Inflation rates in the United States and other developed economies have closely tracked each other historically. Problems with global supply chains and changes in spending patterns due to the COVID-19 pandemic have pushed up inflation worldwide. However, since the first half of 2021, U.S. inflation has increasingly outpaced inflation in other developed countries. Estimates suggest that fiscal support measures designed to counteract the severity of the pandemic’s economic effect may have contributed to this divergence by raising inflation about 3 percentage points by the end of 2021.

Download replication data zip file (373 KB)

Few people would question the devastating economic consequences of the COVID-19 pandemic, which resulted in a dramatic collapse in economic activity and loss in employment worldwide. The United States introduced unprecedented fiscal and monetary policy responses to provide rapid economic relief. The Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law in March 2020. In the same month, the Federal Reserve lowered the target range for the federal funds rate to 0–¼% and introduced additional measures to ease liquidity.

As we begin the third year since the start of the pandemic, the U.S. economy has rebounded at an astonishing rate. Unemployment recovered from a high of 14.7% in April 2020 to 3.8% in February 2022. Meanwhile, the gap between actual GDP and its potential rate has nearly closed to less than 0.5%, as calculated by the Congressional Budget Office. However, global supply chain distortions persist, and subsequent waves of COVID-19 infections continue to disrupt service-oriented industries.

There are many reasons to expect inflation to be higher than normal (Barnichon, Oliveira, and Shapiro 2021; Bianchi, Fisher, and Melosi 2021; Shapiro 2021a,b). In this Economic Letter we widen the recent analysis with an international comparison. Though many of the pandemic distortions are common to other countries, we show that U.S. inflation has risen more quickly and increasingly diverged from inflation in other OECD (Organisation for Economic Co-operation and Development) countries. In seeking an explanation, we turn to the combination of direct fiscal support introduced to counteract the economic devastation caused by the pandemic. Importantly, we trace the effect of these measures over time. The interplay between when assistance was delivered and how households responded to successive COVID waves created complicated dynamics in the economy. Building these dynamics into a simple model suggests that they may have contributed to about 3 percentage points of the rise in U.S. inflation through the end of 2021.

U.S. inflation is now higher than abroad

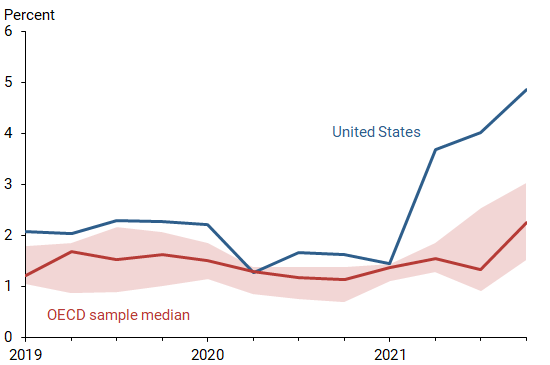

One way to illustrate what has happened with U.S. inflation is to compare it with the average rate of inflation across a group of OECD economies: Canada, Denmark, Finland, France, Germany, Netherlands, Norway, Sweden, and the United Kingdom. We rely on core inflation measures, which remove the more volatile food and energy prices. To align with what is available in all the countries in our study, we use consumer price index (CPI) inflation instead of the personal consumption expenditures price index, the preferred measure of inflation used by the Federal Reserve.

The blue line in Figure 1 displays the year-over-year percent changes in U.S. core CPI inflation. The figure also shows the median (red line) and the range between the 25% and 75% largest values (also known as the interquartile range and shown by the shaded area) of inflation for our OECD sample. A tighter range indicates that most OECD countries in our sample experienced inflation rates similar to each other. The figure shows that, before the pandemic, U.S. core CPI inflation remained, on average, about 1 percentage point above the OECD sample average. The small difference between U.S. and OECD inflation during this period is well known as many of the OECD countries struggled to get inflation up to target following the Global Financial Crisis and subsequent euro-area sovereign debt crisis.

Figure 1

Annual core CPI inflation: U.S. versus OECD

Note: Shaded area reflects interquartile range for OECD sample.

Source: OECD Household Dashboard: cross country comparisons.

