Homeownership, although far from universal, forms a central part of what might

be called a national ethos, in which owning one’s own home is associated with

middle-class status and the American dream achieved.1

Yet, a recent article by

Ryan Cooper bore the grandiose title “It’s Time to Kill the American Dream

of Homeownership.”2

Whether homeownership is or is not a good investment for a middleclass

family is not the issue here, although there is a compelling case that it still is.3

The

question this chapter will attempt to answer is a different one; namely, what role does homeownership

play in the vitality of middle neighborhoods in legacy cities?

This question is particularly timely for a number of reasons. First, as Cooper noted,

many support the proposition that homeownership is overrated or irrelevant, or, in the

recent words of a respected colleague, “it’s time to get over homeownership.” Second, the

years since the bursting of the housing bubble in 2006 and 2007 have shown not only a

widely reported decline in homeownership rates nationally, but a significantly greater decline

in homeownership rates—and in the absolute number of homeowners—in legacy cities.

If a relatively high level of homeownership is indeed an important factor in fostering

neighborhood stability, a different phenomenon—a growing number of single-family homes

purchased by absentee investors—should be a source of considerable concern to those who

care about the future of middle neighborhoods. My case for this proposition is circumstantial;

homeownership is interwoven with many other factors affecting neighborhoods, and,

as I will discuss, the pathways by which it affects neighborhood vitality are complex and

multifaceted.4

At the same time, I would argue that the case is strong, and that homeownership

should be at the forefront of policies and strategies to stabilize or revive urban middle

neighborhoods.

At the same time, it is important to stress that arguing for the value of homeownership

does not imply that rental housing is unnecessary or that renters are in some fashion

second-class citizens and cannot contribute to their neighborhoods. Rental housing is

a vital part of any community, particularly those with large numbers of lower-income

families for whom homeownership may not be a realistic or desirable alternative. While

maintaining a high homeownership rate may be a desirable public policy, policies that

focus on homeowners and fail to address both the importance of a sound rental housing

stock and engaging renters fully in their communities are as unbalanced as strategies that

ignore homeownership entirely.

This chapter is in four sections. The first provides a brief historical introduction to

homeownership in middle neighborhoods, while the second discusses the research evidence

for the neighborhood effects of homeownership and explores some of the pathways

by which those effects are experienced. The third describes the erosion of homeownership

in legacy cities and their neighborhoods, including a case study of Trenton, New Jersey,

where I have been able to use a unique neighborhood-level data set showing the trends in

owner-occupant and investor home purchases from 2006 through 2013. The final sections

explore the features of a model that links different homeownership effects to neighborhood

change and suggest some policy implications for middle neighborhoods.

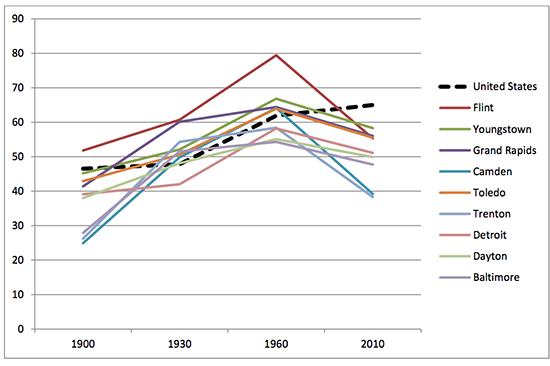

The Historical Background

The middle neighborhoods of legacy cities were developed beginning in the late

nineteenth century through the early 1960s. They were historically, and remain today with

few exceptions, neighborhoods of single-family homes.5

In Camden, Baltimore, and many

coastal cities, these homes were row houses, while in Toledo, Detroit, and most inland

cities; they were detached houses on small, usually narrow, lots. Homeownership rates in

legacy cities from 1920 on were often comparable to or higher than the national homeownership

rate (Table 1). By 1930, one-half or more of the single-family houses in most of these

cities were owner-occupied.

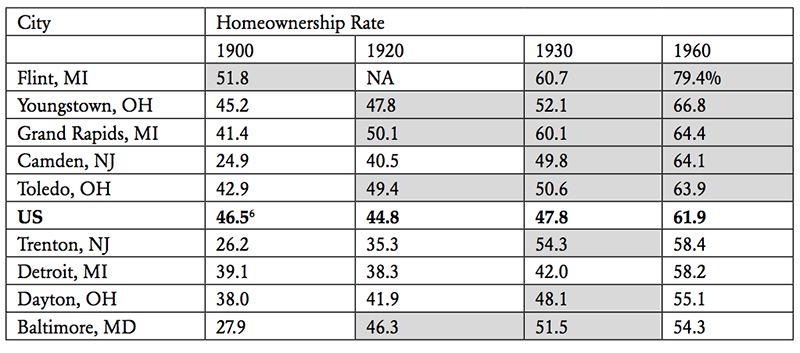

Table 1

Homeownership Rates in Select Legacy Cities, 1900–1960

Source: 1900, 1920, 1930, and 1960 Census of Housing, U.S. Bureau of the Census.

Homeownership rates in the cities in Table 1 grew at a far more rapid pace than the

national average from 1900 to the Great Depression and World War II in the 1930s and

1940s, and homeownership was common in urban areas well before the reforms of the New Deal. Between 1900 and 1930, the number of homeowners in Baltimore more than tripled,

to 97,000, while the number of renters grew much more modestly, from 70,000 to 92,000.

The number of Trenton homeowners also more than tripled, to nearly 15,000, while the

number of renters increased by fewer than 2,000. In both cities, the character of the housing

stock, mainly single-family row houses, did not change materially. In all likelihood,

what was happening was that many rented houses became owner-occupied and that the

majority of the new houses built were sold to homebuyers rather than absentee landlords.

Homeownership growth in many cities did not end with the Depression. A number

of cities, including most notably Toledo and Detroit in Table 1, saw dramatic increases in

homeownership following World War II. Between 1930 and 1960, the number of homeowners

in Detroit doubled, to 299,000, while the number of renters barely grew, from

211,000 to 215,000. Clearly, and contrary to widespread belief, the increase in homeownership

during the immediate postwar period was not a purely suburban phenomenon.

Although data do not exist to enable one to zoom in on particular neighborhoods in

these cities, it is reasonable to assume that middle neighborhoods, being inhabited largely

by middle-income families and occupying the middle of the local housing market, had

homeownership rates similar to or higher than those shown in Table 1, and that well before

World War II, homeownership was already a central element in the character of the typical

urban middle neighborhood. As I suggest, both here and in the previous essay in this volume,

the recent drastic drop in homeownership in many of these neighborhoods has been

a significant factor in their decline.

