needed aid fast—faster than the government could stand up a program to help. The first payments to users were disbursed on March 22. This initiative, called Project 100+, has since become the largest private cash transfer program in the United States, distributing over $140 million in cash assistance to date.15

Figure 3

The partnership between Propel and GiveDirectly that gives randomly selected Fresh EBT users $1,000 cash transfers.

The Stakes Are Higher for Social Safety Net Programs

These innovations are just a fraction of the changes that could be achieved by the entry of additional technology companies to the social safety net space. However, helping individuals manage their government benefits is fundamentally different from managing a bank account or other financial asset. The subset of individuals who receive these benefits are more financially vulnerable than the broader population. Getting their benefits balance wrong or contributing to the loss (even temporarily) of benefits constitutes an enormous loss that can have a ripple effect in their financial lives. Establishing guardrails is necessary to promote growth in this field in a responsible way.

Propel has learned lessons from its experience building out the first of these tools. First, connecting to this subset of households is a privilege. For Propel, this means that Fresh EBT is not an open advertising platform, unlike other tech platforms. All offers and job opportunities that appear in the Fresh EBT app must meet one requirement: they must provide a clear benefit to Fresh EBT users with minimum risk. This is not driven by paternalism—government beneficiaries are no less savvy than any other consumers—but because it is much harder for them to absorb any financial loss. It is also a mutually reinforcing approach in which Fresh EBT provides only ads and opportunities that are valuable to users, which, in turn, creates continued use and growth of the app.

Second, any product that accesses or aggregates the user’s information should always do so through consumer-authorized access in real time. This means users should authorize the service through a transparent, clear, and well-designed interface that allows for real-time informed consent to pull the information.

Finally, data security and privacy must be the top priority. This doesn’t just mean using best-in-class security practices, but also collecting the minimum information needed to provide the service and storing even less information.

The proliferation of consumer-authorized financial apps today is a result of the Consumer Financial Protection Bureau developing guiding principles for the financial sector in 2017.16 These principles established the value of consumers’ right to access their information through the platform of their choice, to best serve their financial needs. Consumer-permissioned data access is arguably even more important in government benefits programs because consumers cannot simply exit the program and move to an alternative provider. Having more access to their balance and transaction information gives consumers a choice in deciding how to experience the program.

Inviting private companies to bring more innovation to government benefits might result in valuable services, but it also carries the threat of opening the field to bad actors. Although this is a real concern, it can be mitigated by establishing good guiding principles for the field. In addition, predatory practices often arise, even with the most stringent regulations, when there are no high-quality services available to meet a need.17 This is often not mitigated by building higher barriers to access, but rather by inviting and encouraging more high-quality ones. It is important to create an environment where good alternatives can thrive, giving low-income Americans many options. This can crowd out predatory behavior, not least when information about services is easily accessible through public rating and accountability systems, like those in the app stores.

Technological Innovation Is Not a Silver Bullet

Tech-driven innovation is not a panacea for all government program shortcomings. Stakeholders have long identified, and advocated to close, the gaps in some of these programs and to overhaul others in order to create more equitable access for racial minorities across the social safety net. These are changes that need to happen at a federal government level and will take great political capital and time. However, tech-driven innovation can create small improvements to the imperfect system millions of Americans have to live with now.

Twenty years ago, the government introduced the electronic benefits transfer card (EBT card) to reduce consumer stigma by aligning the government benefits experience with private-sector payment options. Government program beneficiaries no longer had to use physical food stamps at the grocery store—they could pay with a card, like other customers. A new public-private partnership could help usher in the next leap forward in the government benefits customer experience—one in which the government provides a robust and healthy social safety net, available and accessible to all, and private companies enhance those services by offering more choice and personalized services. The proliferation of partnerships like this could make a significant difference in the day-to-day experience of managing and using benefits and the day-to-day lives for millions of Americans across the country.

The Community Development Innovation Review focuses on bridging the gap between theory and practice, from as many viewpoints as possible. The goal of this journal is to promote cross-sector dialogue around a range of emerging issues and related investments that advance economic resilience and mobility for low- and moderate-income communities and communities of color. The views expressed are those of the authors and do not necessarily represent the views of the Federal Reserve Bank of San Francisco or the Federal Reserve System.

