Small businesses and farms were hit hard by restrictions that limited their ability to pay operating costs during the COVID-19 crisis. Banks played an important supportive role, substantially expanding the loans available to these firms during the early months of the crisis. The growth in lending was associated with small business participation in the Paycheck Protection Program (PPP) and bank use of the PPP Liquidity Facility. Analyzing data for the first half of 2020 suggests that these programs were successful in supporting lending growth during the crisis, particularly among small banks.

The rising threat of the COVID-19 pandemic in March resulted in a sharp increase in bank borrowing by U.S. businesses. This reflected businesses’ widespread concerns about their ability to maintain access to funding in light of worsening economic conditions. In particular, corporate borrowing from banks rose $532 million overall, representing a 5.1% increase in the first half of the year. By comparison, borrowing increased only 3.6% during the first six months of 2019.

As Federal Reserve Governor Michelle Bowman (2020) noted, small businesses, which tend to be service-oriented and clustered in retail and food services, were heavily affected by the pandemic. This Letter examines small business borrowing during the pandemic, highlighting the lending role of small—or “community”—banks. Despite the large number of small banks—defined as those with total assets less than $10 billion—they are dwarfed by medium and large banks in the amount of total lending. However, they are important participants in small business and farm lending. In the sample we study, they comprised about 25% of lending to this category in the second quarter of 2020.

In addition, we examine the role of the Paycheck Protection Program (PPP) launched by the Treasury Department in March under the Coronavirus Aid, Relief, and Economic Security (CARES) Act and administered by the Small Business Administration (SBA). The goal of the program was to help small businesses survive during the pandemic-associated lockdowns. We find that the intensity of participation by banks in the PPP was associated with greater growth in lending to small businesses and farms. Moreover, our analysis shows that bank participation in the Federal Reserve’s Paycheck Protection Program Lending Facility (PPPLF) was also positively associated with their degree of PPP participation, particularly among small banks.

As such, these two programs seem to have encouraged increased lending to small businesses and farms during the COVID-19 crisis. To the extent that small businesses’ credit needs are dependent on their relationships with smaller banks, these programs also appear to have helped reduce the financial strain on small businesses.

Measuring lending for different sized banks

Commercial banks in the United States are required to file quarterly Call Reports of their balance sheets and income statements. We use this bank-level data from the end of the fourth quarter of 2019 through the second quarter of 2020 to evaluate lending activity by banks of different sizes during the height of the pandemic lockdowns. We separate banks into three groups: small banks with total assets below $10 billion, large banks with assets exceeding $100 billion, and medium banks with assets ranging between the two. Our year-end 2019 sample includes 4,247 small banks, 641 medium-sized banks, and 138 large banks. These three categories respectively accounted for 7.6%, 12.1%, and 80.3% of total lending during this period, highlighting the outsized role of larger banks.

However, small banks play a much larger role in small business lending. We follow regulatory reporting conventions that define small business loans as being $1 million or less that are issued as either standard commercial loans, secured by nonfarm nonresidential properties, or small agricultural loans of $500,000 or less. The latter category includes loans secured by farmland to finance farm residential and other improvements as well as agricultural production and related activities. While some studies suggest that these reporting thresholds are imprecise indicators of lending to small businesses, we consider the standard definitions of small business and farm lending in our analysis as indicative of overall conditions in the first half of 2020. For these types of loans, small banks accounted for 25.3%, medium banks for 22.4%, and large banks for 52.2% of lending during this period; this highlights the important role of small banks, which provided about a quarter of the total lending to these borrowers.

Lending growth according to bank size

We analyze bank-level lending growth over the first half of 2020 using regression analysis. We follow the literature, such as Rice and Rose (2016) and Li, Strahan, and Zhang (2020), in choosing which Call Report variables to include to account for potentially important disparities in bank characteristics. For example, Cornett et al. (2011) demonstrated that financial constraints during the Global Financial Crisis of 2007–2009 inhibited credit expansion by banks. We account for bank-level characteristics such as the share of assets with high liquidity, the share of funding coming from deposits, the equity–capital ratio, and a measure of outstanding loan commitments. After conditioning on these traits, we examine the differences in lending growth rates across the three bank size categories. The online appendix details these conditioning variables and our formal regression results.

We first examine overall growth in lending rates by bank size over the first half of the year. Our results confirm substantial lending growth among small banks. Small bank lending grew 11.6 percentage points more on average during this period than would be expected based on their individual characteristics. This was a much larger increase than the 3.3 percentage point growth we found for small banks over the first half of 2019 using the same regression. Mid-sized banks also exhibited high growth of about 9 percentage points in the first half of 2020. However, large bank growth on average was not higher than expected based on individual firm characteristics.

We next focus on growth rates for small business and farm lending. Banks of all sizes experienced sizable increases in lending to small businesses, even after conditioning on bank characteristics. Small banks had an average of 23.2 percentage points more growth than expected. Medium and large banks experienced even higher growth at 37.7 and 34.9 percentage points, respectively. These substantially larger growth rates suggest that small businesses and farms turned to banks for funding and support to weather the business slowdown during the first half of the year.

Impact of the Paycheck Protection Program

The Paycheck Protection Program (PPP) was launched in March under the CARES Act and continued through a second round of lending that closed on August 20. The PPP was intended to help small businesses survive the lockdowns aimed at controlling the pandemic. PPP loans charged only 1% interest with maturities of two to five years. The loans also carry minimal risk because they can be forgiven if borrowers meet certain conditions, such as maintaining employee headcount or salary levels. While interest rate spreads were small under these loans, banks received SBA fee payments, which increased their non-interest income.

