Today’s economic challenges are different from the past, and it’s important to learn from history to achieve a better economic future for everyone. As the economy recovers from the effects of COVID-19, the Fed’s new policy framework retains vigilance against inflation while committing to not pull back the reins on the economy in response to a strong labor market. The following is adapted from a virtual webinar by the president and CEO of the Federal Reserve Bank of San Francisco to the Economic Club of New York on March 2.

In February of last year, right before COVID-19 hit our shores, I was in Ireland. Walking around Dublin one day, I happened upon a converted warehouse with artists selling their work. One of the artists had a wall of beautifully colored, tiny framed prints. Each one was etched with the phrase “History Will Repeat Itself” followed by an arrow pointing to the future. It seemed a pessimistic, almost fatalistic view, so I asked him if he had painted his prophecy or his fear. He answered, somewhat gruffly, “Both.”

As an unrelenting optimist, I saw something different in his work—the potential for agency. For people and institutions to learn from the past and use those lessons to shape a better future.

At the Federal Reserve, we have a practical test before us. With much welcomed light at the end of the COVID tunnel, we must work to return the economy to full employment and price stability. This is a tall order, millions of Americans are out of work and inflation remains well below our target.

At the same time, a swell of market and academic commentary has started to emerge about a quick snapback, an undesirable pickup in inflation, and the need for the Federal Reserve to withdraw accommodation more quickly than expected (see, for example, discussion in Casselman 2021 and Irwin 2021). I see this as the tug of fear. The reaction to a memory of high and rising inflation, an inexorable link between unemployment, wages, and prices, and a Federal Reserve that once fell behind the policy curve.

But the world today is different, and we can’t let those memories, those scars, dictate current and future policy. We need to learn from history without letting it drive our actions. We must consider all the lessons from our past, not just the ones that frighten us. This is what I will tackle today.

Students of history

The old normal

I started at the Federal Reserve Bank of San Francisco in 1996 and became deeply steeped in the standard macroeconomic logic that many of us learned. It goes like this. There is a level of unemployment in the economy below which wage and price inflation will start to pick up. Once that begins, the feedback loop between prices and wages and wages and prices will spiral and be hard to control. So, prudent central bankers should avoid that situation, even try to stave it off. Given that monetary policy works with a lag, this means we need to be forward-looking and respond to expected future inflation to ensure that actual inflation remains close to target.

In this simple model, our key tool was, among others, the Phillips curve, which captures the tradeoff between unemployment and inflation. The Phillips curve had the additional feature of delivering a non-accelerating inflation rate of unemployment, or NAIRU, which could be used to gauge the level of full employment. We also applied expectations theory, which posits that future inflation depends largely on expectations about future inflation.

With these tools in hand, it felt straightforward to assess where the economy stood relative to the Federal Reserve’s dual mandate goals. If unemployment was below or projected to be below NAIRU, wage and price inflation would start to build and economic agents would begin to expect higher future inflation. A responsive and proactive Fed would pull the reins on growth and the labor market and broader economy would settle at our full employment and price stability goals.

Of course, many other factors made this very simple system work. First, the real neutral rate of interest, or r-star, was well above zero, roughly in the range of 2–3%. Combined with inflation expectations above 2%, the Fed had plenty of room on both sides of the business cycle to adjust the federal funds rate and stimulate or restrain growth. Second, inflation was highly responsive to economic activity. In other words, the Phillips curve was steep. So, changes in policy that impacted growth and employment had a concurrent and significant effect on inflation.

The new normal

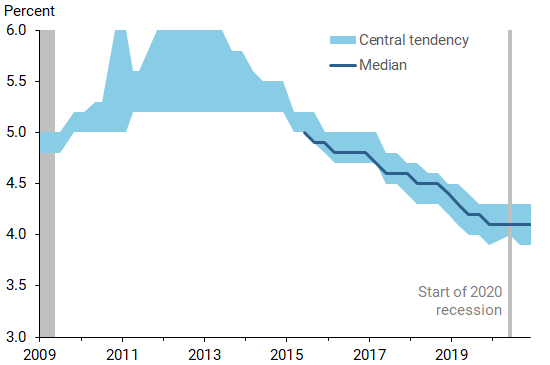

Compared with this old normal, our new normal is almost an “opposite world.” Here is what I mean. There is still some level of unemployment below which wage and price inflation will pick up, but it’s hard to know, a priori, where it is. We saw this in the last expansion, when Fed policymakers continuously lowered their estimates of the longer-run rate of unemployment in the face of modest inflationary pressures (Figure 1).

