Central banks and governments around the world must be able to adapt policy to changing economic circumstances. The time has come to critically reassess prevailing policy frameworks and consider adjustments to handle new challenges, specifically those related to a low natural real rate of interest. While price level or nominal GDP targeting by monetary authorities are options, fiscal and other policies must also take on some of the burden to help sustain economic growth and stability.

As nature abhors a vacuum, so monetary policy abhors stasis. Instead of being a rigid set of precepts, it follows the adage, that which survives is that which is most adaptive to change. Over the past century, monetary policy strategies have evolved in response to changing realities, from the panics and depressions of the late 19th and early 20th centuries that led to the creation of the Federal Reserve to the Great Depression, from Bretton Woods and subsequent battles to contain inflation to the dominance of inflation targeting today (Williams 2014, 2015a).

In the wake of the global financial crisis, monetary policy has continued to evolve, in this latest incarnation battling low inflation and stagnation via unconventional monetary policy actions like quantitative easing and near-zero or even negative interest rates. As we move forward, economic conditions require that central banks and governments throughout the world carefully reexamine their policy frameworks and consider further adjustments in terms of monetary policy strategy—both in its own right and as it relates to other policy arenas—to successfully navigate these new seas.

All the economic world’s a stage: The roles of monetary and fiscal policy

To set the stage, we must look at pre-crisis views of the roles of monetary and fiscal policy. The inflation wars of the 1970s and 1980s led to a broad consensus on two fronts among academics and policymakers: First, central banks are responsible and accountable for price stability, which was often acknowledged through the formal adoption of an inflation targeting framework. Second, monetary policy should play the lead role in stabilizing inflation and employment, while fiscal policy plays a supporting role through mechanisms like automatic stabilizers and ad hoc fiscal stimulus during recessions. In this mindset, fiscal policy should focus primarily on longer-run goals such as economic efficiency and equity. The consensus on these two is evinced by countless research papers dedicated to monetary policy strategy and implementation in the past quarter-century, compared with a relative handful on the design of countercyclical fiscal policy.

In the post-financial crisis world, however, new realities pose significant challenges for the conduct of monetary policy. Foremost is the significant decline in the natural rate of interest, or r* (r-star), over the past quarter-century to historically low levels. Our understanding of the economy and monetary policy are underpinned by the concept of the natural interest rate—that is, the short-term real (inflation-adjusted) interest rate that balances monetary policy so that it is neither accommodative nor contractionary in terms of growth and inflation. In this Letter, I focus on the medium-term value of the natural rate—essentially what inflation-adjusted interest rates will be in an economy at full strength.

While a central bank sets its short-term interest rate, r-star is a function of the economy that is beyond its influence. The new challenge for central banks is how to deliver stable inflation in a low r-star world. This conundrum shares some characteristics and common roots with the theory of secular stagnation; in both scenarios, interest rates, growth, and inflation are persistently low (Summers 2015).

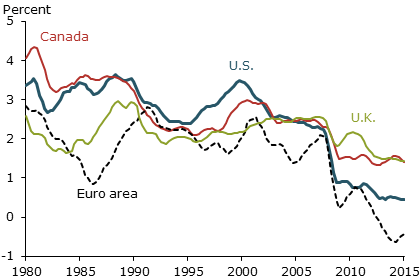

How low can rates stay?

A variety of economic factors have pushed natural interest rates very low and they appear poised to stay that way (Williams 2015b, Laubach and Williams 2015, Hamilton et al. 2015, Kiley 2015, Lubik and Matthes 2015). This is the case not just for the United States but for other advanced economies as well. Figure 1 shows estimates of the inflation-adjusted natural rate for four major economies: the United States, Canada, the euro area, and the United Kingdom (Holston, Laubach, and Williams 2016). In 1990, estimates ranged from about 2½ to 3½%. By 2007, on the eve of the global financial crisis, these had all declined to between 2 and 2½%. By 2015, all four estimates had dropped sharply, to 1½% for Canada and the United Kingdom, nearly zero for the United States, and below zero for the euro area.