Neighborhood Effects of Homeownership

With homeownership looming so large in the American ethos, it is not surprising that

an extensive body of research exists on its effects, whether in terms of wealth-building, behavior

and family outcomes, or neighborhood conditions and dynamics. In this section, I

summarize the research findings in five separate areas: residential stability, property values,

property condition, social/behavioral factors, and social capital and collective efficacy.

All of this research shares the problem of how to isolate homeownership from other

social and economic factors. Although the research, particularly more recent work, typically

tries to control for socioeconomic differences between owners and renters, such as income

or race, it is more difficult to pin down the extent to which homeownership is affected by

self-selection; in other words, whether people who choose to become homeowners have

different attitudes or values than people of similar social and economic status who choose

not to become homeowners. This may in turn affect their behavior and their effect on their

surroundings.7

Although this does not affect the relationship between homeownership and whatever

neighborhood feature one is trying to measure, such as stability or civic engagement, it

means that one can never be completely certain that one is measuring the effect of homeownership or the effect of some other social factor that is, in turn, linked to homeownership.

For that reason, the nature of the pathways through which homeownership exerts its

influence, which I address later, becomes particularly important.

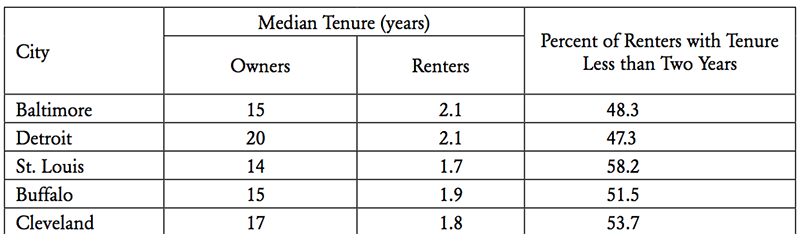

Residential Stability

Residential stability in legacy city middle neighborhoods is declining as homeownership

declines. Residential stability or turnover appears to be an important element in

neighborhood health, with high turnover or “churning” seen as a factor leading to decline8.

Homeownership is statistically associated with greater length of tenure; the 2013 American

Community Survey finds that the median length of residence for homeowners in their

current home is 11 years. This compares with fewer than three years for tenants. The tenure

gap is even greater in legacy cities, as shown in Table 2.

Table 2

Average Tenure for Owners and Renters in Select Legacy Cities

Source: 1 year 2012 American Community Survey

Analysts have raised the question of how to separate the impact of homeownership

as such from the impact of long-term tenure stability (National Association of Realtors

2006). Some research has found that the effect of homeownership on child outcomes drops

significantly when controlling for mobility9

. Thus, in theory, one might be able to achieve

outcomes similar to those associated with homeownership by stabilizing the tenure of renters

or by fostering intermediate forms of tenure, such as rental with tenure rights or share

appreciation, as exist in some European countries.

In practice, though, this may not be a realistic option. First, evidence is strong that

homeownership improves residential stability independent of other socioeconomic factors10.

This may be a function of the greater transaction costs for homeowners associated

with moving or it may reflect some of the value or attitudinal changes associated with

homeownership, as noted earlier. Second, the magnitude of the tenure gap between owners

and renters is so great that it is hard, if not impossible, to conceive of a plausible strategy

that would eliminate it. Although some advocates have suggested that a landlord-tenant regime that incorporates security of tenure and rent control would have such an effect, the

experience in New Jersey, where security of tenure is enshrined in state law and rent control

is legal and widely used, does not support that proposition.11 Increasing tenants’ tenure

through legal and economic strategies is a desirable policy objective. It would almost certainly

yield significant benefits for tenants and may also yield some potential community

benefit. However, it is unlikely in the extreme to be able to substitute for homeownership

as a means of fostering neighborhood stability.

It is not enough to encourage families to become homeowners. It is equally or more

important to ensure that they become stable, long-term homeowners, and that they do not

involuntarily lose their homes through foreclosure, tax delinquency, or other controllable

factors12. There is abundant evidence that involuntary loss of homes is severely destructive

to both the homeowners and their neighborhoods, potentially exceeding whatever benefits

were gained by becoming homeowners in the first place.13

Property Values

The value or sales prices of homes in a neighborhood is arguably the single most direct

measure of the economic vitality of a neighborhood. Rising property values are a direct

indicator of positive economic change in a neighborhood, and declining values equally

directly measure negative change. Because homeowners tend to have higher incomes than

renters, it stands to reason that property values would be higher in areas with high homeownership

levels. There is considerable evidence, however, that, independently of income,

homeownership and property values bear a strong relationship to each other.

A number of studies have found that newly constructed, subsidized housing for

owner-occupancy increases the value of nearby homes.14 Although these effects may have

as much to do with the replacement of vacant lots or derelict buildings, research has found

significant price increases with increases in homeownership rates, even after systematically

controlling for both neighborhood and individual characteristics.15 Chengri Ding and

Gerrit-Jan Knaap have looked at the converse, finding that the loss of homeowners from

Cleveland neighborhoods reduced property values in those areas.16 William Rohe and

Leslie Stewart have found that the relationship works in reverse as well; healthy property

value appreciation triggers greater homeownership.17 This last point offers insight into an

important aspect of the pathways that drive neighborhood effects, the process by which

households decide where to buy homes.

Property Maintenance and Condition

The condition and maintenance of properties are important elements in a neighborhood’s

stability and health. Although research finds a strong relation between homeownership

and property maintenance and condition, it also finds that the relationship is contingent,

in the sense that homeowners’ maintenance decisions are strongly influenced by

other neighborhood features. Both George Galster18 and Yannis Ioannides19 found that the level of social interaction and social cohesion in a neighborhood significantly influences

property upkeep. Put differently, a homeowner’s maintenance and investment decisions

are influenced by neighborhood expectations and by what he or she sees neighbors doing.

Their findings suggest a possible link between homeownership, property upkeep, and collective

efficacy. This would be a fruitful area for further research.