End Notes

1. Jimmy Chen went on to found Propel, the makers of Providers (formerly Fresh EBT).

2. Monica Anderson and Madhumitha Kumar, “Digital divide persists even as lower-income Americans make gains in tech adoption” (Washington, DC: Pew Research Center, May 2019), https://www.pewresearch.org/fact-tank/2019/05/07/digital-divide-persists-even-as-lower-income-americans-make-gains-in-tech-adoption/.

3. Heather Hahn et al., “Why Does Cash Welfare Depend on Where You Live?” (Washington, DC: Urban Institute, June 2017), https://www.urban.org/research/publication/why-does-cash-welfare-depend-where-you-live.

4. Among Fresh EBT users, 19 percent of Latinx and 15 percent of Black households report not receiving a single Economic Impact Payment, while 11 percent of white users report the same. For an analysis on the racial disparities in Economic Impact Payment receipt among Fresh EBT users of Color, see “The COVID-19 Pandemic Hit Fresh EBT Users Harder,” Propel, May 6, 2021; https://www.joinpropel.com/indepth-racial-disparity.

5. For example, nonprofit Code for America created Get Cal Fresh (https://www.getcalfresh.org/), an online application system for California’s SNAP program (Supplemental Nutrition Assistance Program, or “food stamps”). Get Cal Fresh is mobile and desktop-friendly, reduces a process that took approximately 45 minutes to eight minutes, and integrates text-message confirmation and reminders. Nava, a public benefits corporation, has partnered with state and federal partners to improve a number of programs (see https://www.navapbc.com/services/case-studies/), including Medicare and Medicaid. Individual state and local governments have also improved their own program access and delivery—for example, New Jersey’s Office of Innovation created a user-friendly unemployment benefits tool to reduce complexity in unemployment benefits during the COVID-19 pandemic (https://getstarted.nj.gov/labor/).

6. In July 2021, Propel launched Providers, a new app that replaced Fresh EBT. Providers builds on the core functionality of Fresh EBT, EBT card balance checking, and adds a free debit account so users can manage their whole financial lives in one place. Providers is the only app where users can manage government benefits and debit/banking side-by-side.

7. Real Fresh EBT user interview; name has been changed.

8. See the Center on Budget and Policy Priorities’ SNAP Chart Book for more details on the impact, reach, and current utilization of SNAP, https://www.cbpp.org/research/food-assistance/chart-book-snap-helps-struggling-families-put-food-on-the-table.

9. Heather Hahn et al., “Access for All: Innovation for Equitable SNAP Delivery” (Washington, DC: Urban Institute, June 2020), https://www.urban.org/sites/default/files/publication/102399/access-for-all-innovation-for-equitable-snap-delivery_0.pdf.

12. Andrew Hillis, “Salience through Information Technology: The Effect of Balance Availability on the Smoothing of SNAP Benefits” Harvard Business School Working Paper, No. 18-038, October 2017, https://www.hbs.edu/faculty/Pages/download.aspx?name=18-038.pdf.

13. Wendy De la Rosa and Joanne Yeh, “Managing SNAP (Food Stamps) Efficiently” (Durham, NC: Center for Advanced Hindsight, 2016), https://advanced-hindsight.com/archive/wp-content/uploads/2015/11/propel_case.pdf .

14. The benefits “hidden” by this feature were still completely available for use at any time, just simply not reflected in the current balance displayed in the app.

15. Read more about Project 100+, including the impact on recipients in their own words, at www.givedirectly.org/covid-19/us/.

16. “Consumer Protection Principles: Consumer-Authorized Financial Data Sharing and Aggregation,” Consumer Financial Protection Bureau, October 2017, https://files.consumerfinance.gov/f/documents/cfpb_consumer-protection-principles_data-aggregation.pdf. For more information on the ongoing challenges related to consumer-authorized financial apps, see Rebecca Ayers and Suman Bhattacharyya, “Why screen scraping still rules the roost on data connectivity,” Fin Ledger, March 20, 2021, https://finledger.com/2021/03/10/why-screen-scraping-still-rules-the-roost-on-data-connectivity/.

17. For more on the persistence of payday lending, see Bethany McLean, “Payday Lending: Will Anything Better Replace It?” The Atlantic, May 2016, https://www.theatlantic.com/magazine/archive/2016/05/payday-lending/476403/.