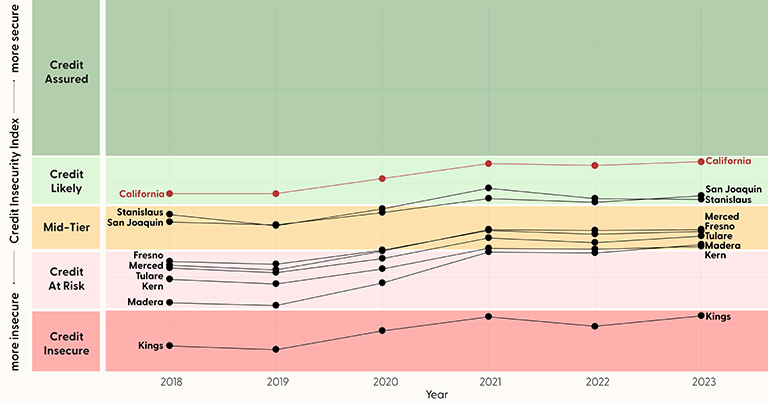

How can Federal Reserve data tools inform local practice? In February’s San Joaquin Valley Financial Empowerment convening—which brought together local practitioners, state agencies, and small business associations—the Community Engagement and Analysis team saw in real time how local data can spark action. When county‑level indicators from the Federal Reserve Bank of New York’s Credit Insecurity Index revealed that Kings County in the Central Valley of California lags behind its neighbors, those numbers immediately reframed the discussion in the room. The data shows that nearly 21% of Kings County adults have no credit file and about 13% are credit‑constrained. That insight helped participants identify Kings County as a near‑term opportunity for deeper outreach and engagement from the region’s Bank On initiative, which works to connect consumers to safe, affordable bank accounts.

What the Data Revealed About Regional Variation

Across California’s Central Valley, consumer debt is approaching 20‑year highs. Auto loans and credit card balances are rising the fastest, and delinquency remains concentrated among lower‑income borrowers. These patterns underscore what the Credit Insecurity Index1 highlights in Kings County: households already facing higher debt burdens are also those most likely to be absent from or constrained within the credit system.

To explore these trends where you live, the Federal Reserve Bank of Philadelphia offers the Consumer Credit Explorer, a tool showing how debt and delinquency vary across regions.

By layering these debt patterns with county‑level credit insecurity measures, a clear picture emerged: while many Central Valley counties have made modest progress since 2018, Kings County continues to experience some of the region’s highest rates of credit insecurity. This analysis brought into focus where targeted outreach could make a difference.

Figure 1. Credit Insecurity Trends Among Counties in California’s Central Valley

Local Financial Pressures Add Context

Financial constraints across the Central Valley point to the need for access to safe, low‑fee banking products. According to the University of Washington’s Self‑Sufficiency Standard,2 childcare, housing, and taxes together consume a substantial share of household budgets. For many families, these essential expenses leave little margin for financial shocks or high‑fee financial services. The goal of Bank On‑certified accounts is to provide a stabilizing tool by offering predictable, affordable banking options for households navigating volatile monthly budgets.

“A little bit of very local data can help surface something actionable.”

Leilani Barnett, Senior Outreach Manager, San Francisco Fed

Growing Momentum Through Bank On

Amid rising costs and credit pressures, Bank On participation across the Central Valley has been growing. According to the Federal Reserve Bank of St. Louis’s Bank On National Data Hub,3 Fresno, Kern, and San Joaquin counties each reached roughly 55,000 open accounts by the end of 2024, contributing to more than 262,000 open accounts across the region. Fresno alone added over 20,000 new accounts in 2024.

This growth is particularly meaningful when viewed alongside the cost‑of‑living pressures described above. As families work to meet basic needs, access to safe, low‑fee accounts helps avoid burdensome costs associated with high‑fee financial services and costly credit alternatives. That’s why partners at the convening recognized that extending Bank On outreach to Kings County is timely while also building on an established regional momentum that can help open new pathways to financial stability where credit insecurity remains elevated.

Bringing Local Data to Local Practitioners

The outcomes of the convening in Fresno provide a clear example of how place‑specific data, presented in the right setting, can inform local efforts. Maps and county‑level indicators made geographic disparities visible in ways that resonated immediately with the participants in the room. The data emphasized the need for more outreach in Kings County to ensure that the communities facing the highest credit insecurity are included in regional financial empowerment conversations.

Participants noted that credit insecurity in the region is not evenly distributed—it clusters in specific places, highlighting opportunities for more targeted outreach. When tools like the Credit Insecurity Index, the Consumer Credit Explorer, and the Bank On National Data Hub, are paired with local insight and cross‑sector collaboration, partners can identify opportunities that might otherwise remain hidden.

End Notes

1. Credit Insecurity in the United States: 2018–2023. Federal Reserve Bank of New York. https://www.newyorkfed.org/outreach-and-education/household-financial-stability/credit-insecurity-united-states

2. Self Sufficiency Standard. Center for Women’s Welfare University of Washington School of Social Work. https://selfsufficiencystandard.org/

3. Bank On National Data Hub. Federal Reserve Bank of St. Louis. https://www.stlouisfed.org/community-development/bank-on-national-data-hub

Community Engagement and Analysis works to understand the economic experiences of lower-income households and communities to help build a stronger economy for all Americans. This work contributes to the Federal Reserve Bank of San Francisco’s work to support monetary policy, strengthen financial institutions, and enhance payment systems.