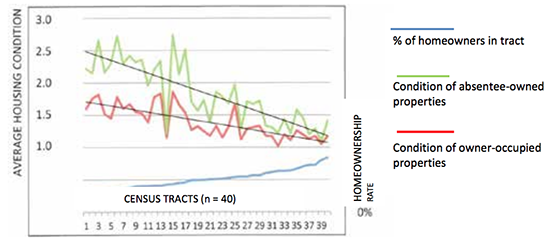

Who owns the home is also important. My research in Las Vegas found a significant

difference in property conditions between owner-occupied and absentee-owned properties

within the same block or neighborhood20. Figure 3 illustrates the difference in property

conditions in Flint, Michigan, for owner-occupied and absentee-owned properties, as well

as the effect of higher homeownership rates on the condition of rental properties21 The

census tracts shown along the X (horizontal) axis in Figure 3 are organized in order of

homeownership rate from low to high. The Y-axis shows the average condition score for

properties, using a 4-point scale in which properties in good to excellent condition were

scored 1, and dilapidated properties scored 4.

Figure 1

Tenure and Property Condition by Census Tract in Flint Michigan

housing condition) and Genesee County Property Records (homeowner/absentee owner distribution).

Figure 1 support the research findings that neighborhood peer behavior plays a major

role in driving maintenance decisions. The higher the homeownership rate, the better

properties are maintained and the better their condition. At every point on the continuum,

moreover, owner-occupied properties are better maintained than absentee-owned properties,

with the quality gap largest in areas where homeownership rates are lowest.

At the same time, one should not infer that the effects seen in Figure 1 are necessarily

caused by higher homeownership rates. Higher homeownership rates are associated with

higher incomes and higher property values, and it is likely that these effects are the result of

the interplay between these (and perhaps other) factors.

Mortgage Foreclosure and Tax Delinquency

A number of studies have found that absentee owners are more likely than owneroccupants

to allow their properties to go into mortgage foreclosure. Richard Todd, who

studied Cuyahoga County, Ohio, early in the foreclosure crisis found that nearly three times

as many non-occupant owners in Cuyahoga County had a foreclosure notice filed on their

mortgage by April 30, 2008, than owner-occupants (28 percent vs. 9 percent)22. Even when

controlling for such factors as income, borrower’s race, and neighborhood housing values,

the foreclosure rate on mortgages to non-occupants was at least double that of owner-occupied

mortgages. Other research found that the disparity between foreclosure rates for owneroccupants

and absentee owners was significantly greater in the midwestern states where

legacy cities are typically located than in Sunbelt states such as Nevada and Florida.23

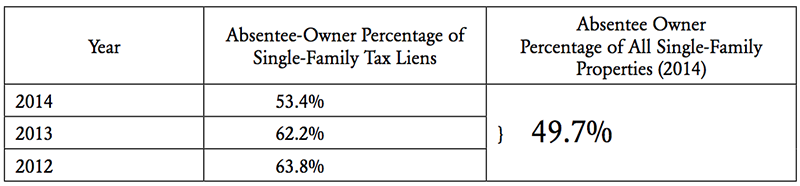

Little or no published research exists on the relationship between homeownership and

tax delinquency, although logic would suggest that the same disparities apply. My work

in Trenton, New Jersey, supports that proposition. I was able to use parcel-level data to

compare tax delinquency and redemption rates for owner-occupants and absentee owners

of single-family homes (Table 3).

Table 3

Percentage of Absentee Owner Properties with

Tax Liens on File in 2014 in Trenton, New Jersey

Table 3 suggests that although the likelihood of early tax delinquency is only moderately

greater for absentee owners (+15 percent), the likelihood of long-term delinquency—

reflected in the failure to redeem 2012 and 2013 tax liens as of late 2014—is significantly

greater (+65-75 percent) for absentee owners than for owner-occupants.

Social and Behavioral Conditions

Many studies find a strong connection between homeownership and different family

social or behavioral conditions, and these conditions can affect neighborhood stability

in important ways. Changes in child and youth outcomes may affect crime through

lower drop-out rates, in turn leading to lower juvenile delinquency; or through lower

teen pregnancy rates leading in turn to lower poverty rates in the next generation. These relationships reflect the well-established link between teen pregnancy, single female

parenthood, and poverty. Richard Green and Michelle White found a strong relationship

between homeownership and greater educational attainment, lower dropout rates, and

fewer teen pregnancies.24 Other researchers have found that the children of homeowners are

more likely to achieve higher levels of education and subsequent earnings, controlling for

other relevant social and economic factors affecting educational outcomes and earnings25.

It is likely that a strong feedback chain exists between such behavioral changes at the family

level and neighborhood conditions.

Research also has found that homeownership is associated with better physical and

psychological health26, overall life satisfaction27, and owners’ greater sense of control over

their environments28. The extent, however, to which these factors affect neighborhood

conditions remains uncertain.

It should be stressed that these positive effects are the product of successful homeownership,

reinforcing the point made earlier that public policy should not aim simply to

create homeowners but to foster sustainable homeownership. Homeowners who are delinquent

on their mortgages or mired in foreclosure proceedings suffer from increased stress,

depression, and mental illness29. The possibility should not be dismissed that these psychological

effects contribute to the well-documented powerful negative effects of foreclosure

on neighborhood vitality.

Social Capital and Collective Efficacy

Social capital can be seen as a combination of civic engagement and trust or the extent

to which people feel mutual obligations to one another (Putnam 1993). Kenneth Temkin

and William Rohe studied change in Pittsburgh neighborhoods between 1980 and 1990

and find that “neighborhoods with relatively large amounts of social capital are less likely

to decline when other factors remain constant.”30 A related concept linking social dynamics

to neighborhood change is collective efficacy, or the “social cohesion combined with

shared expectations for social control.”31 This concept echoes a much earlier formulation by

Jane Jacobs, who wrote “a successful neighborhood is a place that keeps sufficiently abreast

of its problems so it is not destroyed by them.”32

Notably, however, “social control,” Sampson, Raudenbush, and Earls write, “should

not be equated with formal regulation or forced conformity by institutions such as the

police and courts. Rather, social control refers generally to the capacity of a group to

regulate its members according to desired principles—to realize collective, as opposed to

forced, goals.”33 They found that collective efficacy is “a robust predictor of lower rates of

violence,” after controlling for neighborhood characteristics.34 Later research has found that

the absence of collective efficacy to be a strong predictor of homicide rates35.

Homeownership is positively associated with social capital. Homeowners are much

more likely to participate in activities that increase neighborhood social capital, such as

volunteering or participating in block group meetings.36 Manturuk, Lindblad and Quercia found similar patterns when looking specifically at the behavior of low- and moderateincome

homeowners37.

