The business practice of adjusting prices using algorithms powered by artificial intelligence—known as AI pricing—has grown rapidly and spread across many sectors in the economy. Unlike traditional price setting, AI pricing uses predictive analysis of large data sets to incorporate real-time changes in supply and demand conditions into pricing decisions. This enables businesses to adjust prices more quickly in response to unexpected changes in market conditions and monetary policy. Industry-level evidence suggests that price adjustments are more sensitive to monetary policy in sectors where AI pricing is more prevalent.

When you book a flight, reserve a hotel room, or shop online, the quoted prices may vary depending on the day and time of your search or even the platform used for the search. Companies are increasingly using advanced algorithms powered by artificial intelligence (AI) for setting such prices. AI pricing enables companies to adjust their product prices more rapidly in response to changes in supply and demand conditions. Thus, the rise of AI pricing, if widespread in the economy, could fundamentally change the effectiveness of monetary policy in stabilizing inflation and employment fluctuations. For example, if policy tightening leads to larger drops in inflation because of widespread usage of AI for pricing, then the policy would have smaller impacts on employment and production.

This Economic Letter documents some facts about the recent developments in business adoption of AI pricing based on online job postings data. The data suggest that AI pricing adoption has grown rapidly during the past decade, and its adoption has spread across many sectors in the economy. There is also evidence that prices are more sensitive to changes in monetary policy in sectors where AI pricing is more prevalent.

The rise of AI pricing

Studying the economic impact of AI pricing requires reliable data sources that cover a broad set of firms and sectors in the economy. Since we do not have direct information that helps measure firms’ adoption of AI pricing, we construct a proxy for AI pricing adoption using online U.S. job postings data from Lightcast, a data set that covers online job postings in the entire economy from 2010 onward. The idea is that, if a firm posts a job that requires AI pricing skills, then the firm is likely an adopter of AI pricing or plans to adopt it.

Following Adams et al. (2026), we use a two-step procedure to identify job postings that require skills related to AI pricing. First, we identify jobs that require AI-related skills using the textual analysis approach of Acemoglu et al. (2022), focusing on advanced technologies such as machine learning, cloud computing, and AI chatbots. Second, within the categories of AI-related jobs, we identify pricing jobs by searching for the keyword “pricing” in the job titles, skill requirements, and job descriptions. An AI pricing job is one that both requires AI-related skills and contains the keyword “pricing.”

We are primarily interested in studying how the adoption of AI pricing might affect price adjustments following a change in monetary policy. For this purpose, we compute the share of AI pricing jobs posted by each publicly traded firm. Since we do not have firm-level price data, we use industry-level price indexes for our analysis. Accordingly, we add up the number of AI pricing jobs posted by all firms within each industry to obtain an industry-level indicator of AI pricing adoption.

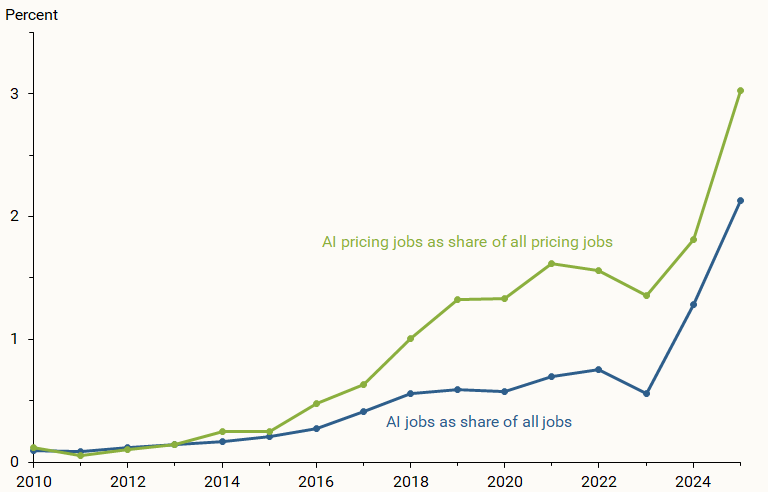

Figure 1 shows AI pricing jobs as a share of all pricing jobs (green line) in our sample from 2010 to 2025. The share surged from 0.12% in 2010 to 3% in 2025, with accelerated growth after 2015. Despite rapid growth, the share of AI pricing jobs remains modest, reaching about 3% by 2025. The post-2015 accelerated growth of AI pricing was accompanied by a similar accelerated growth of overall AI job postings (blue line). As a result, AI pricing jobs as a share of all AI jobs remained stable. During the same period, the share of pricing jobs in all jobs fell about 40%, potentially reflecting the job displacement effects of AI pricing (see, for example, Adams, Liu, and Miller 2026).

