Download PDF (pdf, 618 kb)

Introduction

The public’s demand for cash continues to grow as the amount of currency in circulation reached $1.43 trillion in October 2016. In addition, data from the Federal Reserve’s Diary of Consumer Payment Choice (DCPC) shows that cash remains the most frequently used payment instrument accounting for 31 percent of all consumer transactions. Developed by the Federal Reserve Bank of Boston in collaboration with the Federal Reserve Banks of San Francisco and Richmond, this study provides a unique view into consumer shopping and payment decisions, including their use of cash.1 Preliminary analysis of the 2016 DCPC data indicates that:

- Most consumer payments are for small value transactions, and cash predominates these small value payments. Approximately 60 percent of in-person payments under $10 were made in cash, compared to 20 percent of in-person transactions for $25 or more.

- Cash is held and used by a large majority of consumers, regardless of age and income; however, how it is used varies across demographic groups.

- Consumers’ opportunities to use cash are limited to in-person transactions for the most part. In 2016, only 75 percent of all payments were conducted in person.

This FedNotes uses preliminary findings from the 2016 DCPC to dig deeper into who uses cash and why. The paper is organized in four sections: Section 1 provides an overview of aggregate demand for cash; Section 2 reports on transaction shares by payment instrument; Section 3 reports on payment instrument use by demographic characteristics; and Section 4 discusses the implications of changing shopping patterns.

Section 1. Demand for currency is growing, particularly as a store of value

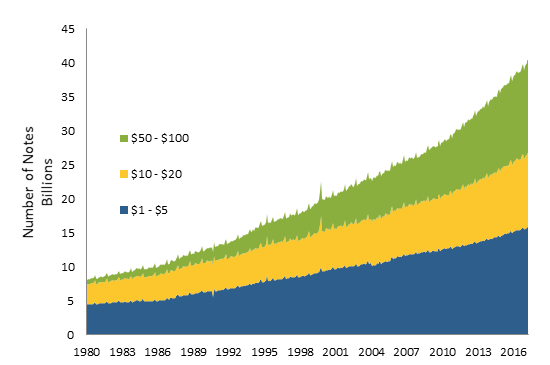

As highlighted in a recent posting by Federal Reserve Bank of San Francisco President John Williams,2 demand for cash is on the rise, both in the United States and across the globe. Figure 1 shows the growing demand for all denominations of U.S. notes, with particularly strong demand for high value denominations. Since 2009, the compound annual growth rate (CAGR) for the number of notes in circulation has been 5.6 percent, with the value of currency in circulation growing at a 7.4 percent annual growth rate.3

Figure 1

Number of Notes in Circulation by Denomination

The growth of currency in circulation is driven by both international and domestic demand for cash. In both of these markets, cash can be used as a payment instrument and as a store of value. Store of value demand for $50 and $100 denominations is greater in the international market, and payment instrument demand for the $1 through $20 denominations is greater domestically. While most $100s are held internationally, the majority of currency shipments to and from the Federal Reserve Banks are destined for the domestic market. Yet, determining which consumers are using cash and for what purpose—store of value or transactional use—cannot be ascertained from aggregate volume / value data alone. To better understand how consumers use cash, data at the payment level is needed.

Section 2. Cash is widely used, and heavily used for smaller purchases

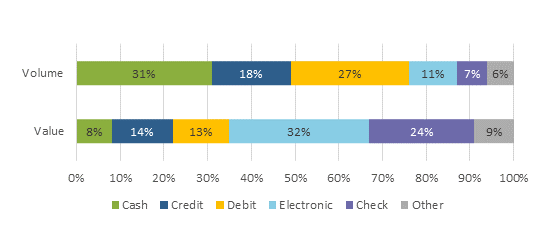

As in prior years, results from the DCPC indicate that by volume of transactions cash was the most used payment instrument in 2016, ahead of both debit and credit cards. Figure 2 shows the estimated aggregate volume and value shares of all payments (including bill payments and non-bill payments) from the 2016 DCPC. This includes cash, check, credit cards, debit cards, other electronic payments made through bank accounts, and other payments.4 On average, DCPC participants reported making 46 transactions per month, and used cash to pay for 14 of those transactions (31 percent). Debit and credit made up 27 and 18 percent respectively.