Other research has found strong relationships between homeownership, collective efficacy,

and neighborhood crime and disorder38. Lower homeownership, or lower collective

efficacy, are both associated with higher levels of crime and disorder. This relationship is

again subject to the homeowner having a sustainable mortgage. Two European studies also

support the link between homeownership and collective efficacy. A Danish study found

a strong association between greater homeownership and lower crime in a neighborhood,

while controlling for multiple economic and demographic variables39, while a German

study found that homeowners were less willing to accept deviant behavior and more ready

to intervene when they observe such behavior40.

In conclusion, the relationship between homeownership and neighborhood change is

complex and multidimensional, yet it appears clear that increasing stable, sustainable homeownership

can significantly further positive neighborhood change through many different

pathways, while a decline in homeownership is likely associated with neighborhood decline.

The Erosion of Homeownership in Legacy Cities

Although homeownership rates in legacy cities tended to parallel and even exceed national

trends between 1900 and 1960, the trends have sharply diverged since then. In those

cities, homeownership is declining and investor purchases are rising. Given the importance

of homeownership to neighborhood health, as described above, this is a problematic trend.

All of the cities shown initially in Table 1 saw their homeownership rates drop after

1960, in some cases sharply, as in Flint or Camden, and in others more gradually, as in

Toledo or Grand Rapids (Figure 2). Although homeownership rates have declined nationally

in recent years, the long-term national trajectory over that period, as shown in Figure 2,

was upward.

Figure 2

Homeownership Rates in Select Legacy Cities, 1900–2010

Figure 2 is somewhat misleading, however, given that it implies that homeownership

has been declining since 1960 for all of these cities. Instead, many legacy cities saw continued

growth or only modest declines in homeownership rates until the collapse of the

housing bubble in 2007, at which point the rate plummeted. Table 4 shows the trends for a

cluster of large legacy cities.

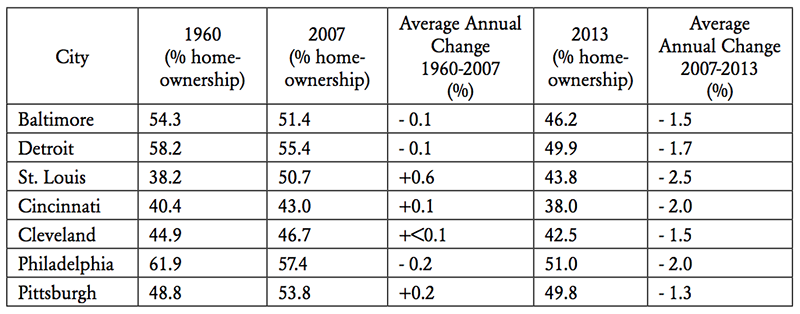

Table 4

Change in Homeownership Rates, Select Cities, 1960–2007 and 2007–2013

had one-year ACS data available for both 1960–2007 and 2007–2013.

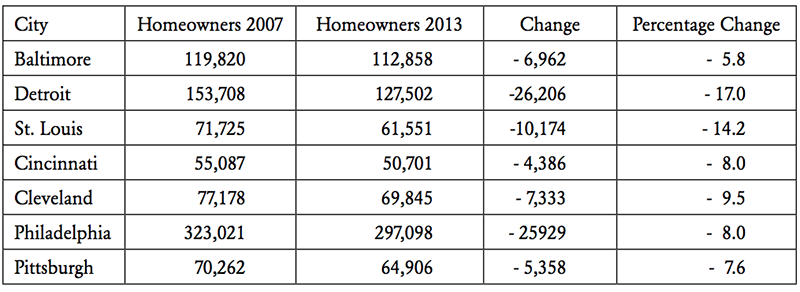

Four of the seven cities in Table 4 saw homeownership growth between 1960 and 2007,

modest in most cases, but substantial in St. Louis. Since 2007, all seven have seen sharp

declines in both homeownership rates and in the number of owner-occupant households

(Table 5). As a whole, these seven cities lost 11 percent of their homeowners, or more than

94,000 homeowner households.

An initial inference might be that the changes in legacy cities are no more than a

reflection of the erosion of homeownership nationally during this period. This is incorrect,

as not only is the rate of decline in these cities more substantial than the national rate of

decline, but the numerical decline is far more substantial, as a percentage of the homeowner

base, than nationally. The number of homeowners in these cities is declining at a rate of

1 percent to nearly 3 percent per year in the case of Detroit.

Table 5

Change in Number of Homeowners, Select Cities, 2007–2013

During this same six-year period, the number of renters increased in each of these cities,

in some cases substantially. Even in Detroit, where the total population continued to

decline precipitously, the number of renters increased by more than 3,000 households.

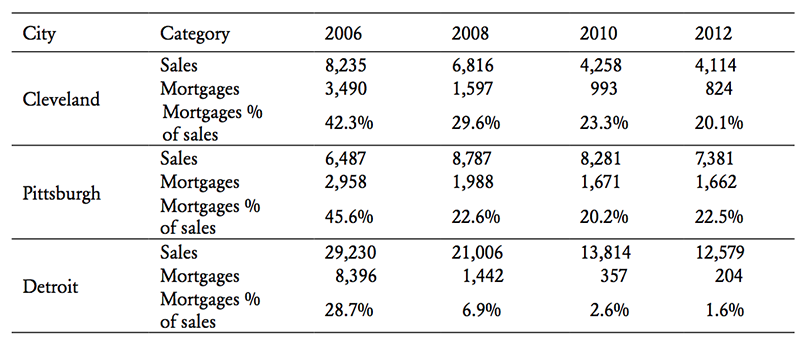

Several factors drive this erosion of homeownership, but one factor is clearly the

increasingly dominant role of investor-buyers in legacy city housing markets. It is hard to

measure this trend with precision, although a comparison of total sales volumes with the

number of purchase mortgages in the same community during the same period can provide

a rough sense of the trajectory of change.41 Table 6 compares sales volumes with purchase

mortgage volumes for three cities between 2006 and 2012. Mortgages declined from 42 percent

of sales in Cleveland in 2006 to 20 percent by 2012, and in Pittsburgh from 46 percent

to 22 percent. In Detroit, where the market collapse was pronounced, mortgages in 2012

represented fewer than 2 percent of total sales.

