The labor force participation (LFP) rate for prime-age workers surged from early 2021 through early 2023, especially for women. This helped reduce the large shortfall of available workers relative to available jobs that emerged during the recovery from the pandemic. Analysis of state labor markets indicates that the cyclical response of prime-age LFP was much more pronounced during the two most recent business cycles than in prior ones. This state-level relationship weakened in 2023, however, suggesting that the cyclical gains in prime-age LFP are winding down.

The U.S. prime-age labor force—individuals in the age range of 25 to 54—grew rapidly as the labor market recovered from the pandemic shock. Much of this growth has come from increases in their labor force participation (LFP) rate, which measures the share of this population group who are employed or actively looking for a job.

The speed and strength of the rebound in prime-age LFP has been surprising when compared with historical patterns. As of early 2023, the prime-age LFP rate reached its highest level since the early 2000s, with the rate for men exceeding the prior peak in early 2020 and the rate for women reaching a historical high.

In this Economic Letter, we examine the dynamics of prime-age LFP and its relationship with the business cycle. In addition to published national data, we rely on state panel data formed from Current Population Survey (CPS) microdata. Our analysis shows that, during the past two business cycles that included the Great Recession of 2007-09 and the COVID-19 pandemic, the prime-age LFP rate generally moved in the same direction as overall state labor market conditions. This relationship was much less evident during the prior business cycles of the 1990s and early 2000s.

This procyclical pattern in prime-age participation during the past two business cycles suggests that LFP can act as a “safety valve” for high-pressure labor markets. In particular, the growth in the prime-age labor force has been an important factor for labor market rebalancing in the aftermath of the pandemic, helping to close a large shortfall of available workers relative to available jobs. This in turn likely has contributed to reduced hiring challenges for employers and possibly a slowdown in wage growth toward rates that are more sustainable and consistent with the Federal Reserve’s 2% inflation goal. However, we also find evidence that the cyclical upswing in prime-age LFP may have reached its limit.

Prime-age LFP rising

Prime-age people form the core of the U.S. labor force. Their share has declined as the U.S. population has aged over the past few decades, but in 2023 they still accounted for nearly two-thirds (64%) of the total labor force. Given their large share, this group’s participation in the workforce is an important determinant of overall labor availability.

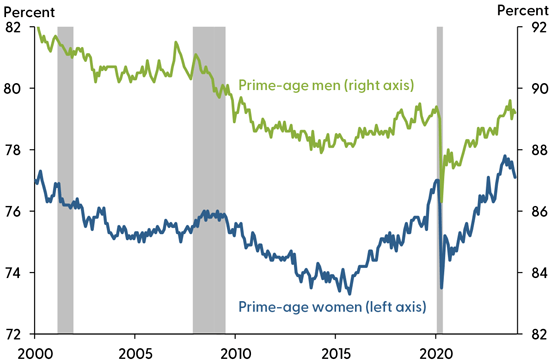

As shown in Figure 1, prime-age LFP dropped precipitously for both men and women during the early phase of the COVID-19 pandemic. After a rapid but partial recovery in the few months following the initial pandemic shock, LFP increased steadily through mid-2023. The figure also shows that the LFP increase has been especially pronounced for prime-age women. Their LFP rate has notably exceeded the pre-pandemic peak and, in fact, reached a historical high in 2023. By contrast, the rate for prime-age men has returned to its pre-pandemic level but remains well below its prior historical high.

Figure 1

Prime-age labor force participation rates

Source: Bureau of Labor Statistics via Haver Analytics (monthly data through December 2023).

This surge in prime-age LFP accounts for a large share of overall labor force growth during the pandemic recovery. Between December 2020 and December 2023, the prime-age labor force grew about two-and-a-half times faster than the prime-age population. This has helped reduce the large shortfall of available workers relative to available jobs that emerged in the aftermath of the pandemic (Valletta 2023).

The recovery in prime-age and overall LFP since the early days of the pandemic has been faster than implied by past analysis. For example, Bengali, Daly, and Valletta (2013) found that LFP recoveries typically do not start before national employment has reattained its pre-recession peak level. During the pandemic recovery, however, this payroll employment level was achieved in June 2022, about a year after prime-age LFP began a sustained recovery. In recent comprehensive research, Hobijn and Şahin (2022) examined the role of labor force flows in explaining cyclical changes in LFP. They found that fluctuations in job-loss and job-finding rates, which affect labor force attachment, are more important than cyclical movements in labor force entry and exit rates. This implies that LFP movements will tend to lag changes in unemployment. Contrary to this finding, the adjustments following the pandemic have been rapid, largely occurring in tandem with changes in unemployment. This rapid adjustment in LFP likely reflects the sudden stops and starts in the economy due to the public health measures designed to address the pandemic.

