Kevin J. Lansing, research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of February 11, 2016.

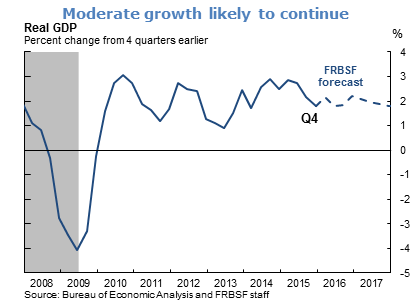

- Real GDP growth slowed in the fourth quarter of 2015 to less than 1% at an annual rate. Declines in business investment, inventories, and net exports were offset by solid increases in personal consumption expenditures and residential investment. For 2015 as a whole, real GDP growth was 1.8%, slightly below the average annual growth rate of 2.1% observed since the Great Recession ended.

- We expect real GDP growth to pick up in 2016 and then ease to trend by the end of 2017. Downside risks to the U.S. growth outlook include possible spillovers from economic slowdowns in foreign markets and a continued strengthening of the U.S. dollar which would pose a headwind for net exports.

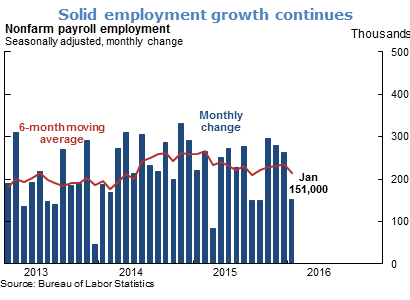

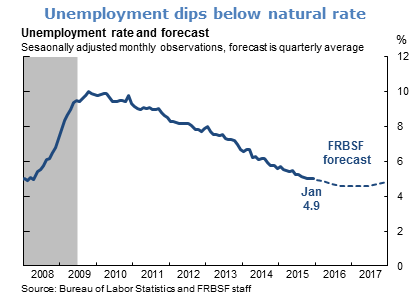

- Payroll employment increased by 151,000 jobs in January, signaling continued improvements in the labor market. The six-month moving average remains above 200,000 new jobs per month. The unemployment rate dipped to 4.9% in January, which is slightly below the level that we judge to be the natural rate of unemployment.

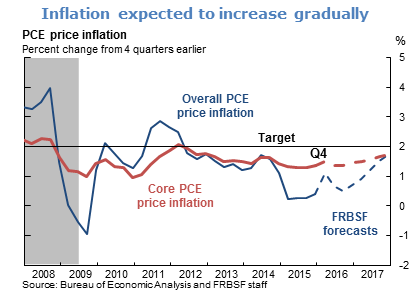

- Inflation as measured by the four-quarter change in the personal consumption expenditures (PCE) price index has remained below the Federal Open Market Committee’s (FOMC) 2% target since mid-2012. Absent further declines in energy prices or a further strengthening of the U.S. dollar, we would expect PCE inflation to rise gradually towards 2% as economic slack continues to dissipate.

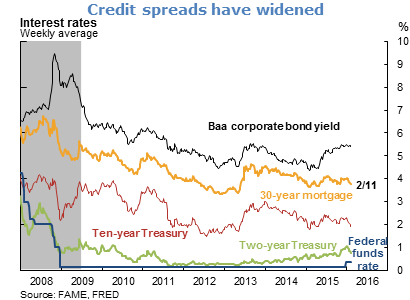

- Treasury yields have declined recently reflecting a “flight-to-safety” in response to investor concerns about economic slowdowns in foreign economies and the prospect that such events could have negative spillovers for U.S. growth. Since May 2015, the yield spread between Baa-rated corporate bonds and 10-year Treasury bonds has widened by nearly 100 basis points, indicating that corporate bondholders are demanding more compensation for exposure to credit risk.

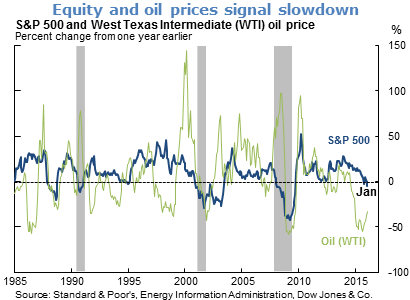

- Recent declines in the Standard & Poor’s (S&P) 500 have caused the index to dip below levels that prevailed one year ago. Over the same time frame, oil prices have dropped precipitously to levels last observed in 2002. Historically, U.S. recessions have often been associated with oil price spikes, but not sharp declines. The recent contemporaneous drop in stock prices suggests that equity market investors are interpreting lower oil prices as a signal of slowing global growth—a development that would have negative consequences for future corporate profits.

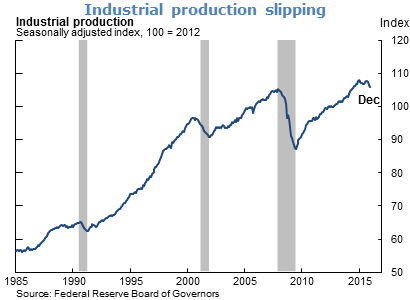

- The Federal Reserve Board’s index of industrial production has recorded three consecutive monthly declines, mainly reflecting production slowdowns in the energy sector. Still, the December 2015 reading is only about 1% below the prior peak recorded in September 2015.

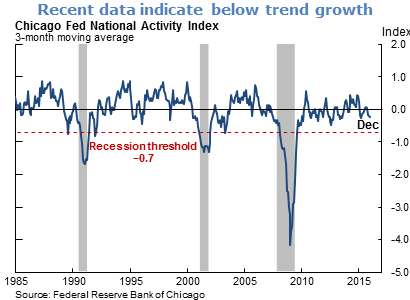

- The Chicago Fed National Activity Index (CFNAI) has proved useful as an early indicator of recessions. It is distilled from 85 monthly series drawn from four broad data categories: consumption and housing; employment, unemployment, and hours worked; sales, orders, and inventories; and production and income. The index is constructed to have an average value of zero, with a positive reading indicating growth above trend and a negative reading indicating growth below trend. The three-month moving average CFNAI is currently at –0.24, well above the threshold of –0.7 that has typically signaled the onset of a recession. But as a caveat, it should be noted that the index has often dropped quickly in the months leading up to past downturns. For example, the index stood at –0.2 in July 2007, only five months before the start of the Great Recession.

- Few, if any, past recessions have been successfully predicted by professional forecasters. Forecasting recessions is difficult because each one tends to differ in important ways from previous episodes. Past recessions have been triggered by upward spiking oil prices, increases in policy interest rates designed to bring down high inflation, and bursting asset price bubbles. None of these scenarios would seem to fit the present circumstances.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.