Figure 1

FOMC projections of longer-run unemployment

Source: Summary of Economic Projections, Federal Reserve Board.

Note: Gray bars indicate NBER recession dates.

The dynamics of inflation have also changed. Inflation is far less responsive to movements in output and employment than in previous decades.

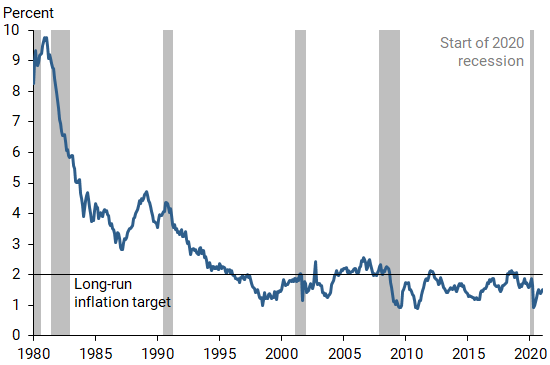

Indeed, despite a near 11-year expansion and historically low unemployment, inflation has remained stubbornly below our 2% target since the Great Recession (see Figure 2).

Figure 2

Core PCE inflation, 12-month growth rate

Source: Bureau of Economic Analysis.

Note: Gray bars indicate NBER recession dates.

This reflects, in part, a weakening of the traditional links between unemployment, wages, and prices. A large literature confirms this, showing that the Phillips curve has become quite flat in recent years (see, for example, Blanchard 2016 and Lansing 2019, and Leduc, Marti, and Wilson 2019). Declines in bargaining power for workers, fierce competition in product markets (think Amazon), and a labor force that is far more elastic than most imagined have all played a role (Daly 2019a, b). Each of these factors are likely to continue to persist in the coming years, requiring us to adjust our policies to adapt to the new environment.

We will need to make these adjustments in an environment that also looks quite different than the old normal. The real neutral rate of interest is expected to remain at very low levels, not much above zero, for some time. In this world, keeping inflation expectations well-anchored at 2% will be essential. As I noted earlier, inflation expectations are an important determinant of future inflation (Jordà et al. 2019a, b). So any drift down translates into lower inflation, a lower nominal funds rate, and fewer rate cuts when the economy needs them. In this context, long periods of below-target inflation, like the one we are experiencing, are costly.

Adapting for today

The lessons of the last decade and projections of our future conditions tell us that, for the foreseeable future, the Federal Reserve will face an uphill battle using conventional monetary policy to keep the economy healthy, the labor market strong, and inflation at our 2% goal (Mertens and Williams 2019, Amano, Carter, and Leduc 2019).

The Federal Open Market Committee’s new policy framework is an explicit recognition of these realities (Board of Governors 2020). It reflects the learnings of current and past FOMC participants, as well as inputs from our year-long review process (see Fed Listens) that included evidence from research and feedback from the businesses and communities we serve.

The resulting revised framework reemphasizes our commitment to maximum employment and stable prices and makes changes to our policy strategy that will make each of these goals easier to achieve.

Clarifying maximum employment

Starting with maximum employment, the new framework states that policy decisions will be informed by “assessments of the shortfalls of employment from its maximum level” rather than by “deviations from its maximum level.” In other words, in the absence of inflationary pressures, we will not pull back the reins on the economy in response to a strong labor market.

The statement also emphasizes that maximum employment is a broad and inclusive goal. In assessing whether it has been reached, there is no single number that tells the story. Instead, we will examine a wide range of indicators—measures like unemployment, labor force participation, job finding, and wage growth—across a broad distribution of workers.

As we apply this strategy, our most important virtue will be patience. We will need to continually reassess what the labor market is capable of and avoid preemptively tightening monetary policy before millions of Americans have an opportunity to benefit. These efforts are critical to support the broad economy and aid the inclusion of historically less advantaged groups, including people of color, those lacking college degrees, and others who face systemic barriers to equitable employment and wages (Aaronson et al. 2019, Petrosky-Nadeau and Valletta 2019).

Getting to 2% inflation

Regarding price stability, the new framework reaffirms the committee’s commitment to a 2% inflation objective but adds that this means achieving inflation that averages 2% over time. To achieve this, the FOMC will employ flexible average inflation targeting. Specifically, following periods when inflation is below 2%, appropriate monetary policy will aim to move inflation above 2% for some time.

This will ensure that inflation expectations remain well-anchored at 2%, even when policy is more frequently constrained by the zero lower bound. This approach helps put a floor under inflation expectations, enhancing our ability to achieve our full employment and price stability goals.