Table 6

Ratio of Purchase Mortgages to Total Sales, Select Cities, 2006–2012

At the same time, Table 6 makes clear that total sales volumes also dropped significantly,

although to a lesser extent, Pittsburgh, which may have the strongest housing market

among major legacy cities, being an exception. This drop in sales volume reflects the severe

difficulty that would-be homebuyers have in obtaining mortgages in the post-bubble era; a

recent Urban Institute report concluded that “tight credit standards prevented 5.2 million

mortgages between 2009 and 2014”42. Although investors have filled part of the gap in effective

market demand, much remains unfilled, leading to greater property abandonment in

weaker neighborhoods. Moreover, as I have discussed in detail elsewhere, depending on the

underlying market conditions of the neighborhood, investor behavior may have significant

destabilizing effects.43

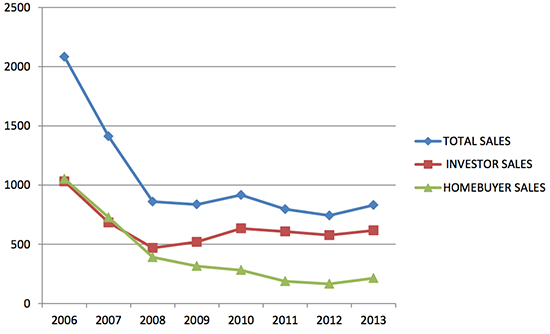

My recent study in Trenton, New Jersey, offers a more detailed picture of increased investor

activity.44 I analyzed individual sales transactions between 2006 and 2013 to identify

investor and homebuyer activity citywide and by neighborhood for each year.45 The trend

shows a pattern consistent with that shown by the comparison of sales and mortgage data.

The number of sales plummeted, with the number of owner-occupant homebuyers declining

from more than 1,000 in 2006 to an average of less than 200 for the past three years

(Figure 3). The number of investors has remained relatively stable since 2007 but at a level

considerably lower than in 2006, the last year of the housing bubble. In 2013, investors represented

nearly 80 percent of all sales in Trenton, compared with 50 percent in 2006.

Figure 3

Sales Transactions by Type of Buyer in Trenton, NJ, 2006–2013

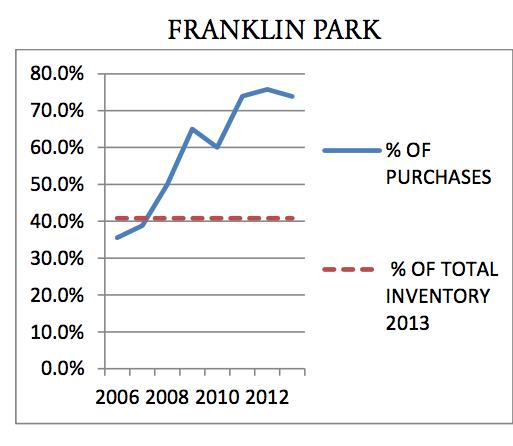

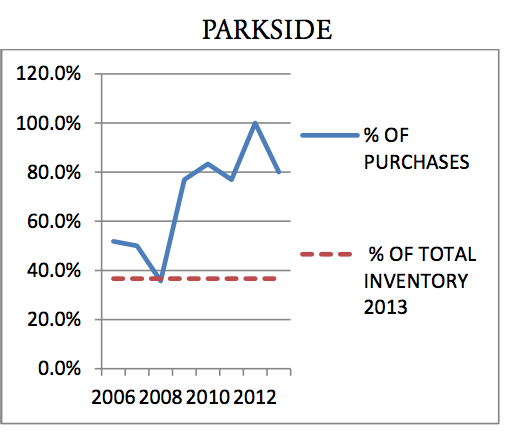

Although in 2006, the percentage of investor buyers was roughly proportional to their

share of the city’s housing stock, by 2013, the investor share was far higher, as illustrated

in Figure 4 for two of the city’s middle neighborhoods. Both of these neighborhoods still

have relatively high homeownership rates (59 percent in Franklin Park and 64 percent in

Parkside). Although investors own only 36 percent of the inventory in Parkside, they have

accounted for 68 percent of the purchases there since 2006 and 86 percent since 2011.

In Franklin Park, investors own 41 percent of the inventory, but they have accounted for

54 percent of the purchases since 2006 and 74 percent since 2011. The rate of erosion in

homeownership in these neighborhoods is likely to be significant.46

Figure 4

Investor Share of Inventory and Purchases, 2006–2013, in Two Trenton Neighborhoods

Modeling the Relationship between Homeownership Erosion and the

Middle Neighborhood

What, then, is the relationship between homeownership erosion and the decline of

so many middle neighborhoods in legacy cities? In the previous essay in this volume, I

presented data showing the extent of that decline, while in this chapter I have tried to make

two points: first, there is a compelling link between homeownership and a host of factors

associated with stable, healthy neighborhoods; and second, decline in both the share and

the number of homeowners in legacy cities and their neighborhoods has accelerated.47

Although the Trenton study finds a very strong relationship between the investor share

of purchases (a reasonable proxy for homeownership erosion) and factors such as median

house price, violent crime rate, or tax foreclosure, all of which are associated with neighborhood

strength and weakness,48 one cannot necessarily conclude that the decline in homeownership

causes neighborhood decline. Nonetheless, there appear to be clear associations

between loss of homeownership and decline, and the findings on neighborhood effects suggest

a number of the pathways for such a relationship. The balance of this section explores

these pathways and suggests a possible model of the relationship between homeownership

and neighborhood change.

In doing so, it is essential to distinguish between those effects that appear to be properties

of homeownership as such, which may be considered primary effects, and those that are the product of those factors, or secondary (or tertiary) effects. For example, even though there appears to be an association between collective efficacy and homeownership, that association

may not be inherent to homeownership in itself, but could be seen as a secondary effect driven by primary features of homeownership, namely the higher level of investment as well as the longer duration of tenure associated with homeownership.

Indeed, stripped to its essence and disregarding the potential of homeownership as

a means of building wealth, there are arguably only two salient features that intrinsically

distinguish homeownership from rental tenure: the significantly longer duration of the

tenure and the fact that homeownership represents a significant financial, and psychological,

investment in a place. The two are closely interwoven. Although the financial investment

may be independent of the duration of tenure, the psychological investment, to the

extent it exists, is likely to be linked to duration of tenure. Duration of tenure, however,

may also be linked to financial investment, if only because of the resulting greater “stickiness”

of homeownership49 and the higher transaction costs associated with selling a home

than renting50.