By early 2021, however, U.S. inflation increasingly diverged from the other countries. U.S. core CPI grew from below 2% to above 4% and stayed elevated throughout 2021. In contrast, our OECD sample average increased at a more gradual rate from around 1% to 2.5% by the end of 2021. These differences in inflation readings cannot be explained by measurement issues.

U.S. direct fiscal transfers are also higher than abroad

While all countries have been affected by the COVID-19 pandemic, policy responses have varied considerably. Beyond efforts to limit the spread of the virus, the availability of testing, and vaccine distribution, how countries handled providing economic support differed primarily in terms of size and scope. It is difficult to tally the measures adopted across all countries. Even within the United States, different states had varying degrees of unemployment assistance, direct household transfers, child support, business loans, and other pandemic assistance programs.

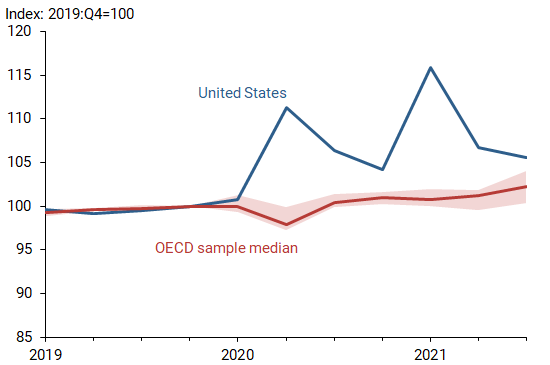

One way to get a read on this tangle of support programs is to directly measure disposable personal income in each country. This measures the amount individuals have left to spend or save after paying taxes and receiving government transfer payments. It is a relatively comparable measure across countries that incorporates the overall magnitude of net pandemic transfers.

Figure 2 shows an index for per capita inflation-adjusted disposable personal income—real disposable income, for short—for the United States and for the median and interquartile range across the sample of OECD economies. The figure shows that, throughout 2020 and 2021, U.S. households experienced significantly higher increases in their disposable income relative to their OECD peers.

Figure 2

Real personal disposable income: U.S. versus OECD

Note: Shaded area reflects interquartile range for OECD sample.

Source: OECD Household Dashboard: cross country comparisons.

Specifically, the two peaks in U.S. disposable personal income reflect the CARES Act, signed into law on March 27, 2020, and the American Rescue Plan (ARP) Act of 2021, signed about a year later. Both Acts resulted in an unprecedented injection of direct assistance with a relatively short duration. In contrast, real disposable personal income for our OECD sample increased only moderately during the pandemic.

Did more disposable income turn into more inflation?

Figures 1 and 2 suggest that the higher rate of inflation in the United States may relate in part to its stronger fiscal response. One way to assess the possible connection is using a Phillips curve framework.

In the Phillips curve, inflation is frequently expressed as a function of inflation expectations, lagged inflation, and a measure of a gap in economic activity. That is, inflation reflects a combination of the public’s views on future inflation, inflation inertia, and how hot the economy is running. Because of the array of policy measures introduced during the pandemic to counterbalance the economic effects of lockdowns, common labor market statistics, such as the unemployment gap, are not as reliable. Therefore, we turn to real disposable income to better capture the demand side of the economy. Moreover, the fiscal measures introduced to fight the pandemic were somewhat unexpected in that their passage, size, and scope were not known with certainty.

Using the Phillips curve logic, we can reasonably compute the effect of pandemic support measures on the inflation forecast. The idea is to compare countries that, like the United States, introduced aggressive support measures, which we call the policy “active” group, versus the less aggressive, or policy “passive,” group before and after the pandemic. Dividing the data by time and by country is a common statistical strategy used to find the effects of a policy. The intuition is that those countries with a less generous policy response act as a control group before and after the pandemic. If the measures introduced by the United States and other countries in the active group had no effect on inflation, the set of passive and active countries should exhibit similar inflation paths. The extent to which they do not can help us measure the effect of active policies on inflation in that country.