Given past analysis, the speed and extent of the prime-age LFP increase took many by surprise. However, it is comparable to the surge that occurred during the similarly tight or “hot” labor market near the end of the long economic expansion that preceded the pandemic. This suggests that the cyclical response of LFP has intensified and may be more pronounced in a hot labor market. We turn to state-level data for a more detailed assessment.

Prime-age LFP cyclicality at the state level

Past work has argued that LFP responds to business cycle conditions, falling when the economy is weak and possibly rising during recoveries (Bengali et al. 2013, Erceg and Levin 2014). We extend and update this work to a wider set of business cycles, including the pandemic. Like this past work, we use data tabulated at the state level, which affords greater variation in measured cyclical labor market conditions than do national data. We maintain our focus on prime-age workers to exclude changes in overall LFP associated with longer-term demographic changes, mainly an aging population. Prime-age LFP rates at the state level are not published in official sources. We therefore used microdata from the monthly CPS, the official U.S. labor force survey, to form state-level panel data on an annual basis for the years 1990 to 2023.

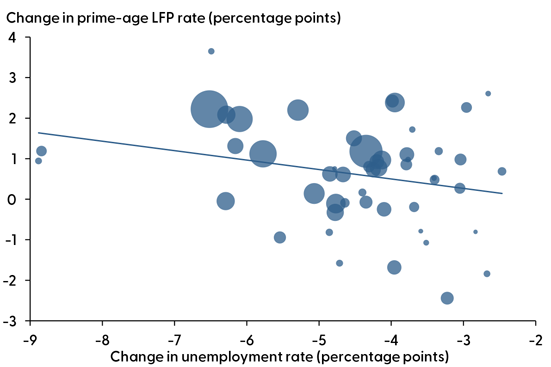

Figure 2 shows the relationship between changes in state unemployment rates and changes in the prime-age LFP rate during the initial pandemic recovery period of 2020 to 2022. Each bubble represents a state, with the size reflecting the state’s share of the total U.S. prime-age labor force. These shares are used to weight the contribution from each state in calculating the overall strength of the relationship between falling unemployment and rising prime-age participation, shown by the fitted regression line. States that experienced greater declines in their unemployment rate over this period also saw a larger increase in their prime-age LFP rate. The fitted regression line indicates that this estimated relationship is substantive and statistically precise, with a one percentage-point decline in the unemployment rate implying about a 0.37 percentage point increase in prime-age LFP.

Figure 2

Prime-age LFP and unemployment rates by state: 2020-22

Source: Authors’ calculations from CPS microdata

A potential concern about this estimate arises due to the mechanical relationship between LFP rates and unemployment: an increase in LFP without any other changes in labor market conditions will automatically increase the unemployment rate. We therefore conducted a parallel analysis of the relationship between the increasing prime-age LFP rate and the rate of payroll employment growth. The sign of the estimated relationship is positive rather than negative, given that unemployment and employment typically move in opposite directions, but otherwise the strength of the relationship is very similar to our result using the unemployment rate.

This estimated procyclical relationship between improving labor market conditions and prime-age LFP may appear to be unsurprising. It is consistent with the notion that job seekers are drawn to and stay in the labor force when employment conditions improve. However, analyzing the complete set of expansions and contractions back to 1990 indicates that this procyclical relationship has not been a long-standing feature of the data. We find a consistent procyclical relationship between changes in state unemployment and prime-age LFP rates during the economic expansions and contractions since 2015, when prime-age LFP started to recover from a long decline following the Great Recession of 2007–09. By contrast, this relationship is absent for earlier business cycles going back to 1990.

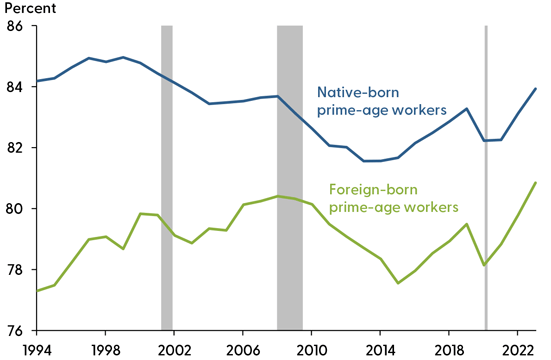

One key feature of labor force growth over the past few years has been a surge in the foreign-born labor force (Bureau of Labor Statistics 2023). We therefore assess the cyclical responsiveness of foreign-born and native-born LFP rates in parallel with our preceding analysis. Figure 3 shows prime-age LFP rates for foreign-born and native-born individuals, calculated from the CPS microdata available starting in the mid-1990s. Both groups exhibit substantial procyclicality during the two recent business cycles. To confirm this visual pattern, we repeated our regression analysis for the foreign-born and native-born groups separately. The results largely reproduce those described earlier, although they are statistically imprecise for the foreign-born group due to their small sample counts at the state level.