Figure 2

2016 Volume and Value Percent, by Payment Instrument

By value, the average cash transaction was approximately $22, while average debit card and credit card transactions were $44 and $57, respectively. Overall, cash payments accounted for eight percent of the average $4,000 that participants reported spending during the month, while debit accounted for 13 percent and credit card payments accounted for 14 percent.

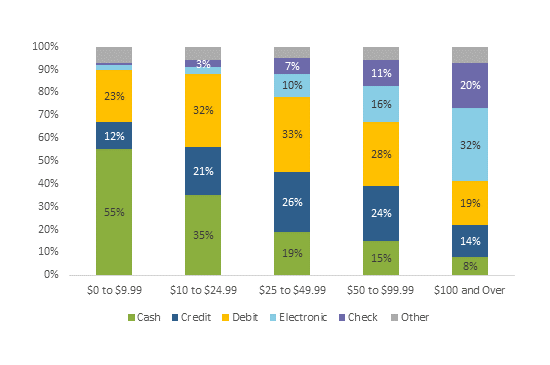

The value of the payment appears to influence whether a consumer chooses to use cash, debit, credit, or another form of payment. As shown in Figure 3, cash is used most often for payments less than $25, while credit and debit cards are used more frequently for payments valued between $25 and $100. Checks and electronic payments are used more frequently for transactions valued $100 and over. Since the majority of all consumer payments are for less than $25, cash is—overall—the most frequently used instrument.

Figure 3

Payment Use by Amount 2016

In addition to transactions, the DCPC asks individuals about their payment preferences.5 Importantly, individuals who stated a general preference for debit and credit cards when making “everyday” (non-bill) purchases frequently use cash for small value payments.

This shift away from their preferred method does not appear to be driven by merchant restrictions on card use for small value payments. Those preferring debit and credit cards reported that only 20 percent of their transactions under $10 were at merchants that did not accept cards for these transactions. Many of them also reported cash as their preferred payment method for transactions less than $10. If consumers who prefer cards are using them only because the merchant didn’t accept a card for their small-value transactions, it is unlikely they would have selected cash as their preference for these transactions (Figure 4).

Figure 4

Non-Bill Payment Preference

Section 3. Most consumers use cash, some more heavily than others

Not only is cash used frequently for small value and in-person purchases, it is also used by a wide array of consumers. The data on cash use by household income provides two main insights. First, consumers make—on average—14 cash transactions per month, regardless of household income. It is also noteworthy that cash was the most, or second most, used payment instrument regardless of household income, indicating that its value to consumers as a payment instrument was not limited to lower income households that may be less likely to have access to an account at a financial institution.

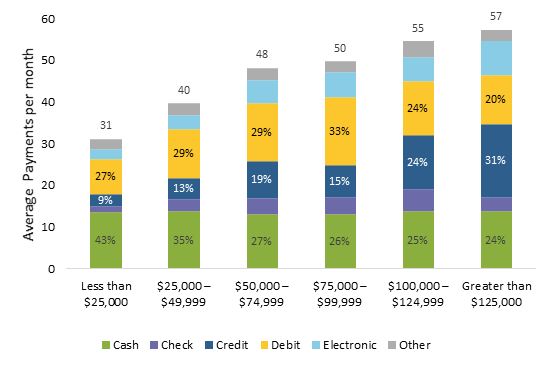

At the same time, it is also clear from Figure 5 that households with an annual income of less than $50,000 per year rely more heavily on cash than do higher income groups. Households earning less than $50,000 per year have considerably fewer transactions overall and, as a result, their cash transactions make up a larger share of their total—8 to 16 percentage points higher than those making more than $50,000.