Practically, the new framework allows us to retain our vigilance against inflation that is too high, while improving our ability to keep inflation from falling too low. It applies the lessons from all of our history and recognizes that persistent misses on either side of the target can leave lasting damage on expectations and the economy.

An unwanted test

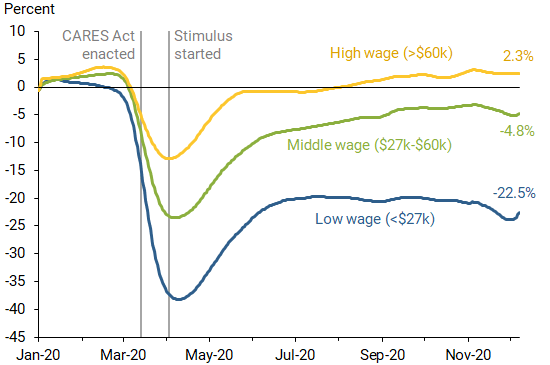

Although the evolution of the framework I just described predates the pandemic, it is exactly what we need to support the economy through this difficult time. In addition to its wrenching toll on health, the virus has severely depressed economic activity. Millions of workers remain unemployed and hundreds of thousands of businesses shuttered, some of them permanently. Digging beneath the aggregate numbers shows that a disproportionate share of affected workers come from the lower half of the wage distribution (Figure 3). Similarly, losses are concentrated among those with less than a college degree (Daly, Buckman, and Seitelman 2020).

Figure 3

Change in employment levels

Source: Opportunity Insights.

Note: Series are indexed to January 4–31, 2020; not seasonally adjusted.

Consistent with historical barriers to education and employment, these losses are also concentrated among communities of color (Gould and Wilson 2020, Kochhar 2020, Powell 2021a).

Inflation has also been pushed down by the pandemic. After falling sharply last year, it has improved as the economy has rebounded. But COVID-sensitive sectors remain a drag on overall inflation (Shapiro 2020). And even when those sectors have fully recovered, it will likely be some time before inflation is sustainably back to 2%.

Getting fully past this crisis and back on track to achieve our dual mandate goals will require monetary policy to be accommodative for some time. We must make sure that everyone who lost their job or left the labor force to care for children or other family members has an opportunity to return (Lofton, Petrosky-Nadeau, and Seitelman 2021; Chair Powell also alluded to this issue in the Q&A following his most recent Congressional testimony, Powell 2021b). We also need to offset the downward inflation pressures created by the pandemic and get back to moving inflation towards our average 2% goal.

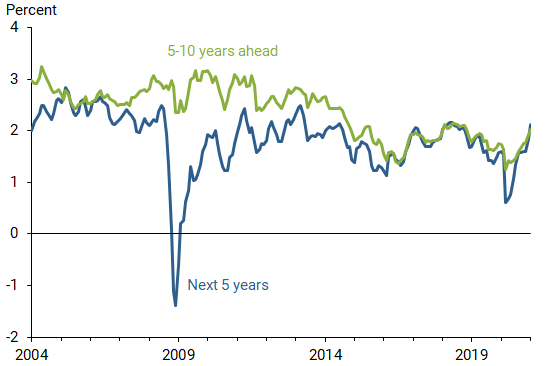

And this brings me back to the fearful swirl about spikes in inflation and the need to preemptively offset them. Of course, we need to be vigilant against all the risks in the economy, but we also must weight them by their likelihood and expected cost. As for the likelihood of runaway inflation, I don’t see this risk as imminent, and neither do market participants (Figure 4).

Figure 4

TIPS-implied inflation compensation

Source: Federal Reserve Board.

Instead, I view the recent rise in inflation compensation to roughly 2% as encouraging and in line with our stated goals. It suggests that our commitment to flexible average inflation targeting has already gained substantial credibility.

But what about the costs? The memory of the 1970s and 1980s and the painful correction it required looms large. But that was more than three decades ago, and times have changed. Today, the costs are tilted the other way. Running inflation too low for too long can pull down inflation expectations, reduce policy space, and leave millions of Americans on the sidelines along the way.

History will repeat itself, unless we learn

So, I’ll end by returning to my Irish artist friend. I bought one of his prints and put it on my office bookshelf. I keep it as a reminder that the weight of the past can be a powerful force, pulling us back to what has been. To shake its grasp requires diligence and intention, an active commitment to be students of history but not victims of it.

To do otherwise will fall short, leaving us like the picture, destined to repeat ourselves.