Figure 1

Estimated inflation-adjusted natural rates of interest

Source: Holston, Laubach, and Williams (2016); data are four- quarter moving averages.

The underlying determinants for these declines are related to the global supply and demand for funds, including shifting demographics, slower trend productivity and economic growth, emerging markets seeking large reserves of safe assets, and a more general global savings glut (Council of Economic Advisers 2015, International Monetary Fund 2014, Rachel and Smith 2015, Caballero, Farhi, and Gourinchas 2016). The key takeaway from these global trends is that interest rates are going to stay lower than we’ve come to expect in the past. This does not mean they will be zero, but when juxtaposed with pre-recession normal short-term interest rates of, say, 4 to 4½%, it may be jarring to see the underlying r-star guiding us towards a new normal of 3 to 3½%—or even lower. Importantly, this future low level of interest rates is not due to easy monetary policy; instead, it is the rate expected to prevail when the economy is at full strength and the stance of monetary policy is neutral.

The critical implication of a lower natural rate of interest is that conventional monetary policy has less room to stimulate the economy during an economic downturn, owing to a lower bound on how low interest rates can go. This will necessitate a greater reliance on unconventional tools like central bank balance sheets, forward guidance, and potentially even negative policy rates. In this new normal, recessions will tend to be longer and deeper, recoveries slower, and the risks of unacceptably low inflation and the ultimate loss of the nominal anchor will be higher (Reifschneider and Williams 2000). We have already gotten a first taste of the effects of a low r-star, with uncomfortably low inflation and growth despite very low interest rates. Unfortunately, if the status quo endures, the future is likely to hold more of the same—with the possibility of even more severe challenges to maintaining price and economic stability.

Low r-star and strategies for mitigation

To avoid this fate, central banks and governments should critically reassess the efficacy of their current approaches and carefully consider redesigning economic policy strategies to better cope with a low r-star environment. This includes considering fiscal and other policies aimed at raising the natural interest rate, as well as alternative monetary and fiscal policies that are more likely to succeed in the face of a low natural rate.

Taking each of those in turn, I’ll start with policies aimed at raising r-star by affecting its underlying determinants. One potential avenue is to increase longer-run growth and prosperity through greater long-term investments in education, public and private capital, and research and development. Despite growing skepticism and endless column inches questioning whether college is worth the cost, the return on investment in post-secondary education is as high as ever (Autor 2014, Daly and Cao 2015). Likewise, returns on infrastructure and research and development investment are very high on average (Jones and Williams 1998, 2000, Fernald 1999).

Turning to policies that can help stabilize the economy during a downturn, countercyclical fiscal policy should be our equivalent of a first responder to recessions, working hand-in-hand with monetary policy. Instead, it has too often been stuck in a stop-and-go cycle, at times complementing monetary policy, at times working against it. This is not unique to the United States; Japan, and Europe have also fallen victim to fiscal consolidation in the midst of an economic downturn or incomplete recovery.

One solution to this problem is to design stronger, more predictable, systematic adjustments of fiscal policy that support the economy during recessions and recoveries (Williams 2009, Elmendorf 2011, 2016). These already exist in the form of programs such as unemployment insurance but are limited in size and scope. Some possible ideas for the United States include Social Security and income tax rates that move up or down in relation to the national unemployment rate, or federal grants to states that operate in the same way. Such approaches could be designed to be revenue-neutral over the business cycle; they also could avoid past debates over fiscal stimulus by separating decisions on countercyclical policy from longer-run decisions about the appropriate role of the government and tax system. Indeed, economists across the political spectrum have championed these ideas (Elmendorf and Furman 2008, Taylor 2000, 2009).

