New evidence suggests that rising oil prices associated with declining oil supply slow economic activities less when interest rates are constrained at the zero lower bound. Moreover, these oil price spikes can even increase overall output. Evidence points to the following explanation. An oil supply shock raises inflation in all periods, but the nominal interest rate does not react under the zero lower bound, so the shock reduces the real interest rate, stimulating demand in the economy.

Oil prices reached $123 per barrel for West Texas Intermediate crude in March 2022, a level not seen since the onset of the Global Financial Crisis. The rapid increase in oil prices through March 2022 raised concerns that it could lead to stagflation—a simultaneous decline in economic activity and rise in prices—as experienced in the 1970s. This recent period of high oil prices coincided with the Federal Reserve keeping its short-term policy interest rate, the federal funds rate, at or near the so-called zero lower bound (ZLB).

In this Economic Letter, we empirically evaluate the macroeconomic effects of oil price changes driven by oil supply movements when the short-term nominal interest rate is at the ZLB. We find that changes in the oil supply tend to have a smaller contractionary effect on the economy—and over the longer term could even lead to an increase in output—during periods when the short-term interest rate is constrained at the zero lower bound.

Supply shocks in the ZLB

Economic theory suggests that negative shocks to the supply side of the economy, such as an increase in the cost of production, are contractionary in normal times, leading to lower output. However, they can become less contractionary or even expansionary when the nominal interest rate stays at the ZLB (Eggertsson 2008 and Bodenstein, Guerrieri, and Gust 2013). Intuitively, an increase in the cost of production due to, for example, higher oil prices, tends to push up inflation and expected inflation and reduce overall output. In normal times, the Fed raises the short-term nominal interest rate more than one-for-one with inflation, increasing real interest rates, so that households and businesses postpone their spending. When the nominal interest rate stays near zero, an increase in inflation expectations leads to a decline in the real interest rate, stimulating overall demand. If this positive effect on demand is large enough, firms can increase output, even though production costs may be higher because of the oil supply shock.

Oil prices driven by oil supply shocks

Oil price changes can originate from changes in supply or demand. For example, both a reduction in oil supply from the Organization of the Petroleum Exporting Countries (OPEC) and an increase in oil demand due to strong global economic activity can lead to higher oil prices. Failing to account for the source of oil price movements can lead to incorrect inferences.

For this Letter, our analysis focuses on price changes driven by oil supply shocks that are unrelated to macroeconomic conditions in the U.S. economy. Since changes in the reported data for oil prices reflect both supply and demand conditions, it is difficult to distinguish oil supply from demand changes. To solve this, we follow Känzig (2021), who uses the variation in oil futures prices in a tight window around OPEC production announcements. Intuitively, OPEC announcements contain news about future oil supply, and they are unlikely to coincide with news about the U.S. economy. These shocks change oil prices on impact and affect oil production more gradually. We call these changes oil supply news shocks.

We estimate the responses of U.S. macroeconomic variables, including industrial production, the unemployment rate, inflation, inflation expectations, and the short-term nominal interest rate, following oil supply news shocks. Our empirical specification allows the effects of oil price changes to be different during the ZLB period and the normal period when the nominal interest rate is not constrained by the ZLB.

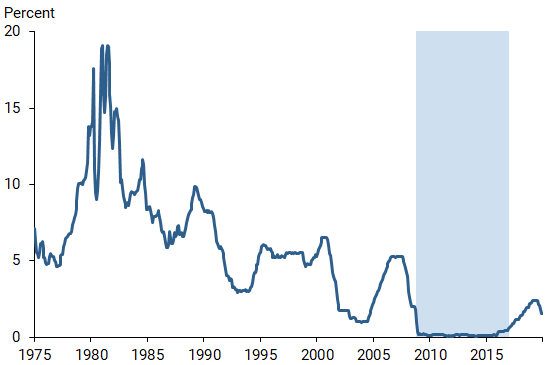

Figure 1 shows monthly U.S. federal funds rate data between January 1975 and December 2019, with the shaded area marking the ZLB period from November 2008 to November 2016, when the rate fell below 0.5%. Our results are similar if we restrict the ZLB period to times when the rate is below 0.25%.