Mary C. Daly is president and chief executive officer of the Federal Reserve Bank of San Francisco.

References

Aaronson, Stephanie, Mary C. Daly, William Wascher, and David W. Wilcox. 2019. “Okun Revisited: Who Benefits Most from a Strong Economy?” Brookings Papers on Economic Activity Conference Draft, Spring.

Amano, Robert, Thomas J. Carter, and Sylvain Leduc. 2019. “Precautionary Pricing: The Disinflationary Effects of ELB Risk.” FRB San Francisco Working Paper 2019-26.

Blanchard, Olivier. 2016. “The Phillips Curve: Back to the ’60s?” American Economic Review 106(5), pp. 31–34.

Board of Governors of the Federal Reserve System. 2020. “Statement on Longer-Run Goals and Monetary Policy Strategy.” August 27.

Board of Governors. 2021. “Federal Reserve issues FOMC statement.” Press release, January 27.

Carvalho, Carlos, Andrea Ferrero, and Fernanda Nechio. 2016. “Demographics and Real Interest Rates: Inspecting the Mechanism.” European Economic Review 88, pp. 208–226.

Casselman, Ben. 2021. “On the Post-Pandemic Horizon, Could That Be … a Boom?” New York Times, February 21.

Daly, Mary C. 2019a. “The Bumpy Road to 2 Percent: Managing Inflation in the Current Economy.” Remarks to The Commonwealth Club, San Francisco, CA, March 26.

Daly, Mary C. 2019b. “A New Balancing Act: Monetary Policy Tradeoffs in a Changing World.” Speech at the Reserve Bank of New Zealand, Wellington, NZ. August 29.

Daly, Mary C., Shelby R. Buckman, and Lily M. Seitelman. 2020. “The Unequal Impact of COVID-19: Why Education Matters.” FRBSF Economic Letter 2020-17 (June 29).

Gould, Elise, and Valerie Wilson. 2020. “Black Workers Face Two of the Most Lethal Preexisting Conditions for Coronavirus—Racism and Economic Inequality.” Report, Economic Policy Institute, June 1.

Holston, Kathryn, Thomas Laubach, and John C. Williams. 2017. “Measuring the Natural Rate of Interest: International Trends and Determinants.” Journal of International Economics 108, supplement 1 (May), pp. S39–S75.

Irwin, Neil. 2021. “The Clash of Liberal Wonks That Could Shape the Economy, Explained.” New York Times, The Upshot, February 8.

Jordà, Òscar, Chitra Marti, Fernanda Nechio, and Eric Tallman. 2019a. “Inflation: Stress-Testing the Phillips Curve.” FRBSF Economic Letter 2019-05 (February 11).

Jordà, Òscar, Chitra Marti, Fernanda Nechio, and Eric Tallman. 2019b. “Why Is Inflation Low Globally?” FRBSF Economic Letter 2019-19 (July 15).

Kochhar, Rakesh. 2020. “Hispanic Women, Immigrants, Young Adults, Those with Less Education Hit Hardest by COVID-19 Job Losses.” Fact Tank, Pew.

Lansing, Kevin J. 2019. “Improving the Phillips Curve with an Interaction Variable.” FRBSF Economic Letter 2019-13 (May 6).

Leduc, Sylvain, Chitra Marti, and Dan Wilson. 2019. “Does Ultra-Low Unemployment Spur Rapid Wage Growth?” FRBSF Economic Letter 2019-02 (Jan. 14).

Lofton, Olivia, Nicolas Petrosky-Nadeau, and Lily Seitelman. 2021. “Parents in a Pandemic Labor Market.” FRB San Francisco Working Paper 2021-04.

Mertens, Thomas M., and John C. Williams. 2019. “Monetary Policy Frameworks and the Effective Lower Bound on Interest Rates.” American Economic Association Papers and Proceedings 109 (May), pp. 427–432.

Petrosky-Nadeau, Nicolas, and Robert G. Valletta. 2019. “Unemployment: Lower for Longer?” FRBSF Economic Letter 2019-21 (August 19).

Powell, Jerome H. 2021a. “Getting Back to a Strong Labor Market.” Speech to the Economic Club of New York (via webcast), February 10.

Powell, Jerome H. 2021b. “Semiannual Monetary Policy Report to the Congress.” Remarks delivered to the Committee on Banking, Housing, and Urban Affairs, U.S. Senate, February 23.

Shapiro, Adam Hale. 2020. “Monitoring the Inflationary Effects of COVID-19.” FRBSF Economic Letter 2020-24 (August 24).

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org