Figure 5

Payment Instrument Use by Household Income

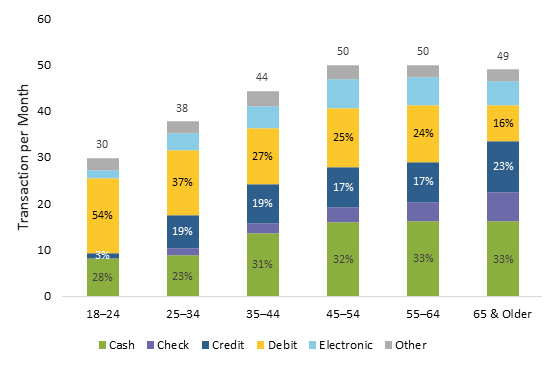

Similar to household income, all age groups use cash (Figure 6). By absolute number of transactions, individuals under 35 years-of-age use cash less than those over 35, with the number of cash payments equaling approximately 9 and 16 transactions per month, respectively. However, after controlling for the differences in the number of transactions across age groups, the intensity of cash use is somewhat more consistent across age groups.

Figure 6

Payment Instrument Use by Age Group

While cash use as a payment instrument is an important indicator of the demand for cash, understanding how DCPC respondents chose to hold cash provides further insight. On the evening before the start of their DCPC period and at the end of each survey day, participants reported their available cash on-hand, which provided four data points for each diarist on their cash holdings: the night before the DCPC started and at the end of each survey day.

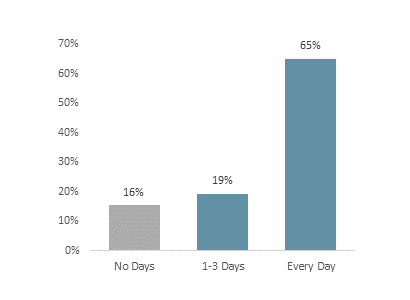

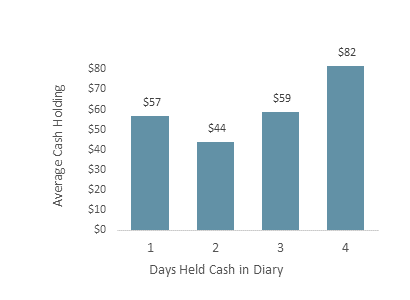

Even when participants were not using cash as their primary payment instrument, many held cash, potentially as a secondary payment option. Based on responses, nearly 85 percent of participants held cash at the end of at least one DCPC day (Figure 7), with the average value of those holdings being nearly $59. However, only 55 percent of participants used cash during their assigned three-day survey period. Of those individuals who held cash in their purse, wallet, or pocket at the end of the night, only 63 percent used cash in a transaction.

Figure 7

Cash Holding Frequency

Figure 8

Average Cash Holding

Of the participants who did not report holding cash at the end of the survey day, approximately 15 percent used cash for one or more payments. In these instances, individuals withdrew and used the cash over the course of the day. The DCPC results suggest that some individuals withdraw and hold cash with an option to spend it, others withdraw cash for specific circumstances or merchants, and some withdraw and use only the cash they need for the day.

Section 4. Shopping trends are putting downward pressure on cash use

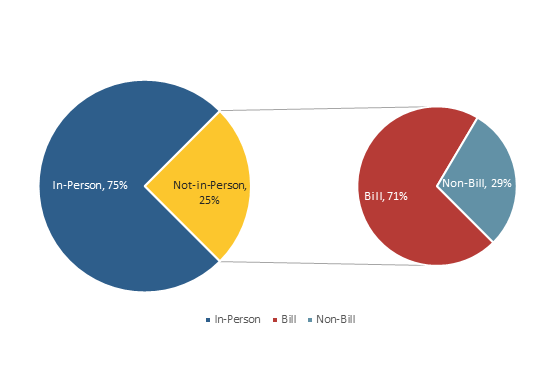

Technological developments and the continued growth of electronic and mobile commerce are changing consumers shopping and payment habits. Because of these changing habits, an additional factor influencing cash use is whether the consumers make payments either in-person or not-in-person. When consumers choose to shop online, or not-in-person, using cash is almost never an option. As consumer payment locations change, it adds an additional dimension to understanding how cash is used. Some examples of in-person payments include brick-and-mortar stores, vending machines, parking meters, and taxis; examples of not-in-person transactions include online purchases or checks made for bill payments.6

DCPC data show approximately 75 percent of purchases took place in person. For those 25 percent of purchases that are not-in-person, over 70 percent are bill payments. Given that most bill payments are not made with cash—even when they are made in person—the impact on cash transactions volume is probably more muted than if non-bill payments were driving the rising share of not-in-person purchases. This suggests that increased online payments are causing downward pressure on cash use, but it is not nearly as high as if the percent of non-bill transactions made up a greater portion of not-in-person transactions.