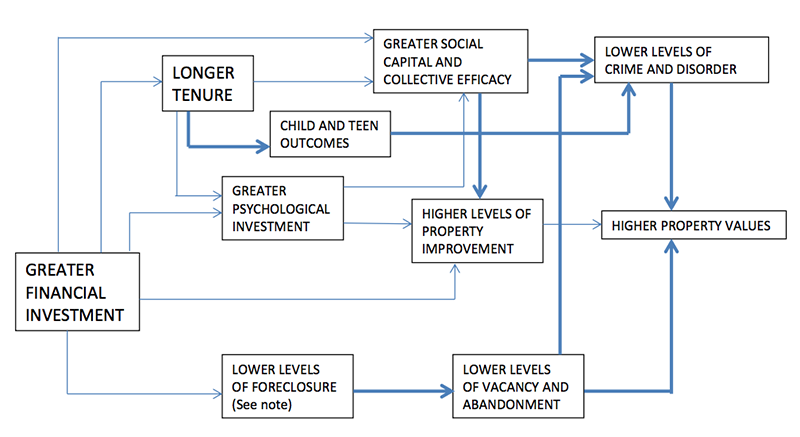

Figure 5 is a conceptual model of the relationship between homeownership and neighborhood

change. The extent to which the specific pathways in the model are supported by

the body of research discussed earlier varies widely. The relationships between collective efficacy

and crime incidence, or between crime and property values, for example, are strongly

supported. The relationship, on the other hand, between length of tenure and collective

efficacy is my hypothesis, drawn by inference from the research, rather than a relationship

that has been explicitly established by research. Relationships that are more strongly

established are shown with bold lines. Although the relationship between homeownership

and foreclosure incidence is reasonably well established, the relationship between the financial

investment in homeownership and foreclosure is inferred from the prior relationship,

rather than being established in itself.

The model suggests a number of different pathways by which a relatively high and

stable homeownership rate is likely to have a positive effect on the vitality of middle

neighborhoods, and by extension, how the erosion of homeownership is likely to sap that

vitality. As tenure shifts from ownership to rental, under the social and economic conditions

affecting those neighborhoods, the neighborhoods are likely to see declines in property

improvement and increased mortgage foreclosure and tax delinquency as direct results

of the tenure shift. Indirectly, the increased residential instability and reduced investment

associated with the erosion of homeownership may in turn lead to reductions in collective

efficacy and child outcomes, which in turn may trigger negative changes in crime incidence

and property values, both of which are significant destabilizing factors.

I am not suggesting that these changes will necessarily take place. There are far more

variables at play than can be suggested by the model, while there is no magic to any particular

homeownership rate. However, it is important to stress that the erosion of homeownership

in legacy city neighborhoods, particularly since the end of the housing bubble, is not

taking place in a social or economic vacuum. It is taking place in the context of a series of

powerful demographic and economic trends, all of which are having the effect of placing

these neighborhoods increasingly at risk of destabilization. In that context, the erosion of

homeownership in legacy cities should be a matter of substantial concern.

Conclusion

As with any complex policy issue, concern does not necessarily offer guidance on

how the issue should be addressed. When it comes to the erosion of homeownership, and

its effect on middle neighborhoods in legacy cities, this is particularly the case, since any

policies to address this particular issue need to be carried out within the context of the

highly problematic widespread decline of middle neighborhoods, which imposes significant

constraints on what may be fasible.

Figure 5

Conceptual Model of Homeownership and Neighborhood Change

This is particularly true with respect to what might be seen as the obvious policy solution;

namely, to encourage more people to become homeowners in middle neighborhoods.

There appear to be severe limitations to what may be possible in this respect. The decline

in the number of middle-income households in general, and the number of married-couple

child-rearing households not only within the cities but also throughout metropolitan

regions, means that the pool from which homebuyers come is a shrinking one. The weak

competitive position of many legacy cities in their regions makes them a hard sell for many

prospective home-buying households. Although some neighborhoods, with distinct locational,

physical or other assets, may, – and should, – become competitive for homebuyers,

it is not likely to be an option available for all struggling middle neighborhoods.

A second approach, which is less often discussed but may have a wider potential reach,

is how better to retain and engage the neighborhood’s present homeowners, many of

whom are not only disengaged but actively fleeing the city for suburban areas.

Slowing their flight and engaging their energies in their neighborhoods are arguably

the two most important steps to stabilize these neighborhoods. However, doing so will

require some combination of both community-building strategies in the neighborhood–

which most probably will depend on the existence of a strong community development

corporation (CDC) or other similar entity—and a responsive municipal government capable

of improving public services and willing to give its residents a strong role in shaping

the destiny of their neighborhoods.

Finally, although this chapter has focused on homeowners, it is important to pay greater

attention to the renter population in middle neighborhoods as well as their landlords.

Both groups have not received the attention their significant neighborhood role deserves,

the former largely ignored and the later often demonized. Both, however, will have a

significant impact on their neighborhoods’ future. Creative organizing strategies to engage

both tenants and landlords and policy changes that encourage greater stability of tenure for

tenants, could be important steps toward greater neighborhood stability, although perhaps

not a substitute for homeownership. Moreover, because many tenants eventually do become

homeowners, such policies would in all likelihood increase the probability that they

buy in the neighborhood, rather than join the flight to the suburbs.

Endnotes

1. It is worth noting, however, that although homeownership may play a more potent ideological role in the

United States than elsewhere, when it comes to actual homeownership rates, the United States is roughly in the

middle of the pack among developed nations. While the homeownership rate in the United States is higher than

that of many European nations like Germany or France, it is much lower than in Italy or Spain, and slightly lower

than in other predominately English-speaking countries like the United Kingdom or Canada. In many of these

countries, such as Italy, Spain and Israel, homeownership in multifamily housing is much more the norm than in

the United States.

2. Cooper 2014

3. Mallach 2011

4. In addition, the problems obtaining reliable data at the neighborhood level are considerable.

5. For obscure historic reasons, the dominant urban neighborhood house form in in a coastal belt including

northern New Jersey and most of coastal New England was the two- and three-family house, in which the units

were stacked on one another. In Boston, they are known as ‘triple-deckers’. Such houses, while also found elsewhere,

make up only a small part of the residential stock in other American cities.

6. This obscures a significant difference between rural and urban housing; in 1900, the non-farm homeownership

rate was only 36.4%.

7. Not only is this inherently difficult to measure, but the difficulty is compounded by the effect of homeownership

itself; in other words, the process of becoming a homeowner may change the individual’s values and

attitudes in significant ways. A fascinating study from Argentina offers strong evidence of those effects (Di Tella et

al, 2007).

8. Coulton, Theodos and Turner 2009.

9. Barker and Miller 2009

10. Rohe and Stewart 1996

11. New Jersey landlord-tenant law prohibits eviction except for cause. Tenants are deemed to have indefinite

tenure, and unlike most parts of the United States, may not be evicted simply because their lease has expired.

