Thomas M. Mertens, research advisor at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of August 10, 2017.

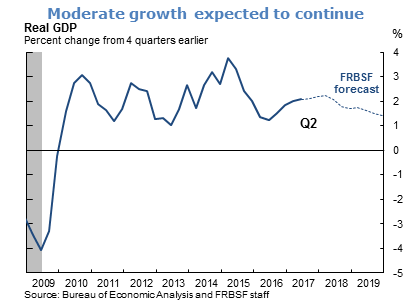

- The U.S. economy continues to grow at a moderate pace. After a relatively weak first quarter with real GDP growing at an annualized rate of 1.2%, the economy in the second quarter rebounded, growing at 2.6%, supported by robust consumer spending as well as greater inventory investment. We expect output growth to average about 2% for 2017, followed by a gradual transition over the next two years back to our estimate for potential output growth of 1½ to 1¾%.

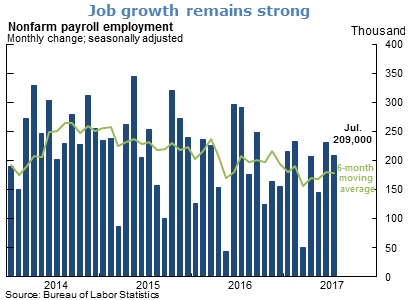

- Ongoing moderate economic growth has been accompanied by further strengthening of the labor market which appears to be at or even beyond full employment. Nonfarm payroll employment increased by 209,000 in July, and gains have averaged about 180,000 over the past six months. This pace of job creation is well above the rate necessary to absorb new entrants into the labor force, which we estimate at around 80,000 to 100,000 jobs per month.

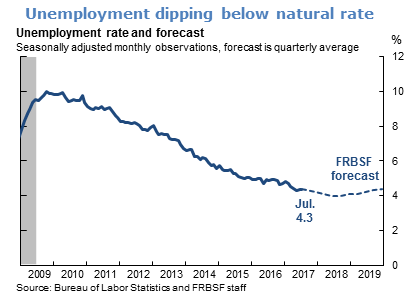

- The unemployment rate fell to 4.3% in July, after having ticked up a touch in June. The current reading reflects the robust pace of job creation and is below our estimate of the natural rate of unemployment which we put at 4.8%. Over the medium term, we expect the unemployment rate to gradually revert towards its natural rate.

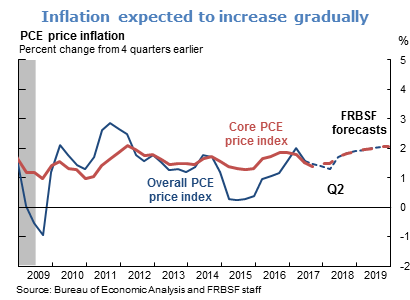

- Inflation remains below the target rate of 2% set by the Federal Open Market Committee (FOMC). The price index for overall personal consumption expenditure (PCE) grew at a rate of 1.6% over the previous year, while core PCE rose by 1.5%. Transitory factors and one-time price reductions are holding down inflation, and will continue to dampen annual inflation numbers until they fall out of the 12-month window. Supported by the strong fundamentals of the overall economy, we expect inflation to move towards the target rate of 2% over the medium term.

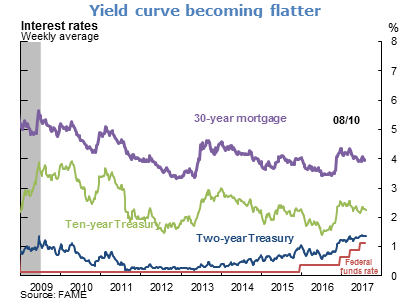

- Financial conditions continue to ease and remain accommodative. The yield curve has continued to flatten since the beginning of the year, with the two-year Treasury bill yield increasing by 14 basis points (bps), and the 10-year Treasury yield decreasing by 19 bps.

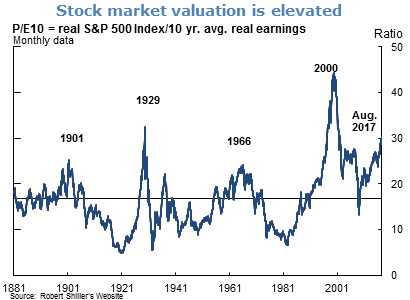

- Valuation measures for U.S. equities are high relative to historical benchmarks. A prominent measure, the price-earnings ratio, measured as the real S&P 500 index divided by the ten-year average of real corporate earnings, currently stands above 30, substantially higher than the historical average of about 17. In the past, this measure has deviated from its historical average for prolonged periods, often peaking before economic recessions, but eventually reverting towards the average. One factor that may explain why it is now elevated is that the currently low level of long-term interest rates implies a lower discounting of future corporate cash flows and thus higher valuations of equities. Another possible factor is that the current ten-year average of earnings is suppressed since it reflects the weak performance of firms during the Great Recession of 2007-2009 along with the subsequent recovery. However, moderate economic growth prospects over the medium-term provide an argument against elevated equity valuations. Furthermore, higher price-earnings ratios have tended to predict low future price growth or even price declines over the following ten-year period.

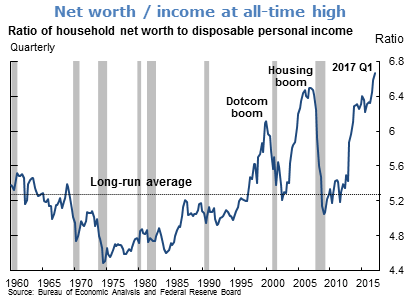

- The ratio of household net worth to disposable personal income provides a valuation measure of for a broader set of asset classes. Household net worth, which depends on the value of bonds and real estate as well as equities, has risen faster than disposable income in recent years, as equity values and also long-term bond and housing prices have been increasing. Currently, the ratio of household net worth to disposable personal income stands at a record high of about 6.7, compared to its historical average of 5.3 since 1960. Similar to the price-earnings ratio, this valuation measure tends to revert back to its historical average. However, valuation measures are noisy signals of trends in financial markets and the economy and need to be combined with other available data.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.