Sylvain Leduc, executive vice president and director of research at the Federal Reserve Bank of San Francisco, stated his views on the current economy and the outlook as of September 8, 2022.

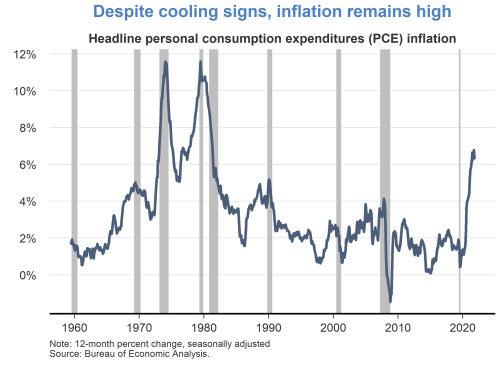

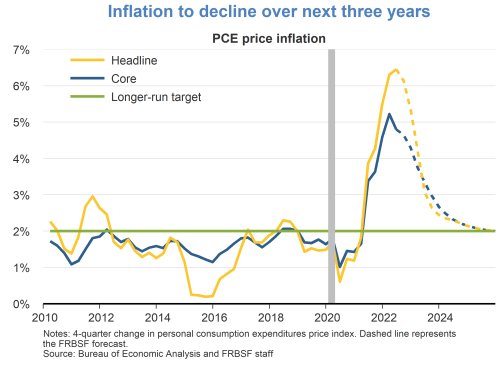

- While inflation continues to be very high, inflationary pressures moderated somewhat in July. Helped by recent declines in crude oil prices, the 12-month change in the headline personal consumption expenditures (PCE) price index declined to 6.3%, a 0.5 percentage point drop compared to June. Core PCE inflation, which removes food and energy prices, also declined, though more modestly.

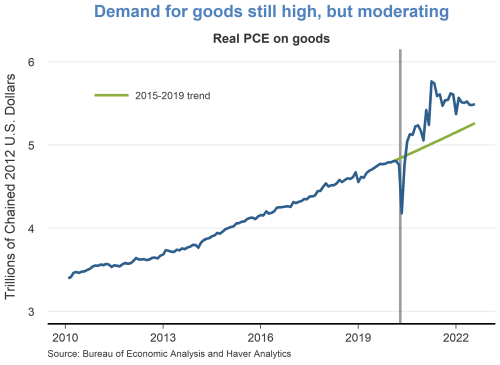

- The economy is continuing to rebalance toward more typical spending patterns. As consumers had avoided close contact activities during the early stages of the pandemic, particularly those in the services sector, because of health concerns during the spread of the coronavirus, goods consumption jumped substantially above its pre-pandemic trend at the onset of the recovery.

- In particular, durable goods, such as cars, electronics, appliances, and furniture, experienced a surge in demand, which reversed roughly 20 years of deflation in that sector arising from the effects of globalization and technological improvements. The resulting rise in durable goods price inflation contributed to the overall inflationary pressures experienced since the middle of 2021, alongside generous fiscal support and accommodative monetary policy. However, since the start of the year, durables inflation has been moderating, declining from 11.5% in January to 5.6% in July from 12 months earlier, as consumers rebalance their spending patterns.

