Thuy Lan Nguyen, senior economist at the Federal Reserve Bank of San Francisco, stated her views on the current economy and the outlook as of March 9, 2023.

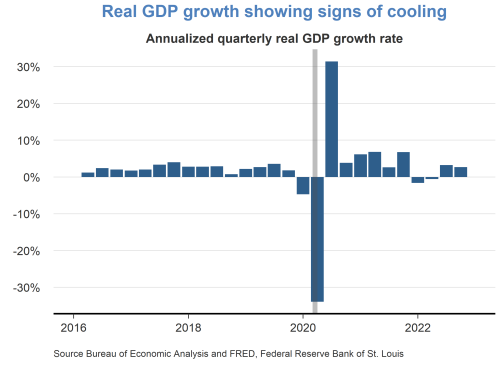

- The U.S. economy has shown some signs of cooling. Real GDP grew at an annual rate of 2.7% in the fourth quarter of 2022, down from 3.2% in the third quarter, according to the Bureau of Economic Analysis second estimate. Evidence of cooling can also be seen in the Institute for Supply Management (ISM) index for manufacturing, which has had readings below 50 for four consecutive months, indicating a contraction in U.S. manufacturing activities.

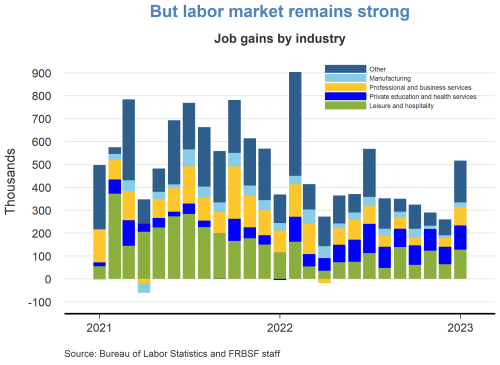

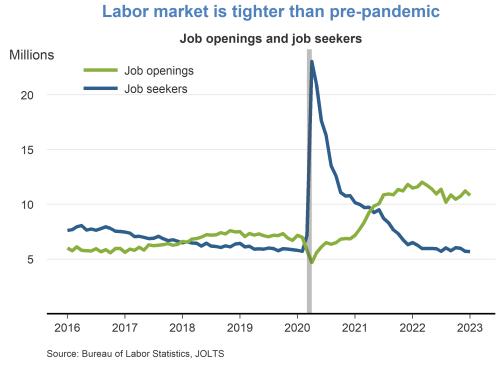

- The labor market remains strong with the unemployment rate declining to 3.4% in January, the lowest level since May 1969. Employment gains were robust in January with the economy adding 517,000 new jobs, the largest monthly increase since July 2022. The sectors of leisure and hospitality, private education and health services, and professional and business services all recorded sizeable job gains. The labor market remains very tight by historical standards. The number of job openings decreased by 410,000 in January relative to the previous month, as measured by the Job Openings and Labor Turnover Survey (JOLTS). But the number of job openings remains well above the number of job seekers as measured by the number of unemployed persons.

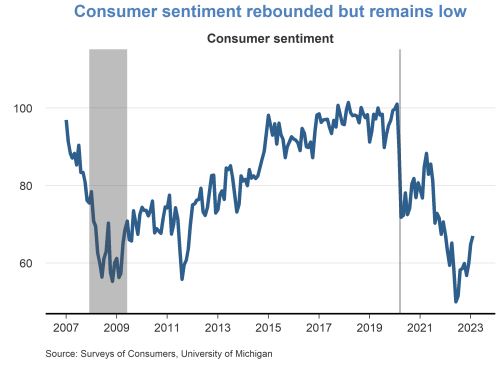

- The University of Michigan’s consumer sentiment index, which had steadily declined in 2022, continued its recent upward trend in February 2023, reaching its highest level in more than a year. However, despite the recent rebound, sentiment remains rather low and close to the levels observed during the Great Recession that ran from December 2007 to June 2009.

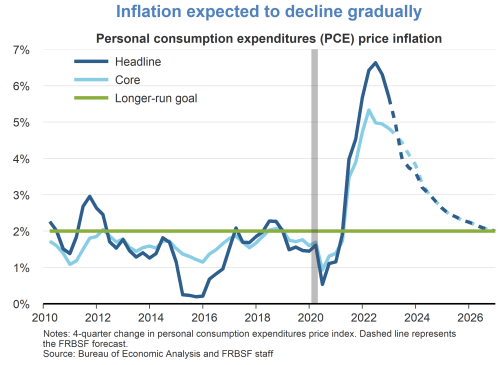

- The headline personal consumption expenditure (PCE) price index rose 5.4% over the 12 months ending in January. The core PCE price index, which excludes volatile food and energy prices, rose 4.7% over the same period. Both inflation readings are up slightly from December. While inflation has come down from peak readings recorded in June 2022, it remains well above the Federal Reserve’s 2% longer-run goal. We expect inflation to return gradually to 2%.