Figure 1

Shares of AI job postings and AI pricing job postings

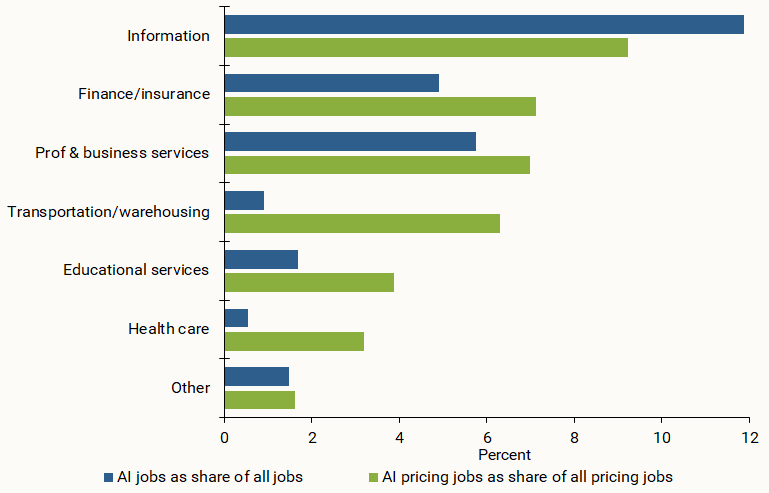

Figure 2 shows a snapshot of the cross-industry distribution of AI pricing adoption (green bars) and AI adoption (blue bars), as proxied by the shares of job postings in 2025. While AI adoption was concentrated in a few sectors such as information technologies, finance and insurance, and professional and business services, AI pricing adoption was more widespread, extending to sectors such as transportation, education, and health care. The figure also shows that the shares of AI pricing job postings vary substantially across industries.

Figure 2

Industry-level shares of AI pricing jobs and AI jobs, 2025

Source: Lightcast and authors’ calculations.

AI pricing and effects of monetary policy

AI pricing can be used by companies to customize their product prices for different consumers and thereby raise profit margins (see Adams et al. 2026 for a detailed discussion). AI pricing can also enable companies to adjust their prices more frequently in response to changes in market conditions and monetary policy.

We examine whether AI pricing has led to larger price adjustments following changes in monetary policy. For this purpose, we combine our online job posting data with industry-level price indexes from the Bureau of Economic Analysis (BEA), along with a measure of monetary policy surprises developed by Bauer and Swanson (2023). The Bauer-Swanson methodology identifies unexpected changes in monetary policy, so-called surprises, by analyzing high-frequency changes in financial market indicators within narrow windows surrounding Federal Open Market Committee (FOMC) announcements. The underlying principle is straightforward: If a policy change were fully anticipated, financial markets would remain stable following the announcements; conversely, market reactions would indicate unanticipated effects (or surprises) of policy announcements. Following Bauer and Swanson’s approach, we further refine the surprise measure by removing the influence of predictive macroeconomic and financial variables. We use the resulting quarterly time series to measure unexpected monetary policy changes, with a sample period from the first quarter of 2010 to the fourth quarter of 2019.

We then compare the responses of price adjustments to monetary policy surprises across industries with different shares of AI pricing job postings. For this purpose, we use a local projections model—a statistical tool proposed by Jordà (2005)—to estimate how the price level of an industry responds over time to a tightening of monetary policy that is equivalent to a 1 percentage point unanticipated increase in the federal funds rate in a given quarter. We compare the price responses for industries with low and high AI pricing adoption rates, as proxied by the job postings. The model takes into account how unexpected monetary policy changes interact with other macroeconomic variables.