Figure 3

Prime-age LFP rates: Foreign-born and native workers

Source: Authors’ calculations from CPS microdata (annual averages through 2023)

Looking ahead

Given the important role of prime-age LFP gains for rebalancing the labor market, one key question is how long they are expected to continue. Our analysis suggests that these gains are winding down and may have already ended in late 2023.

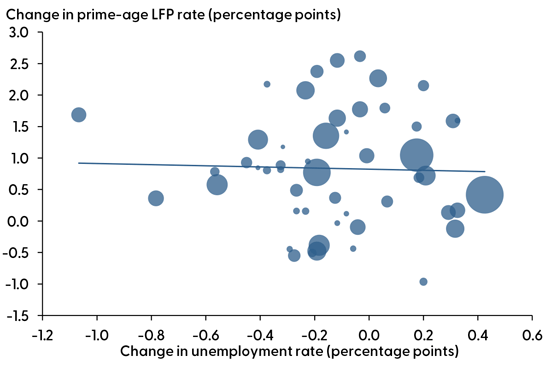

Figure 4 shows a scatter plot like Figure 2, using state changes in unemployment rates and prime-age LFP changes between 2022 and 2023. In contrast to the strong procyclical relationship for 2020–22, the estimated relationship for the subsequent annual change is somewhat weaker and statistically imprecise. This does not simply reflect measuring the change over a shorter time, since we find a strong procylical relationship when we examine changes from 2021 to 2022. The waning of procyclical gains in prime-age LFP is consistent with Figure 1, which shows a decline in prime-age LFP rates for men and women in late 2023.

Figure 4

Prime-age LFP and unemployment rates by state: 2022-23

Source: Authors’ calculations from CPS microdata.

Conclusion

Our analysis in this Letter using state panel data uncovered strong procyclical changes in prime-age LFP rates over the past two cycles, which represents a departure from little to no cyclicality in prior cycles. Although we did not examine potential explanations for the greater cyclicality in recent cycles, one plausible driver is the larger wage gains for low-wage workers during the two most recent expansions compared with prior expansions. These individuals tend to be more responsive to changes in labor market conditions than higher-wage workers; hence, higher wages for this group may be propelling the observed LFP increases, which is broadly consistent with the findings in Aaronson et al. 2019.

Our results suggest that by increasing worker availability during economic expansions, rising prime-age LFP may act as a “safety valve” for hot labor markets, helping to ease upward wage and price pressures. However, our results for the years 2022–23 indicate that the recent procyclical rise in prime-age LFP may have ended. These findings suggest that further rebalancing of the labor market will need to come from slower growth in labor demand rather than continued rapid growth in worker supply.

References

Aaronson, Stephanie R., Mary C. Daly, William L. Wascher, and David W. Wilcox. 2019. “Okun Revisited: Who Benefits Most from a Strong Economy?” Brookings Papers on Economic Activity, Spring 2019.

Bengali, Leila, Mary Daly, and Rob Valletta. 2013. “Will Labor Force Participation Bounce Back?” FRBSF Economic Letter 2013-14 (May 13).

Bureau of Labor Statistics. 2023. “Foreign-Born Workers Were a Record High 18.1% of the U.S. Civilian Labor Force in 2022.” The Economics Daily, June 16.

Erceg, Christopher J., and Andrew T. Levin. 2014. “Labor Force Participation and Monetary Policy in the Wake of the Great Recession.” Journal of Money, Credit and Banking, 46(2, October), Supplement.

Hobijn, Bart, and Ayşegül Şahin. 2022. “Maximum Employment and the Participation Cycle.” In Macroeconomic Policy in an Uneven Economy, conference proceedings of the 2021 Jackson Hole Economics Symposium. Kansas City: Federal Reserve Bank of Kansas City, pp. 273–372.

Valletta, Robert G. 2023. FedViews. FRB San Francisco, November 30.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org