Other than for cause, such as non-payment of rent, the only grounds for eviction are that the owner needs the

house or apartment for their personal use. Moreover, rent control is permitted at local option by state law, and

is widely used. While the average length of tenure for tenants in New Jersey is slightly longer than in the United

States as a whole (45% moved in the previous two years, compared to 56%), the difference is roughly proportionate

to the difference for homeowners (11 years compared to 13 years), suggesting that the difference is associated

with lower in- and out-migration levels for New Jersey, rather than any effect of greater security of tenure on rental

stability. However, comparing New Jersey to states with similar migratory profiles, such as Connecticut and Ohio,

we find a slight difference (45% in New Jersey compared to 49% in Ohio and 51% in Connecticut), suggesting

that the different landlord-tenant regime in New Jersey may have some effect on tenure. If so, it is a very modest

one, representing a difference of at most a few months.

12. Mallach 2011.

13. The recent foreclosure crisis has spawned a substantial body of research on the impacts of foreclosure on

neighboring properties, which makes a compelling case for its destructive effects. A recent study by Williams,

Galster and Verma (2013) is particularly worth noting, in that it found a causal relationship between foreclosure

and subsequent decline, as the authors note, “the completed foreclosure indicator was strongly predictive of three

other indicators: property crimes, total home purchase loan amounts, and mean home purchase loan amounts

(p207).” They characterize foreclosures as an “early warning indicator” of neighborhood change.

14. Ellen at al 2002, Ding and Knapp 2003

15. Coulson, Hwang, and Imai (2002, 2003)

16. Ding and Knapp 2003.

17. Rohe and Stewart 1996.

18. Galster 1987

19. Ioannides 2002

20. Mallach 2014a

21. Mallach 2014b

22. Todd 2010

23. Robinson and Todd 2010, Robinson 2012

24. Green and White 1997

25. Boehm and Schlottmann 1999

26. Rossi and Weber 1996; Diaz-Serrano 2009

27. Rohe and Basolo 1997

28. Manturuk 2012

29. Bowdler, Quercia and Smith 2010, Pollock and Lynch 2009

30. Temkin and Rohe 1998, p. 82. Social capital in their study combined institutional infrastructure and sociocultural

milieu, which they define as “a construct that attempts to capture both observable behaviors of neighborhood

residents and their unobservable affective sentiments toward the area.” (p. 69)

31. Sampson 2012, p. 27. They defined collective efficacy by (1) constructing an index of social control, in which

they asked respondents how they would react (on scale of 1 to 5) to various situations, such as if a fight broke out

in front of their house, or they saw children spray-painting graffiti on a nearly building; and (2) constructing a

similar index of social cohesion, asking respondents how they felt about statements such as ‘people in this neighborhood

can be trusted’. Finding that the two scales correlated very strongly with one another, they combined

them to create their measure of collective efficacy.

32. Jacobs 1961. p. 112.

33. (1997), p. 918

34. Ibid. (p. 923)

35. Morenoff, Sampson and Raudenbush 2011

36. DiPasquale and Glaeser 1998, Cheo, Fesselmeyer and Seah 2013

37. Manturuk, Lindblad and Quercia 2010

38. Lindblad, Manturuk and Quercia 2013

39. Lauridsen, Nannerup and Skak 2006

40. Friedrichs and Blasius 2006

41. This is based on the proposition that investor-buyers are significantly less likely to obtain mortgages from

HMDA-reporting sources than are homebuyers, particularly first-time homebuyers. This proposition is strongly

supported by a 2011 analysis from Campbell/Inside Mortgage Finance, which found that 77% of investor-buyers

bought with cash, compared to 26% of ‘move-up’ homebuyers and 10% of first-time homebuyers. See Tracking

Real Estate Market Conditions using the Housing Pulse Survey, available at http://campbellsurveys.com/housingpulse/HousingPulse_white_paper.pdf

42. http://www.urban.org/urban-wire/tight-credit-standards-prevented-52-million-mortgages-between2009-and-2014

43. Mallach 2014a

44. Mallach 2015

45. We used on-line databases maintained by the State of New Jersey for all real property records and for real

property transactions, singling out what are termed Class 2 (one to four family residential) properties. Purchases

by investors were defined as those where (1) the address of the property and the address of the buyer were different;

or (2) for transactions where the addresses were the same, where the name of the buyer was clearly not an

individual or couple; e.g., “233 Chestnut LLC” or “Flip-That-House, Inc.”

46. It should be possible to calculate the rate of erosion using these data bases by identifying investor vs. owneroccupant

sellers as well as buyers. While such an analysis was beyond the scope of the Trenton study or this paper,

it would be valuable, and I hope to be able to carry it out in the near future.

47. Regrettably, the ACS data that I used to present citywide data on homeownership erosion in Tables 4A and

4B does not exist in reliable form at the neighborhood (census tract) level. The only data is available from the fiveyear

rather than one-year ACS, thus covering a narrower and more uncertain time period, and with a very large

margin of error, which is particularly problematic when trying to compare relatively fine-grained changes.

48. The investor share of single family purchases by neighborhood showed very strong correlations (significance

level of .99 or greater) with homeownership rate, tax delinquency, violent crime, vacancy and median sales price.

49. Fennell 2009.

50. Haurin and Gill 2002

References

David Barker and Eric A. Miller, “Homeownership and Child Welfare,” Real Estate Economics 37 (2) (2009): 279-303

Thomas P. Boehm and Alan Schlottmann. “Does Home Ownership by Parents Have an Economic Impact on Their

Children?” Journal of Housing Economics 8 (3) (1999): 217-232.

Janice Bowdler, Roberto Quercia, and David A. Smith. The Foreclosure Generation: The Long-Term Impact of

The Housing Crisis on Latino Children and Families” (Washington, DC: National Council of La Raza, (2010).

Ryan Cooper. “It’s time to kill the American dream of homeownership” This Week, April 25, 2014

N. Edward Coulson, Seek-Joon Hwang and Susumu Imai. “The Value of Owner-Occupation in Neighborhoods”

Journal of Housing Research 13(2) (2002): 153

N. Edward Coulson, Seek-Joon Hwang and Susumu Imai. “The Benefits of Owner-Occupation in Neighborhoods”

Journal of Housing Research 14(1) (2003): 21

Claudia Coulton, Brett Theodos and Margery A. Turner. Family Mobility and Neighborhood Change: New Evidence

and Implications for Community Initiatives. Washington DC: Urban Institute (2009)

Luis Diaz-Serrano. “Disentangling the housing satisfaction puzzle: Does homeownership really matter?” Journal

of Economic Psychology 30(5) (2009): 745-755.

