Michael Bauer, economist at the Federal Reserve Bank of San Francisco, states his views on the current economy and the outlook.

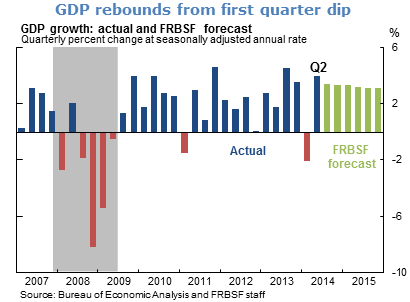

- Real GDP rebounded strongly in the second quarter of 2014, as expected. This followed an anomalous dip in the first quarter caused mainly by transitory factors such as unusually severe winter weather. The increase in real output was broad-based, with gains in consumer spending, investment, government expenditures, and exports. We expect steady growth through 2015, at an average annual rate slightly above 3%.

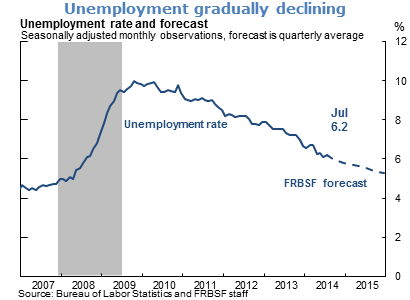

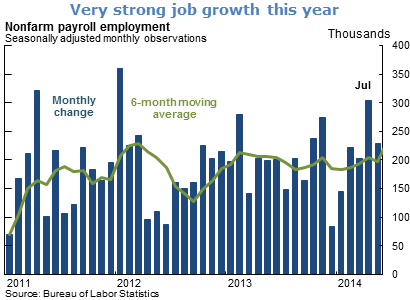

- Conditions in labor markets have improved further, also in line with our expectations. The unemployment rate continued its downward trend throughout the first part of the year. A slight uptick in July was due to an increase in the number of people starting to look for jobs again, that is, increasing labor market participation, which we see as a positive sign. Strong job creation has been another encouraging sign that the labor market is healing. Despite these improvements, which we expect to continue, other indicators suggest there is still a significant amount of slack in the labor market. Importantly, wage growth remains subdued, indicating that the economy is not yet close to full employment.

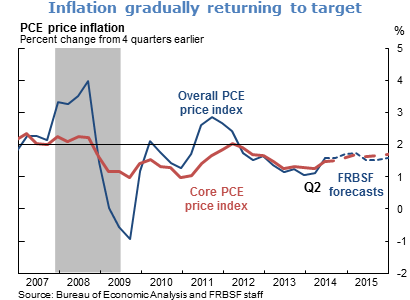

- Broader trends in inflation suggest it is gradually approaching the Federal Open Market Committee’s long-run objective of 2%. Inflation data in the second quarter came in slightly higher than earlier in the year, but most of the increases were in categories with volatile prices. As a result, these numbers probably overstate the true rate somewhat. Hence we expect inflation to moderate in the second half of this year and then gradually increase toward levels consistent with the FOMC’s objective.

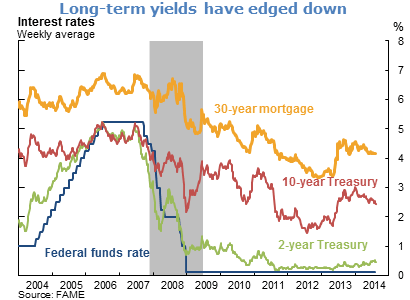

- Financial conditions have been highly supportive of continued growth in the economy. In particular, long-term interest rates receded over the first half of this year, which should further encourage consumer spending, the recovery in the housing market, and business investment.

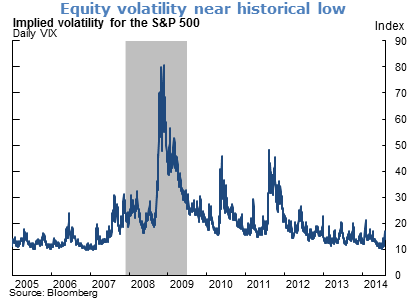

- The stability of the financial system is fundamental for a healthy, growing economy. One aspect of financial stability is the soundness of asset markets, reflected in indicators such as valuations, volatility of market prices, and investor leverage. Recently, there have been concerns about the stability in some equity and bond markets. Valuations in certain segments of equity markets appear stretched relative to fundamentals. And in the market for risky corporate debt—the high-yield bond market—spreads of interest rates over those of safe Treasury bonds have been very low relative to the historical average.

- Importantly, volatility in equity markets has been near historically low levels as indicated by the level of the VIX, an index that measures the volatility of Standard & Poor’s 500 equity index using option prices. It is sometimes nicknamed the “investor fear gauge” since it reflects the anxiety of equity investors. Currently, the VIX is well below its historical average. One interpretation is that investors have not been very worried about risks to the economic outlook. The picture is similar in bond markets, where volatility is currently quite low as well.

- This low volatility environment contrasts with significant risks to the economic outlook, such as geopolitical turmoil in the Middle East, a potential property bust in China, and deflation and stagnation in Europe, to name a few. Investors currently appear to be complacent about these risks.

- This apparent investor complacency could result in abrupt reversals of financial asset prices and spikes in volatility in response to unexpected developments. However, we believe that such changes in asset prices would not substantially tighten overall financial conditions and therefore should have only limited effects on the economy.

- The reason is that, overall, the financial system appears to be on solid footing. For example, banks’ capital ratios have improved, the degree of leverage in the financial sector is relatively low, and there is ample liquidity available in the system. Still, although we are not overly concerned about the low volatility environment in financial markets at this time, we will continue to carefully monitor the health of asset markets for signs of distress.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.