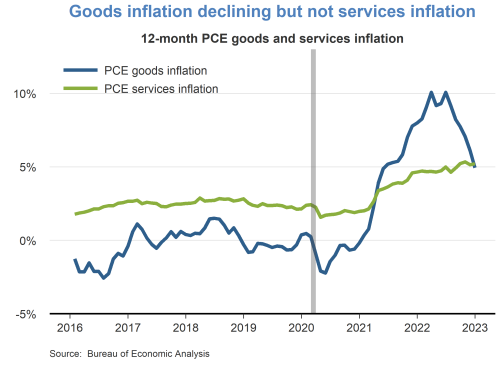

- The consumption basket used to measure headline PCE inflation is comprised of both goods and services, with goods accounting for about 34% of the basket and services accounting for the remaining 66%. The goods component of PCE inflation continued to moderate to 4.7% in January 2023 as supply chain bottlenecks continued to ease. In contrast, the services component of PCE inflation remained elevated at 5.7%. Given that services make up a large portion of the PCE consumption basket, returning inflation to 2% will require a significant drop in services inflation.

- Expectations of one-year-ahead inflation by professionals and U.S. households are mixed. According to the Philadelphia Fed’s Survey of Professional Forecasters (SPF), the one-year-ahead mean forecast for inflation as measured by the Consumer Price Index (CPI) was close to 3% in the first quarter of 2023, down from 3.5% in the last quarter of 2022. For households, the mean forecast for one-year-ahead inflation from the University of Michigan’s Consumer Survey was 4.1% in February, an uptick from the 3.9% reading in January. Research has shown that households’ inflation expectations are sensitive to gasoline prices. U.S. gas prices increased in the months of January and February, which may explain the uptick in the February reading.

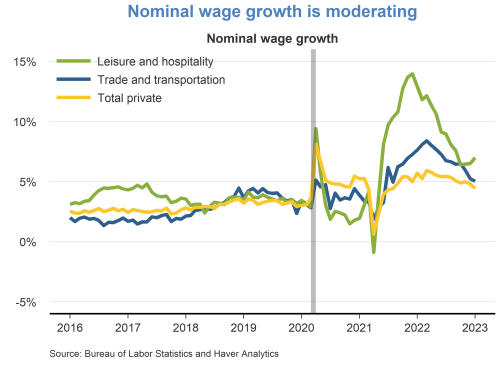

- Nominal wage growth as measured by the 12-month change in average hourly earnings was 4.4% in January, down from 4.8% in December. Wage growth is moderating but remains high in the leisure and hospitality sector, which accounted for about 12% of total private sector employment in January. Continued high wage growth poses the risk that firms will raise prices to cover their higher labor costs, making it harder to restore inflation to 2%.

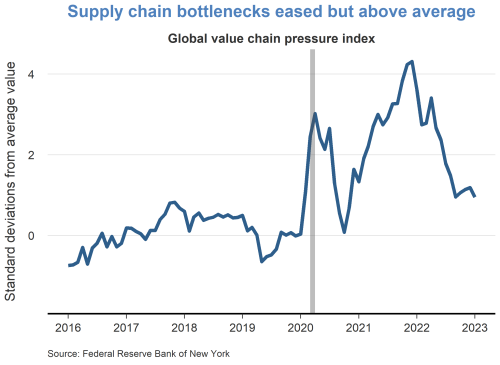

- The New York Fed’s Global Supply Chain Pressure Index declined slightly in January from the previous month. The index has declined sharply from its peak reached in July 2022, suggesting that supply chain constraints are easing. Nevertheless, the index remains well above its pre-pandemic level in January 2020, implying that some supply chain problems remain.

- The Federal Open Market Committee (FOMC) announced at the conclusion of its February meeting their decision to raise the federal funds rate target range by 25 basis points to 4.5 and 4.75%. The Committee noted that it “anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” In addition, the Committee indicated that it will continue reducing its holdings of Treasury securities, agency debt, and agency mortgage-backed securities.

Charts produced by Ethan Goode.

The views expressed are those of the author, with input from the forecasting staff of the Federal Reserve Bank of San Francisco. They are not intended to represent the views of others within the Bank or within the Federal Reserve System. FedViews appears eight times a year, generally around the middle of the month. Please send editorial comments to Research Library.