Figure 1

Federal funds rate, 1975–2019

Source: Board of Governors.

Note: Shading indicates the zero lower bound period.

Results

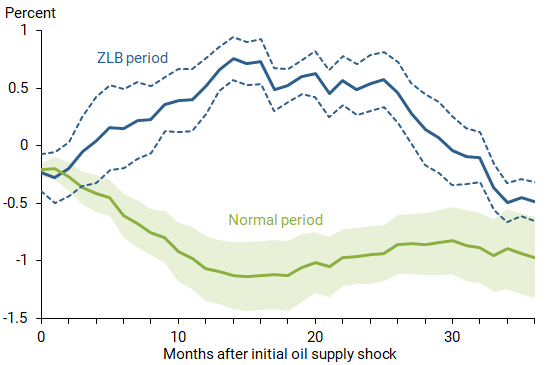

Figure 2 displays the responses of industrial production up to 36 months following an oil supply news shock associated with a 10% increase in the real price of oil, defined as the current West Texas Intermediate crude oil price divided by U.S. consumer price index (CPI). The blue line shows the movements of industrial production estimated with data in the ZLB period, and the green line shows the estimation with data in the normal period. We also plot the confidence bands, which show the statistical uncertainty around each estimate. In particular, assuming our model is correct, the confidence bands contain the true response roughly two-thirds of the time.

Figure 2

Industrial production response to oil supply news shocks

Source: Authors’ calculations.

Note: Responses of industrial production to an oil supply news shock in month 0 associated with a 10% increase in the real oil price during ZLB and normal periods. Shaded area and area between dashed lines indicate the 68% confidence bands around estimates of the same color.

In normal times, industrial production falls persistently after an oil supply news shock. A year after the shock, industrial production decreases by 1%. In the ZLB period, the shock leads to a small decline in industrial production in the first five months, reflecting the recessionary effects of oil price increases. However, industrial production increases afterward, rising by 0.5% about a year after the shock. The confidence bands do not overlap during this time, indicating that the difference between the responses of industrial production in the ZLB period and those in the normal period is statistically significant for horizons between six months and two years after the shock. Our estimates using the unemployment rate to measure the effects on the labor market (not shown) are also consistent with oil supply news shocks being less contractionary in the ZLB period than in the normal period over a one-year horizon.

Why are the effects of oil supply shocks different in ZLB periods?

A potential explanation for the different responses of real economic activity to an oil supply news shock during the ZLB compared with normal periods is the behavior of real interest rates.

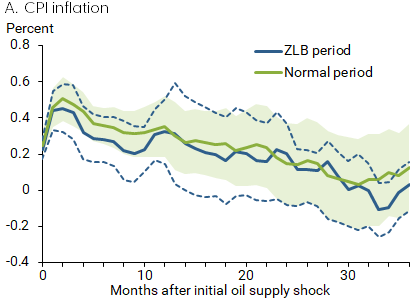

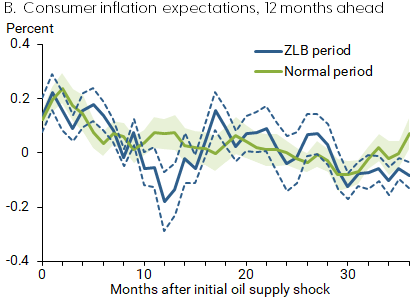

To examine whether evidence supports this explanation, we assess the reactions of inflation and inflation expectations. Figure 3 shows the impulse responses of headline CPI inflation and household inflation expectations as reported by the University of Michigan Surveys of Consumers.

Figure 3

Responses in U.S. economic activity to oil supply news shock

Source: Organisation for Economic Co-operation and Development, University of Michigan Surveys of Consumers, and authors’ calculations.

Note: Responses to an oil supply news shock in month 0 associated with a 10% increase in the real oil price during ZLB and normal periods. Shaded areas and areas between dashed lines indicate the 68% confidence band around estimates of the same color.