For the model, we measure inflation using core CPI and construct one-year-ahead inflation expectations for each country by predicting CPI future observations from a history of 20 years of inflation data as in Hamilton et al. (2016). We construct the real disposable income gap by removing the historical trend from the data and comparing it with a scenario that extends the pre-pandemic trend through to the pandemic period. In addition, since households do not immediately spend the income they receive, we smooth the data using a four-quarter rolling average of the detrended series. Finally, our estimation method accounts for common variation over time in the evolution of the pandemic and the policies implemented, while allowing for differences in inflation across countries.

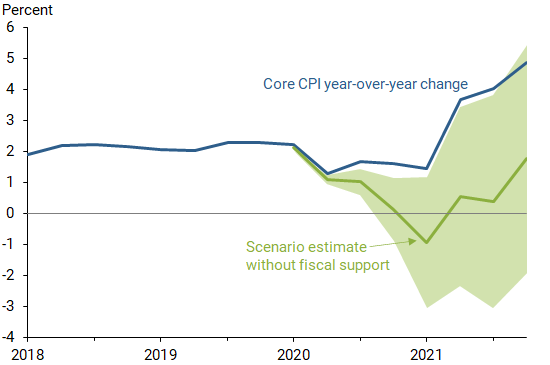

With these elements in place, we estimate our model and use it to construct an inflation path scenario. In particular, we calculate what inflation would have been if U.S. pandemic support measures had been as moderate as the passive group of countries. Figure 3 reports actual U.S. core CPI inflation against this scenario. The green shaded area shows the degree of uncertainty around our estimates. This version of the Phillips curve performs reasonably well and is comparable to historical estimates using measures of slack based on the deviation of output from its potential or unemployment from its natural rate. Importantly, however, our model allows for potential shifts in how inflation responded to economic slack during the pandemic.

Figure 3

U.S. inflation versus scenario minus pandemic fiscal support

Note: Shaded area reflects interquartile range for OECD sample.

Source: OECD Household Dashboard: cross country comparisons.

The comparison between the actual path of inflation and our scenario in Figure 3 suggests that U.S. income transfers may have contributed to an increase in inflation of about 3 percentage points by the fourth quarter of 2021. As the shaded area in Figure 3 indicates, however, this relatively sizable contribution is estimated with considerable uncertainty because the available sample is too short for any greater precision.

Our estimates fall in the upper range of findings from other recent research, although those findings fall well within our estimated confidence range. As Bianchi et al. (2021) point out, alternative modeling frameworks can result in different estimates. Barnichon et al. (2021), for example, indirectly find a much smaller, though statistically significant, contribution from fiscal measures using historical U.S. data and relying on a new measure of labor market slack. Our analysis expands on past studies by using a different sample, a different measure of slack—the disposable income gap—for an international sample, and allowing for the possibility that the pandemic shifted traditional economic relationships.

Conclusion

The United States is experiencing higher rates of inflation than other advanced economies. In this Economic Letter we argue that, among other reasons explored by the literature, the sizable fiscal support measures aimed at counteracting the economic collapse due to the COVID-19 pandemic could explain about 3 percentage points of the recent rise in inflation. However, without these spending measures, the economy might have tipped into outright deflation and slower economic growth, the consequences of which would have been harder to manage.

Òscar Jordà is a senior policy advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Celeste Liu is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Fernanda Nechio is a vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Fabián Rivera-Reyes is a research associate in the Economic Research Department of the Federal Reserve Bank of San Francisco.

References

Barnichon, Regis, Luiz Oliveira, and Adam Shapiro. 2021. “Is the American Rescue Plan Taking Us Back to the ’60s?” FRBSF Economic Letter 2021-27 (October 18).

Bianchi, Francesco, Jonas D.M. Fisher, and Leonardo Melosi. 2021. “Some Inflation Scenarios for the American Rescue Plan Act of 2021.” Chicago Fed Letter 453, April.

Hamilton, James D., Ethan S. Harris, Jan Hatzius, and Kenneth D. West. 2016. “The Equilibrium Real Funds Rate: Past, Present, and Future.” IMF Economic Review 64(4, November), pp. 660–707.

Shapiro, Adam H. 2021a. “Weighing the Role of Supply Bottlenecks in Core PCE Inflation.” SF Fed Blog, May 18.

Shapiro, Adam H. 2021b. “What’s Behind the Recent Rise in Core Inflation?” SF Fed Blog, June 18.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org