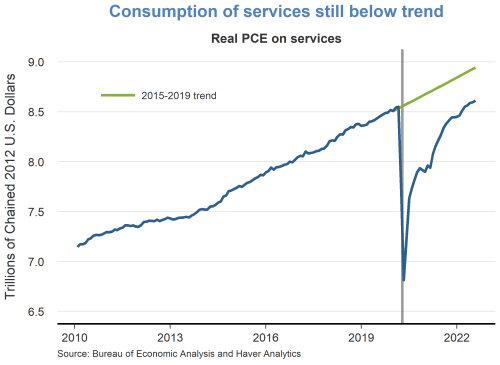

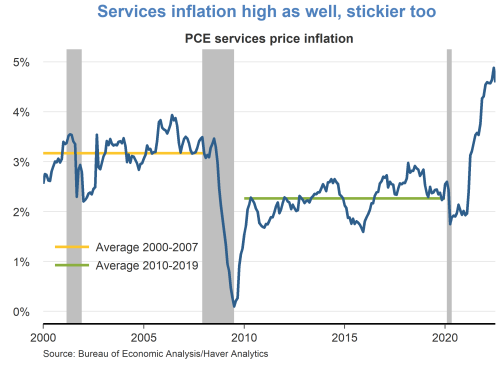

- Correspondingly, consumption of services is steadily rising back to levels more in line with the pre-pandemic trend. The increase in services consumption has contributed to services price inflation at a rate greater than that during the recovery from the Great Recession or the preceding period in the 2000s. Part of the increase in services inflation is due to the large increase in house prices since the onset of the pandemic, which, as our earlier research shows, spilled over to rent inflation, an important component of the services price index, with a lag. While house price growth has moderated recently, house prices, as of June, are still rising more than 15% year-on-year, which should keep rent inflation high over the medium run, given that the spillovers from house price increases to rent inflation tend to be persistent.

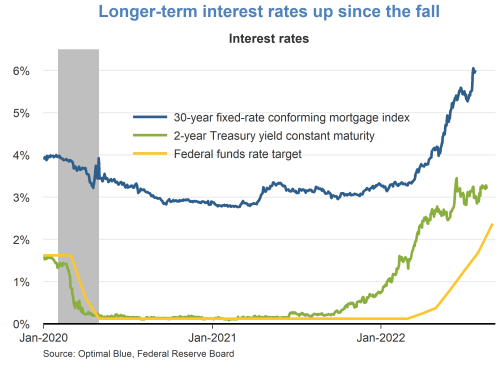

- Significantly higher mortgage rates underlie the recent moderation in house prices. With the increases in the federal funds rate since March and previous policy guidance on its expected future path, long-term mortgage rates have doubled since last fall to roughly 6%. Market participants are anticipating further tightening in monetary policy, with federal funds rate futures suggesting a rise to 4% by early 2023.

- Given a continued anticipated tightening in monetary policy stance and more restrictive financial conditions, we expect inflation to gradually decline toward the Federal Reserve’s 2% target. That said, the decline in inflation is expected to be gradual, reflecting the typical persistence in services inflation and lags in the effects of monetary policy. Overall, we expect inflation to be back at 2% by the beginning of 2025.

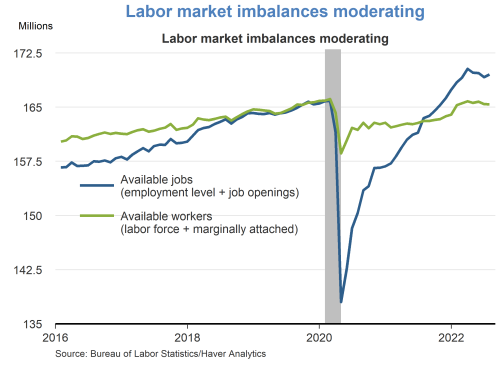

- To achieve this outcome, the Federal Reserve is facing a very challenging path. It aims to reduce inflation by inducing a more moderate pace of growth without triggering a recession. The pace of job creation stepped down last month, with businesses adding 315,000 new jobs in July and the unemployment rate ticking up to 3.7% from 3.5% in July. Most demographic groups have come close or have fully recovered the pandemic-induced job losses. While the imbalance in the labor market, as indicated by the total supply of available workers compared to the current demand, is shrinking a bit, it still remains notably large.

- Nominal wage growth continues to be strong, providing another indication of the economy’s strength. In August, wages, as measured by average hourly earnings, grew 5.2% from 12 months prior compared to roughly 3% in 2019 before the pandemic hit. Moreover, this aggregate number masks important sectoral movements. For instance, in the leisure and hospitality sector, wages are up 8.6% from a year earlier, reflecting continued difficulties finding workers.