Chengri Ding and Gerrit-Jan Knaap. “Property Values in Inner City Neighborhoods: The Effects of Home Ownership,

Housing Investment and Economic Development.” Housing Policy Debate 13(4) (2003), 701-727

Rafael Di Tella, Sebastian Galiani and Ernesto Schargrodsky. “The Formation of Beliefs: Evidence from the Allocation

of Land Titles to Squatters” Quarterly Journal of Economics 122 (1) (2007): 209-241.

Ingrid Gould Ellen, Michael Schill, Scott Susin and Amy Ellen Schwartz. “Building Homes, Reviving Neighborhoods:

Spillovers from Subsidized Construction of Owner-Occupied Housing in New York City” Journal of

Housing Research, 12 (1) (2002): 447-77

Jurgen Friedrichs and Jorg Blasius “Attitudes of Owners and Renters in a Deprived Neighborhood” Paper presented

at the ENHR Conference, Ljubljana, Slovakia (2006)

Lee Anne Fennel. The Unbounded Home: Property Values Beyond Property Lines. New Haven: Yale University

Press (2009)

George C. Galster. Homeowners and Neighborhood Reinvestment Durham NC: Duke U Press (1987)

Richard K. Green and Michelle J. White. “Measuring the Benefits of Homeowning: Effects on Children,” Journal

of Urban Economics 41 (3) (1997): 441-461

Donald R. Haurin and H.Leroy Gill. “The Impact of Transaction Costs and the Expected Length of Stay on

Homeownership” Journal of Urban Economics 51 (3) (2002): 563-584

Yannis M. Ioannides. “Residential neighborhood effects.” Regional Science and Urban Economics 32 (2) (2002):

145-165

Jane Jacobs. The Death and Life of Great American Cities New York, NY: Random House (1961)

Jorgen Lauridsen, Niels Nannerup and Morten Skak. “Owner-Occupied Housing and Crime Rates in Denmark”

Paper presented at the 2006 ENHR Conference, Ljubljana, Slovakia (2006)

Mark Lindblad, Kim Manturuk and Roberto Quercia. “Sense of Community and Informal Social Control among

Lower Income Households: The Role of Homeownership and Collective Efficacy in Reducing Subjective Neighborhood

Crime and Disorder.” American Journal of Community Psychology, 51 (1) (2013): 123-139

Alan Mallach. Building Sustainable Ownership: Rethinking Public Policy Toward

Lower-Income Homeownership. Philadelphia: Federal Reserve Bank of Philadelphia (2011)

Alan Mallach. “Lessons From Las Vegas: Housing Markets, Neighborhoods, and Distressed Single-Family Property

Investors” Housing Policy Debate 24 (4) (2014a): 769-801

Alan Mallach Housing Market Conditions Assessment: City of Flint, Michigan. Flint: Center for Community

Progress (2014b)

Alan Mallach. Laying the Foundation for Strong Neighborhoods in Trenton, New Jersey New Brunswick: New

Jersey Community Capital and Washington DC: Center for Community Progress (2015)

Kim Manturuk, Mark Lindblad and Robert Quercia. “Friends and Neighbors: Homeownership and Social Capital

among Low- to Moderate-Income Families” Journal of Urban Affairs 32 (4) (2010): 471-488

Kim Manturuk. “Urban Homeownership and Mental Health: Mediating Effect of Perceived Sense of Control.”

City & Community 11 (4) (2012): 409-430

Jeffrey D. Morenoff, Robert J. Sampson and Stephen W. Raudenbush. “Neighborhood inequality, collective efficacy,

and the spatial dynamics of urban violence” Criminology; 39 (3) (2001); 517-558

National Association of Realtors. Social Benefits of Homeownership and Stable Housing. Washington DC: NAR

Research Division (2006)

Craig Evan Pollock and Julia Lynch. “Health Status of People Undergoing Foreclosure in the Philadelphia Region”

American Journal of Public Health 99 (10) (2009): 1833-1839

Robert D. Putnam, Robert D. “The Prosperous Community: Social Capital and Public Life.” The American Prospect,

Spring 1993.

Breck L. Robinson and Richard M. Todd. The Role of Non-Owner-Occupied Homes in the Current Housing and

Foreclosure Cycle. Richmond: Federal Reserve Bank of Richmond (2010)

Breck L. Robinson. “The Performance of Non-Owner-Occupied Mortgages During the Housing Crisis”. Economic

Quarterly 98 (2) (2012): 111-138

William Rohe and Leslie S. Stewart. “Home Ownership and Neighborhood Stability” Housing Policy Debate 7:1

(1996): 37-81

William Rohe and Victoria Basolo. “Long-Term Effects of Homeownership on the Self-Perceptions and Social

Interactions of Low Income Persons” Environment and Behavior 29 (6) (1997): 793-819

Peter H. Rossi and Eleanor Weber. “The Social Benefits of Homeownership:

Empirical Evidence from National Surveys” Housing Policy Debate 7 (1) (1996): 1-35

Robert J. Sampson, Stephen W. Raudenbush and Felton Earls. “Neighborhoods and Violent Crime: A Multilevel

Study of Collective Efficacy” Science 277 (1997): 918-924

Robert J. Sampson. Great American City. Chicago IL: University of Chicago Press (2012)

Kenneth Temkin and William Rohe. “Social Capital and Neighborhood Stability: An Empirical Investigation”

Housing Policy Debate 9 (1) (1998): 61-88

Richard M. Todd. Foreclosures on Non-Owner-Occupied Properties in Ohio’s Cuyahoga County: Evidence from

Mortgages Originated in 2005–2006. Minneapolis: Federal Reserve Bank of Minneapolis (2010)

Sonya Williams, George Galster and Nandita Verma. “Home Foreclosures as an Early Warning Indicator of Neighborhood

Decline” Journal of the American Planning Association 79:3 (2013): 201-210

Writer, scholar, practitioner and advocate, Alan Mallach has been engaged with the challenges of

urban revitalization, neighborhood stabilization and housing provision for fifty years. A senior fellow

with the Center for Community Progress, he has held a number of public and private sector positions,

and currently also teaches in the graduate city planning program at Pratt Institute in New York City.

His publications include many books, among them Bringing Buildings Back: From Vacant Properties

to Community Assets and A Decent Home: Planning, Building and Preserving Affordable Housing,

as well as numerous articles, book chapters and reports. He has a B.A. degree from Yale College, and

lives in Roosevelt, New Jersey.