The response of headline CPI (panel A) is similar across the normal and ZLB periods. After an oil supply news shock associated with a 10% increase in the real oil price on impact, the CPI increases up to 0.5% in the normal period and more than 0.4% in the ZLB period. In both cases, the maximum response occurs two months after the shock. The shock also raises consumers’ inflation expectations in both periods (panel B). Since the shock does not affect the nominal interest rate in the ZLB period, it reduces the real interest rate. This in turn stimulates private consumption and investment demand, consistent with economic theory.

Our results are related to Datta et al. (2021) who found that the relationship between oil price movements and stock returns changes from negative to positive when the U.S. economy enters the ZLB period. This is consistent with the possibility that oil price hikes could spur economic activity during ZLB periods. By contrast, Wieland (2019), used a different way to identify oil supply shocks and found that the impacts of the shocks he identified are not statistically different between the ZLB and normal periods in Japan. In this Letter, we use a narrow window around the OPEC announcements to identify oil supply news shocks, which helps to rule out confounding factors with a high level of confidence.

Conclusion

Rising oil prices that are associated with news of oil supply disruptions typically lead to higher inflation and lower economic activity. However, when the nominal interest rate is constrained by the zero lower bound—as the United States experienced from 2008 to 2016—evidence suggests that the same oil supply news shock has a smaller contractionary effect, although it still raises inflation. When inflation and inflation expectations rise during the ZLB period, the real interest rate falls, stimulating aggregate demand and mitigating the negative effects of oil price increases on economic activity. Although our sample does not include the pandemic period, our results suggest that the recessionary effects of oil supply shocks that led to the surge in real oil prices between March 2020 and March 2022—coinciding with a period when the nominal interest rate remained at the ZLB—are likely small.

Since March 2022, the Fed has lifted its policy interest rate from zero. Thus, the nominal interest rate is likely to react more to increases in inflation stemming from oil supply shocks, such as the Russian war with Ukraine. In this environment, oil supply shocks could have a more negative impact on economic activity than they had during the ZLB periods.

Finally, our recent work in progress (Miyamoto, Nguyen, and Sergeyev 2022) expands our study to the experiences of Canada, the euro area, Japan, and the United Kingdom and finds results similar to those described in this Letter, suggesting that our findings are not specific to the United States.

Wataru Miyamoto is an associate professor at the University of Hong Kong.

Thuy Lan Nguyen is a senior economist in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Dmitry Sergeyev is an associate professor at Bocconi University.

References

Bodenstein, Martin, Luca Guerrieri and Christopher J. Gust. 2013. “Oil Shocks and the Zero Bound on Nominal Interest Rates.” Journal of International Money and Finance 12, pp. 941–967.

Datta, Deepa D., Benjamin K. Johannsen, Hannah Kwon, and Robert J. Vigfusson. 2021. “Oil, Equities, and the Zero Lower Bound.” American Economic Journal: Macroeconomics 13(2), pp. 214–253.

Eggertsson, Gauti. 2011. “What Fiscal Policy Is Effective at Zero Interest Rates?” NBER Macroeconomics Annual 2010 25 (May), pp. 59–112.

Känzig, Diego R. 2021. “The Macroeconomic Effects of Oil Supply News: Evidence from OPEC Announcements.” American Economic Review 111(4), pp. 1,092–1,125.

Miyamoto, Wataru, Thuy Lan Nguyen, and Dmitry Sergeyev. 2022. “Oil Shocks at the Zero Lower Bound.” Unpublished manuscript.

Wieland, Johannes. 2019. “Are Negative Supply Shocks Expansionary at the Zero Lower Bound?” Journal of Political Economy 127(3), pp. 973–1,007.

Opinions expressed in FRBSF Economic Letter do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System. This publication is edited by Anita Todd and Karen Barnes. Permission to reprint portions of articles or whole articles must be obtained in writing. Please send editorial comments and requests for reprint permission to research.library@sf.frb.org