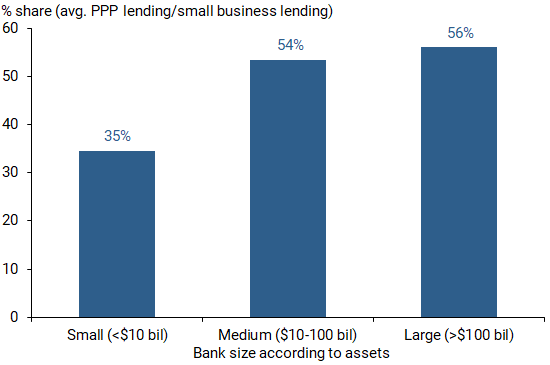

Figure 1 shows the ratios of total PPP lending to total small business and farm lending, arranged by bank size. Small banks were active PPP participants, with almost 35% of their related lending provided through the program. However, their participation as a share of small business lending on average fell short of the shares from medium and large banks, which were also significant participants in the program. Indeed, PPP-related small business lending among large banks represented over 56% of their total small business lending.

Figure 1

Ratio of total PPP lending to total small business lending

Source: Call Reports.

To evaluate the effect of PPP participation on small business loan growth rates, we incorporate these participation ratios for individual banks into our regression analysis. After accounting for differences across individual banks using the same characteristics described earlier, we find a positive and statistically significant relationship between PPP participation and small business and farm lending. Our point estimates suggest that, on average across banks, PPP participation accounts for about 20 percentage points of the growth in small business and farm lending.

While our results do not establish a causal relationship, they suggest that PPP participation is associated with increased growth in bank lending to small businesses and farms. This result is even stronger when we focus more narrowly on small business loans only. Accordingly, we argue that the PPP was effective in its primary objective of encouraging small business lending.

Impact of the liquidity facility on PPP participation

We are also interested in assessing the effect of the Federal Reserve’s PPP Lending Facility (PPPLF) on the PPP participation. The PPPLF was launched on April 9 and allowed banks to use PPP loans as collateral against central bank borrowing. This made it easier for banks to participate in the program without eroding their liquidity because banks could effectively convert their loans into cash.

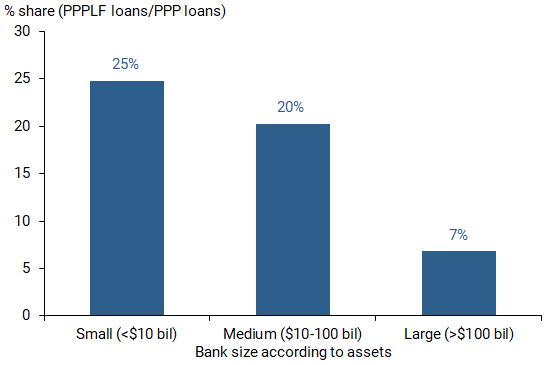

Conventional wisdom suggests that small banks would be particularly intensive users of the PPPLF to help them avoid exhausting a substantive share of their liquid assets. That is, a loan of a given size would be expected to mechanically lead to a larger increase in the share of assets extended as loans at a small bank than at a large bank.

This logic is in keeping with the unadjusted averages of PPPLF participation, as shown in Figure 2. The share of small bank PPP loans that were used as collateral for PPPLF borrowing was relatively higher than for other size banks, accounting for almost 25% of PPP lending. As such, while large banks were more active in PPP lending, the PPPLF was a more important contributor to encouraging small bank participation in the program.

Figure 2

Share of small bank PPP loans used as collateral

Source: Call Reports.

To verify this logic further, we add banks’ PPPLF participation ratios as a factor determining PPP participation in our regression analysis. This analysis provides evidence that banks’ PPPLF participation had a positive and statistically significant effect on the intensity of their participation in the PPP program. Moreover, we also confirm that the PPPLF was particularly important for small bank participation in the PPP. Thus, overall, both the PPP and the PPPLF appear to have worked together to support small business lending during the early COVID-19 period.

Conclusion

Both overall lending and lending to small businesses and farms grew rapidly during the start of the COVID-19 pandemic in the first six months, as firms secured liquid assets to maintain operations. Our analysis of this lending market shows that small banks were important contributors to this lending growth. Moreover, the launch of the Treasury’s PPP and the Federal Reserve’s PPP Liquidity Facility supported the growth of small business lending among all banks, particularly among small banks.

Remy Beauregard is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Jose A. Lopez is a vice president in the Financial Institution Supervision and Credit Department of the Federal Reserve Bank of San Francisco.

Mark M. Spiegel is a senior policy advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Bowman, Michelle W. 2020. “Community Banks Rise to the Challenge.” Speech at the Community Banking in the 21st Century Research Conference, FRB St. Louis, September 30.

Cornett, Marcia Millon, Jamie John McNutt, Philip E. Strahan, and Hassan Tehranian. 2011. “Liquidity Risk Management and Credit Supply in the Financial Crisis.” Journal of Financial Economics 101(2), pp. 297–312.

Li, Lei, Philip E. Strahan, and Song Zhang. 2020. “Banks as Lenders of First Resort: Evidence from the COVID-19 Crisis.” Review of Corporate Finance Studies 9(3), pp. 472–500.

Rice, Tara, and Jonathan Rose. 2016. “When Good Investments Go Bad: The Contraction in Community Bank Lending after the 2008 GSE Takeover.” Journal of Financial Intermediation 27, pp. 68–88.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org