Figure 9

Type Shopping by Location

Conclusion

Cash continues to play an important role in our society. Not only is the value of currency in circulation rising faster than gross domestic product (GDP), but cash was the most used payment instrument by transaction volume in the 2016 DCPC study. Cash use is not limited to a specific population; it is used by young and old, rich and poor.

In the digital age, cash use remains resilient, not because of a lack of payment instrument options, but rather because it is used and preferred by a range of individuals across age and household incomes, specifically for small value transactions as well as a back-up payment instrument. Recent events have reminded us of nature’s destructive powers and the limits of electronic payments in times of crisis. During these times, the need for cash is great. As long as the public continues to demand, use, and hold cash, the Federal Reserve will continue to meet that demand.

About the Cash Product Office

As the nation’s central bank, the Federal Reserve ensures that cash is available when and where it is needed, including in times of crisis and business disruption, by providing FedCash® Services to depository institutions and, through them, to the general public. In fulfilling this role, the Fed’s primary responsibility is to maintain public confidence in the integrity and availability of U.S. currency.

The Federal Reserve System’s Cash Product Office (CPO) provides strategic leadership for this key function by formulating and implementing service level policies, operational guidance, and technology strategies for U.S. currency and coin services provided by Federal Reserve Banks nationally and internationally. In addition to guiding policies and procedures, the CPO establishes budget guidance for FedCash® Services, provides support for Federal Reserve currency and coin inventory management, and supports business continuity planning at the supply chain level. It also conducts market research and works directly with financial institutions and retailers to analyze trends in cash usage.

Diary of Consumer Payment Choice

The Federal Reserve’s national Cash Product Office (CPO) studies data from the Diary of Consumer Payment Choice (DCPC) to understand consumer cash use and anticipate its ongoing role in the payments landscape. Developed by the Federal Reserve Bank of Boston’s Consumer Payment Research Center (CPRC), the DCPC includes a unique dataset and is a nationally representative survey of consumer shopping and payment decisions.7 By tracking consumer payment transactions and preferences during a designated three-day survey period, the CPO compares cash with other payment instruments, such as debit and credit cards, checks, and electronic options. DCPC participants also report the amount of cash on-hand after each survey day, as well as whether they deposited or withdrew cash throughout the day. The CPO analyzes the DCPC data, including the impact of age and income on an individual’s payment behavior and preferences. This detail of the stock and flow of cash at an individual level provides insight into how consumers use cash.

Administered by the University of Southern California Dornsife Center for Economic and Social Research, the Understanding America Study is a panel of approximately 6,000 individuals from across the United States, of which 2,848 panelists completed the DCPC. Using the Census Bureau’s Current Population Survey, responses were weighted to match national population estimates. Similar to the 2012 DCPC, the month of October was selected as a “typical month” to minimize seasonality effects in consumer spending patterns. Diarists were each assigned a consecutive three-day period that was staggered over the month, ensuring a roughly equal number of participants on each day.

Footnotes

1. See the forthcoming Federal Reserve Bank of Boston Research Data Report on “The 2016 Diary of Consumer Payment Choice.”

2. Reports of the Death of Cash are Greatly Exaggerated, SF Fed Blog, FRBSF.org – November 2017

3. The annual growth rate for both the number of notes in circulation and the value of notes in circulation calculation used the compound annual growth rate (CAGR).

4. Other payments include money orders, traveler’s checks, PayPal, Venmo, and text message payments.

5. Individuals are asked about their primary and back-up payment preferences for non-bill payments, as well as their primary preference for bill payments, online payments, and in-person payments by amount.

6. Shopping Experience Trends and their Impact on Cash, FedNotes, FRBSF.org – April 2016

7. DCPC participants are weighted representative by age, household income, and ethnicity.