In the final step, we measure the response of the industry price index relative to its pre-shock level each quarter over a period up to 12 quarters after the initial increase in the federal funds rate. We compare those responses across industries with different shares of AI pricing job postings.

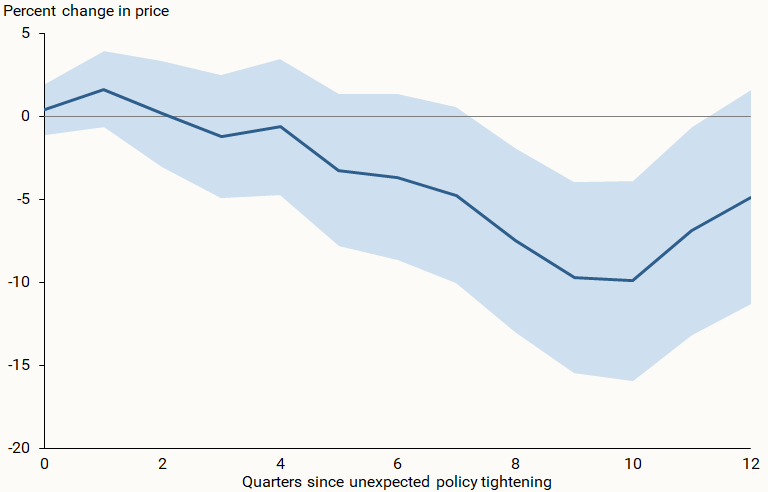

The solid line in Figure 3 shows the effects of an unanticipated tightening of monetary policy on the price index in an industry with an above average share of AI job postings relative to that in an industry with an average share. The shaded area shows the confidence band, which contains the responses to the monetary policy tightening 90% of the time, indicating the statistical uncertainty around the estimates.

Figure 3

Monetary policy tightening effects on industry-level prices

Source: Lightcast, BEA, and authors’ calculations.

The figure shows that, following a tightening of monetary policy, prices in an industry with an above average share of AI pricing decline more than those in an industry with an average share. The relative responses of industry prices to the policy tightening are persistent and reach their largest impact about 10 quarters after the initial policy surprise. Following a monetary policy tightening that raises the federal funds rate by 1 percentage point, the estimated responses imply that the price index of an industry with a share of AI pricing jobs that is one standard deviation (1.7%) above average would fall an extra 0.17% at the two-year horizon, compared to an industry with an average share of AI pricing. This relative price response, although statistically significant, is economically small—which is perhaps not surprising because the AI pricing share remains small in our sample, despite its rapid growth over the past decade.

Conclusion

Online job postings data suggest that the adoption of AI pricing has grown rapidly over the past decade and been incorporated across a broad set of industries. The level of the AI pricing job share remains relatively small, although evidence suggests that this new pricing technology has already modestly increased the sensitivity of prices to unexpected monetary policy changes. If the adoption of AI pricing continues to grow, which is a likely scenario, it would effectively increase the flexibility of price adjustments and thereby amplify the effects of unexpected monetary policy changes on inflation.

References

Acemoglu, Daron, David Autor, Jonathon Hazell, and Pascual Restrepo. 2022. “Artificial Intelligence and Jobs: Evidence from Online Vacancies.” Journal of Labor Economics 40(S1), pp. S293–S340.

Adams, Jonathan, Min Fang, Zheng Liu, and Yajie Wang. 2026. “The Rise of AI Pricing: Trends, Driving Forces, and Implications for Firm Performance.” Journal of Monetary Economics 157(103875).

Adams, Jonathan, Zheng Liu, and Sydney Miller. 2026. “Who Uses AI for Pricing?” Federal Reserve Bank of Kansas City Economic Bulletin (January 7).

Bauer, Michael D., and Eric T. Swanson. 2023. “A Reassessment of Monetary Policy Surprises and High-Frequency Identification.” NBER Macroeconomics Annual 37(1), pp. 87–155.

Jordà, Òscar. 2005. “Estimation and Inference of Impulse Responses by Local Projections.” American Economic Review 95(1), pp. 161–182.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org