Finally, monetary policy frameworks should be critically reevaluated to identify potential improvements in the context of a low r-star. Although targeting a low inflation rate generally has been successful at taming inflation in the past, it is not as well-suited for a low r-star era. There is simply not enough room for central banks to cut interest rates in response to an economic downturn when both natural rates and inflation are very low.

Two alternatives can be considered together or in isolation to address this issue. First, the most direct attack on low r-star would be for central banks to pursue a somewhat higher inflation target. This would imply a higher average level of interest rates and thereby give monetary policy more room to maneuver (Williams 2009; Blanchard, Dell’Ariccia, and Mauro 2010; Ball 2014). The logic of this approach argues that a 1 percentage point increase in the inflation target would offset the deleterious effects of an equal-sized decline in r-star. Of course, this approach would need to balance the purported benefits against the costs and challenges of achieving and maintaining a somewhat higher inflation rate.

Second, inflation targeting could be replaced by a flexible price-level or nominal GDP targeting framework, where the central bank targets a steadily growing level of prices or nominal GDP, rather than the rate of inflation. These approaches have a number of potential advantages over standard inflation targeting. For one, they may be better suited to periods when the lower bound constrains interest rates because they automatically deliver the “lower for longer” policy prescription the situation calls for (Eggertsson and Woodford 2003). In addition, nominal GDP targeting has a built-in protection against debt deflation (Koenig 2013, Sheedy 2014). Finally, in a nominal GDP targeting regime, a decline in r-star caused by slower trend growth automatically leads to a higher rate of trend inflation, providing a larger buffer to respond to economic downturns. Of course, these approaches also have potential disadvantages and must be carefully scrutinized when considering their relative costs and benefits.

In stressing the need to study and consider new approaches to fiscal and monetary policy, I am not advocating an abrupt reversal of course; after all, you don’t change horses in the middle of a stream. And in monetary policy, “abrupt” and “disrupt” have more than merely resonance of sound in common. But now is the time for experts and policymakers around the world to carefully investigate the pros and cons of these proposals.

Conclusion

Economics rarely has the benefit of a crystal ball. But in this case, we are seeing the future now and have the opportunity to prepare for the challenges related to persistently low natural real rates of interest. Thoroughly reviewing the key aspects of inflation targeting is certainly necessary, and could go a long way towards mitigating the obstructions posed by low r-star. But that is where monetary policy meets the boundaries of its influence. We’ve come to the point on the path where central banks must share responsibilities. There are limits to what monetary policy can and, indeed, should do. The burden must also fall on fiscal and other policies to do their part to help create conditions conducive to economic stability.

Policymakers don’t often cite Machiavelli, but in this instance, the analogy is potent (and, perhaps, a portent). In The Prince, fortune is compared to a river; in times of turbulence it wreaks havoc, flooding and destroying everything in its way. But in calm and sedate weather, people can build dams and stem the tide of destruction. In other words, we can wait for the next storm and hope for better outcomes or prepare for them now and be ready.

John C. Williams is president and chief executive officer of the Federal Reserve Bank of San Francisco.

References

Autor, David H. 2014. “Skills, Education, and the Rise of Earnings Inequality among the ‘Other 99 Percent.’” Science 344(6186, May 23), pp. 843–851.

Ball, Laurence. 2014. “The Case for a Long-Run Inflation Target of Four Percent.” IMF Working Paper 14/92, June.

Blanchard, Olivier, Giovanni Dell’Ariccia and Paolo Mauro. 2010. “Rethinking Macroeconomic Policy.” IMF Staff Position Note 10/03.

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas. 2016. “Global Imbalances and Currency Wars at the ZLB.” Manuscript, UC Berkeley, March 10.

Council of Economic Advisers. 2015. “Long-Term Interest Rates: A Survey.” Report, July.

Daly, Mary C., and Yifan Cao. 2015. “Does College Pay?” In Does College Matter? FRB San Francisco 2014 Annual Report.

Eggertsson, Gauti B., and Michael Woodford. 2003. “The Zero Bound on Interest Rates and Optimal Monetary Policy.” Brookings Papers on Economic Activity 2003(1, Spring), pp. 139–211.