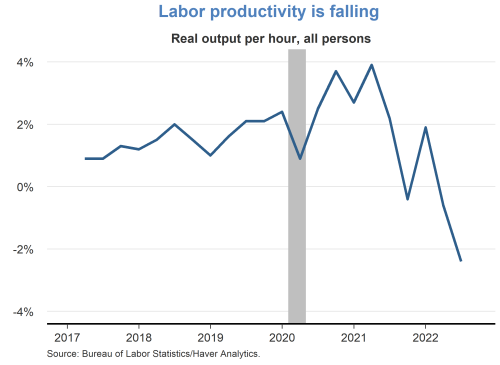

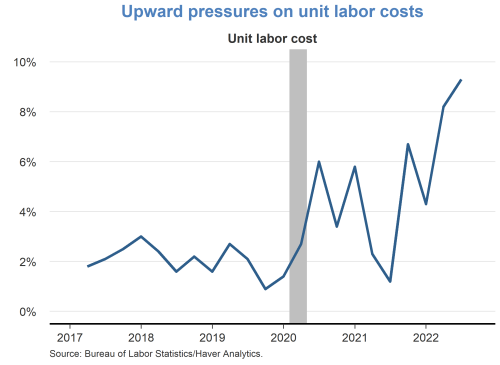

- One concern is that wage pressures are occurring while measured labor productivity is declining. As a result, unit labor costs are rising, which could translate into additional inflation if firms pass on these higher costs to consumers by raising prices. In addition, given the increase in inflation over the past year and the significant rise in households’ year-ahead inflation expectations during the same period, the pressure for higher compensation will continue to be strong to preserve real wages, that is, nominal wages adjusted for inflation, which have been falling dramatically for most workers.

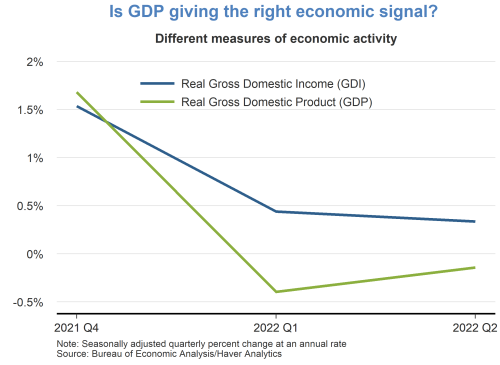

- The strength of the labor market appears at odds with the past two quarters of Gross Domestic Product (GDP) data, which suggest a contraction in economic activity. However, this tension may be due to data measurement issues. For instance, Gross Domestic Income (GDI), which measures economic activity using income data instead of data on expenditures as is the case for GDP, currently suggests a moderation in economic activity that is more in line with the evolution of the labor market than the contraction implied by GDP. Previous research suggests that data revisions tend to move GDP toward GDI. Following this pattern, revisions to second-quarter GDP suggest that the economy contracted less than initially reported.

- Similarly, financial markets do not fully appear to anticipate a recession in the near future, although the risk has clearly risen. Historically, a sustained and meaningful inversion in the yield curve is a good recession predictor. However, for the time being, the term spread between the 10-year and 3-month Treasury rates, our preferred recession indicator, remains positive.

- Overall, there are early signs that inflation is moderating and that the labor market is getting in better balance. But these are only first steps in what is likely to be a prolonged fight to bring inflation down. Importantly, households and market participants continue to expect the Federal Reserve to implement the appropriate policies to achieve this outcome. Indeed, while year-ahead inflation expectations are elevated, long-run expectations continue to fluctuate within normal ranges, consistent with the Fed’s price stability goal.

About the Author

Sylvain Leduc is executive vice president and director of Economic Research at the Federal Reserve Bank of San Francisco. Learn more about Sylvain Leduc

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.