Elmendorf, Douglas W. 2011. “Policies for Increasing Economic Growth and Employment in 2012 and 2013.” Statement before the Committee on the Budget, United State Senate. November 15.

Elmendorf, Douglas W. 2016. “Recommendations for Federal Fiscal Policy.” Remarks at FRB San Francisco, March 4.

Elmendorf, Douglas W., and Jason Furman. 2008. “If, When, How: A Primer on Fiscal Stimulus.” Strategy Paper, The Hamilton Project, January.

Fernald, John G. 1999. “Roads to Prosperity? Assessing the Link between Public Capital and Productivity.” American Economic Review 89(3, June), pp. 619–638.

Hamilton, James D., Ethan S. Harris, Jan Hatzius, and Kenneth D. West. 2015. “The Equilibrium Real Funds Rate: Past, Present, and Future.” Presented at the U.S. Monetary Policy Forum, New York, February 27 (revised August 2015).

Holston, Kathryn, Thomas Laubach, and John C. Williams. 2016. “Measuring the Natural Rate of Interest: International Trends and Determinants.” FRBSF Working Paper 2016-11, June.

International Monetary Fund. 2014. World Economic Outlook, April.

Jones, Charles I., and John C. Williams. 1998. “Measuring the Social Return to R&D.” Quarterly Journal of Economics 113(4), pp. 1119–1135.

Jones, Charles I., and John C. Williams. 2000. “Too Much of a Good Thing? The Economics of Investment in R&D.” Journal of Economic Growth 5 (1, March), pp. 65–85.

Kiley, Michael T. 2015. “What Can the Data Tell Us About the Equilibrium Real Interest Rate?” Finance and Economics Discussion Series 2015-077, Federal Reserve Board of Governors.

Koenig, Evan F. 2013. “Like a Good Neighbor: Monetary Policy, Financial Stability, and the Distribution of Risk.” International Journal of Central Banking 9(2, June), pp. 57–82.

Laubach, Thomas, and John C. Williams. 2015. “Measuring the Natural Rate of Interest Redux.” FRB San Francisco Working Paper 2015-16, October, forthcoming in Business Economics.

Lubik, Thomas A., and Christian Matthes. 2015. “Calculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches.” FRB Richmond, Economic Brief 15-10, October.

Rachel, Lukasz, and Thomas D. Smith. 2015. “Secular Drivers of the Global Real Interest Rate.” Bank of England Staff Working Paper 571, December.

Reifschneider, David, and John C. Williams. 2000. “Three Lessons for Monetary Policy in a Low Inflation Era.” Journal of Money, Credit, and Banking 32(4, November), pp. 936–966.

Sheedy, Kevin D. 2014. “Debt and Incomplete Financial Markets: A Case for Nominal GDP Targeting.” Brookings Papers on Economic Activity, Spring, pp. 301–361.

Summers, Lawrence H. 2015. “Demand Side Secular Stagnation.” American Economic Review 105(5, May), pp. 60–65.

Taylor, John B. 2000. “Reassessing Discretionary Fiscal Policy.” Journal of Economic Perspectives 14(3), pp. 21–36.

Taylor, John B. 2009. “The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy.” American Economic Review 99(2), pp. 550–555.

Williams, John C. 2009. “Heeding Daedalus: Optimal Inflation and the Zero Bound.” Brookings Papers on Economic Activity 2, pp. 1–37.

Williams, John C. 2014. “Inflation Targeting and the Global Financial Crisis: Successes and Challenges.” Presentation to the South African Reserve Bank Conference, Pretoria, October 31.

Williams, John C. 2015a. “Monetary Policy and the Independence Dilemma.” Presentation to Chapman University, Orange, CA, May 1.

Williams, John C. 2015b. “The Decline in the Natural Rate of Interest.” Business Economics 50(2, April), pp. 57–60.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org